Net Zero has become an energy transition delay tactic, driven by incumbents, but it is unlikely to work – as we detail in this month’s Carbon Tracker research

Justice delayed is justice denied, is an ancient legal maxim.

It often means that if an injured party has compensation available, but it cannot be accessed in a timely fashion, then the injured party actually has no compensation at all.

Throughout the energy transition, one factor has loomed large and driven actions: time, or lack of it.

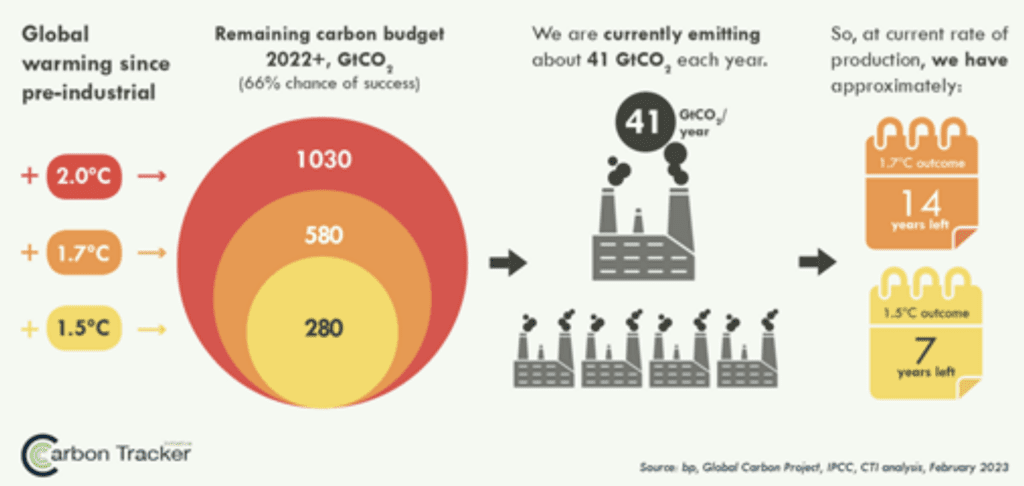

Our remaining carbon budget to allow a 50% probability of staying within a 1.5C ncrease from baseline according to the Global Carbon project , is now nine years.

And Carbon Tracker’s own analysis puts this even lower – at seven years for a 66% probability of staying at 1.5 deg C or less.

Seven or nine years is about 20% the lifespan of a coal or nuclear plant or oil refinery, and 75% the lifespan of the new internal combustion vehicle you may have just bought.

That car may outsee the global carbon budget before it is retired for a new one.

Yet most commentary, from incumbents, and even well-meaning policymakers tends to use a far more relaxed timeframe for action.

Net Zero 2050 has taken hold as a mantra for action, or more accurately inaction.

A giant global kick of a can down the road.

So to re-phrase – energy transition delayed, is energy transition denied: if we cannot access transformative actions in a timely fashion, it is as if they do not exist at all.

As we shall see below.

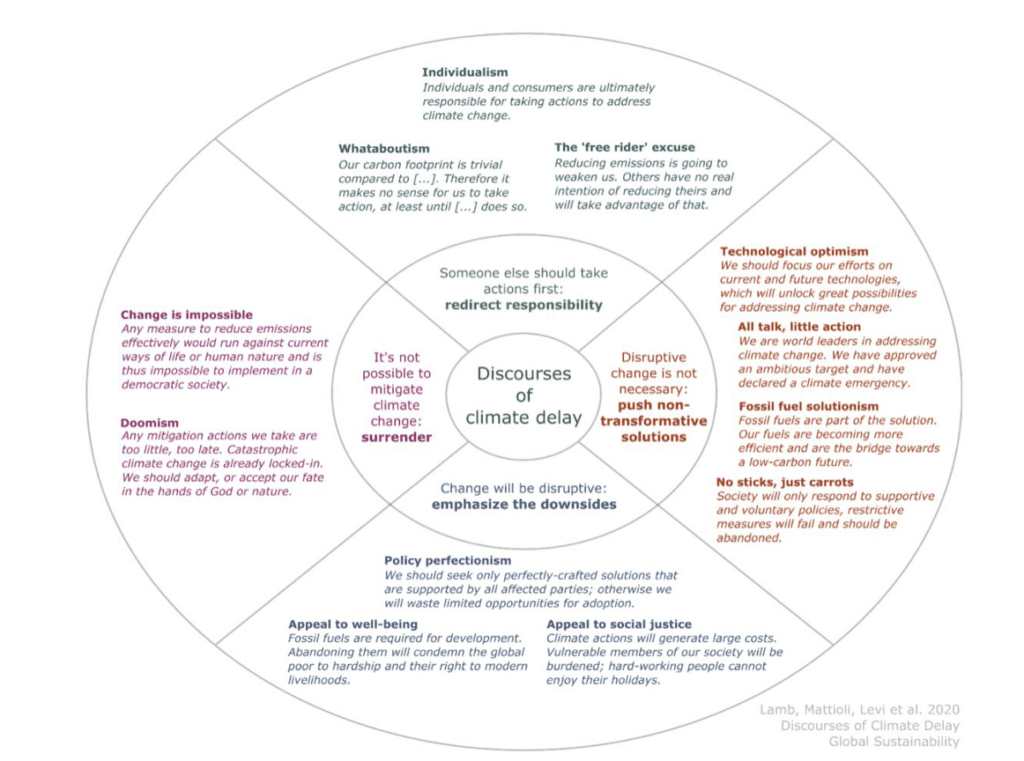

There is a whole body of work given over to how climate change denial, has now given sway to climate change delay: if you can’t beat them, delay them.

There are several analyses of this: for example the World Economic Forum outlines at least 15 delay limitations of Net Zero, but another perhaps less exhausting and accessible one is the Discourses of Delay framework below.

It highlights four main tactics for delaying energy transition: push non-transformative solutions, emphasize downsides, re-direct responsibility and basically give up.

In more detail:

- Non-transformative solutions – fossil fuels are seen as part of the solution – the poster child for this tactic is the creation of at least four emissions scopes to be targeted or talked about: Scope 1 and 2 – company / supply chain controlled, scope 3, consumer emissions and the latest addition 4 – net emissions technologies or off-sets. Plenty of room there for corporate obfuscation, vague targets and other mischief.

- Emphasise downsides – looks to fossil fuels as transition fuels and for poor country development (ignoring renewables lower costs and the fact fossil fuels have had 75 years to do this) and demanding new energy policy perfectionism before action should be taken.

- Re-direct responsibility pushes decarbonisation to consumers (Scope 3 territory) or using misdirection– ie “our carbon foot print is low, so its really China’s problem”

- And Surrender – climate change is locked in – let’s just adapt and pray

At Carbontracker of course our aim is to accelerate the transition as much as possible, given the high risks of inaction, and the high opportunities of action now and in the far future.

This month’s research highlights these delay tactics in several ways and shows how we are tackling these obstruction schemes with our analysis.

A final point is that some of the delays are knowing, and deliberate: sins of commission. Or they can be accidental due to company inaction, sins of omission.

Either way – they delay a transition to an energy system that is less dangerous and also more efficient.

Source – Carbon Brief et al

Let’s start with oil and transport: sins of commission and omission

In our blog – Are Oil and Gas Execs deserving of a windfall ? Spoiler – no they are likely not.

“Our research shows oil and gas executives are still rewarded to chase fossil growth. In our recent analyst note Crude Intentions, we examined compensation structures at the 35 largest listed oil and gas firms, and arrived at an alarming conclusion: most industry executives are still incentivised to keep fossil output growing.”

Indeed, even BP for example sometimes seen as progressive in energy change, has started to backtrack on fossil fuel production cuts, so much so that major funders are looking to resist the re-appointment of BP Chairman Helge Lund

Most oil and gas firms use the fossil fuel solutionism tactic to suggest that we need them to grow their business as part of a “bridge” to the energy transition.

As the paper notes there are many other ways to incentivise change – but the odds are shortening on oil and gas firms reverting to type – and taking the high risks of more carbon investment.

Moving deeper into the transport sector, oil’s primary domain, and possibly soon to be the largest emitter on the planet (as power sector emissions may have peaked in 2022 as noted here.)

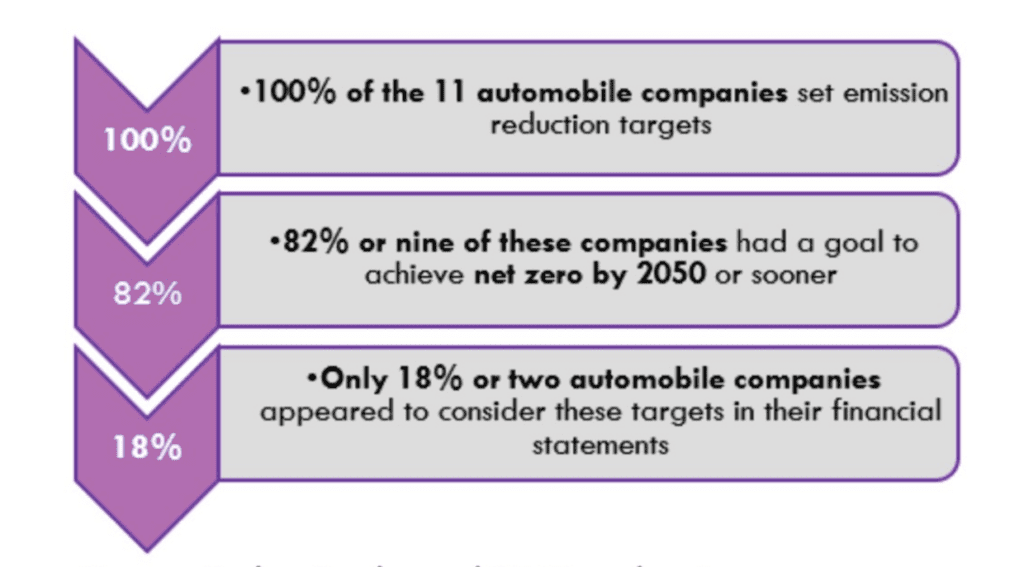

As we describe in the flash note, Driving in the Dark, many major established car companies such as VW, BMW, Toyota and Ford have all made pledges to reduce emissions, and most (but not all) to be Net Zero by 2050.

But then, only two of them appear to have costed this into their upcoming financial statements.

Consistency in treatment of emission targets

Source: Carbon Tracker and CAAP Analyses

As the delay framework shows, this is a clear example of lots of talk, but little action.

And for investors this is troubling in at least two ways.

First and foremost, the transition from an oil-fired car engine to a lithium-ion (or even cheaper sodium-ion) battery, as Clayton Christensen noted in his key work The Innovators Dilemma, should have been a simple sustaining technology change, allowing incumbent car manufacturers to easily shift power-trains.

But they have dropped the ball, as this report shows.

They have hesitated, and also allowed investment into likely dead-end technologies such as hybrids and hydrogen fuel-cell technologies.

And meanwhile Tesla and Chinese EV manufacturers such as BYD, , have now taken the initiative. So – investors now need to carefully watch how this plays out – back the incumbent horse, and assume it gets its simple engineering act together – or look to new entrants who are playing a faster game of innovation.

And so to the power market.

In power we should always start with China: it uses 30% of the world’s electricity demand, and creates almost 40% of global emissions from the power sector (due to a continued reliance on coal).

As our report here notes Balancing Act: Stranded Assets and Flexibility in China’s Power Sector

“In September 2020, the People’s Republic of China announced targets of peaking economy-wide carbon emissions before 2030 and achieving carbon neutrality before 2060.

With national emissions equivalent to approximately one-third of the global total, these commitments are some of the most significant ever made in the global response to climate change. China’s power generation is approximately 60% reliant on thermal power, the majority of which is coal-fired.

To achieve its climate targets, China must therefore transition away from a reliance on coal towards low-carbon alternatives. China has led the world in the deployment of wind and solar, bolstered by the strong financial case for renewables over coal.

However, recent data indicates that c.200 GW of new coal capacity is currently under construction or in various stages of permitting, with 50GW beginning construction in 2022 alone”

These planned investments in over 200GW of new coal capacity could lead to between US$26- US$40bn of value destruction via asset stranding. “

Too little too late and too expensive – again ignoring the key dimension of time.

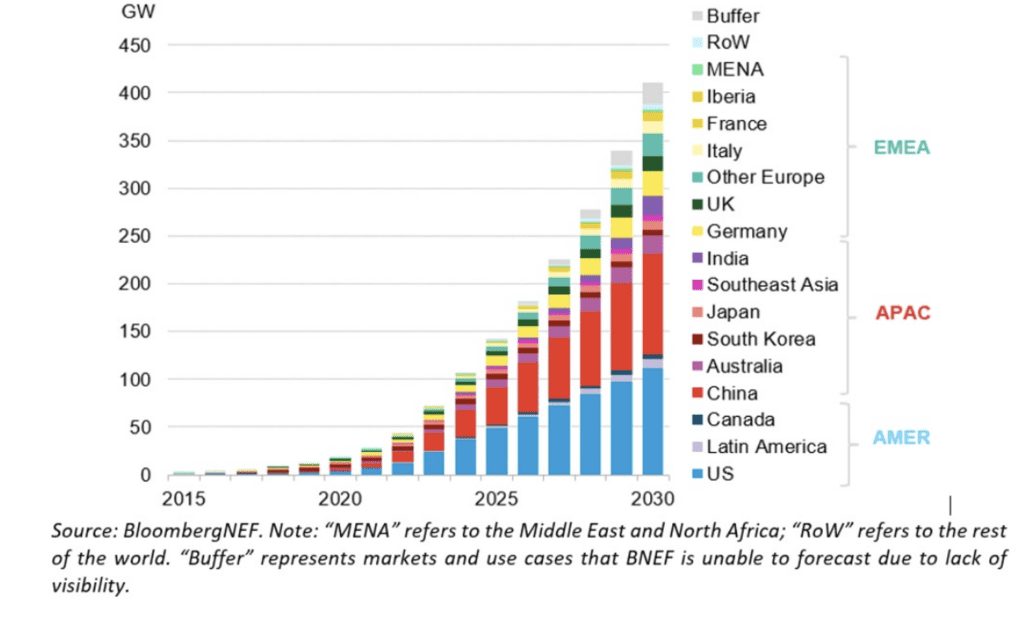

Also in the power sector we document in our power sector technology blog that rapid deployment of battery storage will be needed to support the upcoming massive growth of wind and solar in the world’s various grids (OECD and non-OECD).

“Energy storage consequently requires rapid scaling up and deployment over the next two decades in the UK to fulfil the current role of gas, but with zero emissions. Current UK storage capacity stands at only around 2.4 GW[2], but electricity system operator, National Grid ESO, last year estimated under its Future Energy Scenarios that this will need to reach at least 15 GW by 2030, and 40 GW by 2050, to deliver NZE2050”

But here for once time is our friend – BNEF forecast that global energy storage will increase by 15 times by 2030 to 410GW, from today’s 27GW, or a growth rate of 35% per year. So the UK reaching 15GW from today’s 2,4GW or 22% per year seems feasible.

This again is where the discourse of delay framework is useful.

Delay loves pessimism and emphasising problems – either instinctively or by design.

Or actually not understanding the power of exponential growth.

Exponential growth over time is our biggest supporter now that we have discovered scalable energy technologies that retain that scalability even at high levels of deployment – that is they continue to grow quickly even as they all get very big.

Global cumulative energy storage installations, 2015-2030

This is not a trivial mathematical point – those companies that ignore this fact will either over-build and strand unusable assets, or fail to invest in new technologies that could create massive new energy businesses.

To this point. How are power companies managing these transitions in the US and Europe?

Renewable Energy Targets in the US and EU Power and Utilities sector – nowhere near fast enough

In three corporate research reports we look at 2 large power / renewable energy firms in the US – Duke Energy and Next Era, and a European based global utilities firm EDF SA.

Spoiler alert – neither the US or Europe are utility providers delivering on targets.

Firstly – the US utilities.

They share a similar story – ambitions to retire fossil assets, but not on a timeline that meets Paris requirements.

Coal generation retirements may be on track – because these assets are uneconomic in any event, but gas retirement plans are behind plan.

For example, Duke owns 16GW coal and 21GW of gas generation

But Duke Energy is not Paris-aligned as it does not plan to retire gas generation by 2035 as per IEA NZE, however, the coal phase-out is aligned with zero coal generation by 2035.

A similar story is found with Next Era which is essentially two divisions – Florida Power and Light (FPL) and Next Era Energy Resources (NEER).

FPL is again not Paris aligned as although it is phasing out coal as per its Net Zero plan, it intends to generate electricity via gas beyond its targets with by our calculations almost 60% of generation coming from gas and oil in 2031, with new capacity added in 2029.

NEER is as much more renewables focussed business, with over 90% of its generation from renewables, primarily wind and solar – however its lack of progress in its FPL subsidiary means that overall it still generates 40% of its power via fossil fuels – and with targets slipping as noted especially on gas phase-out.

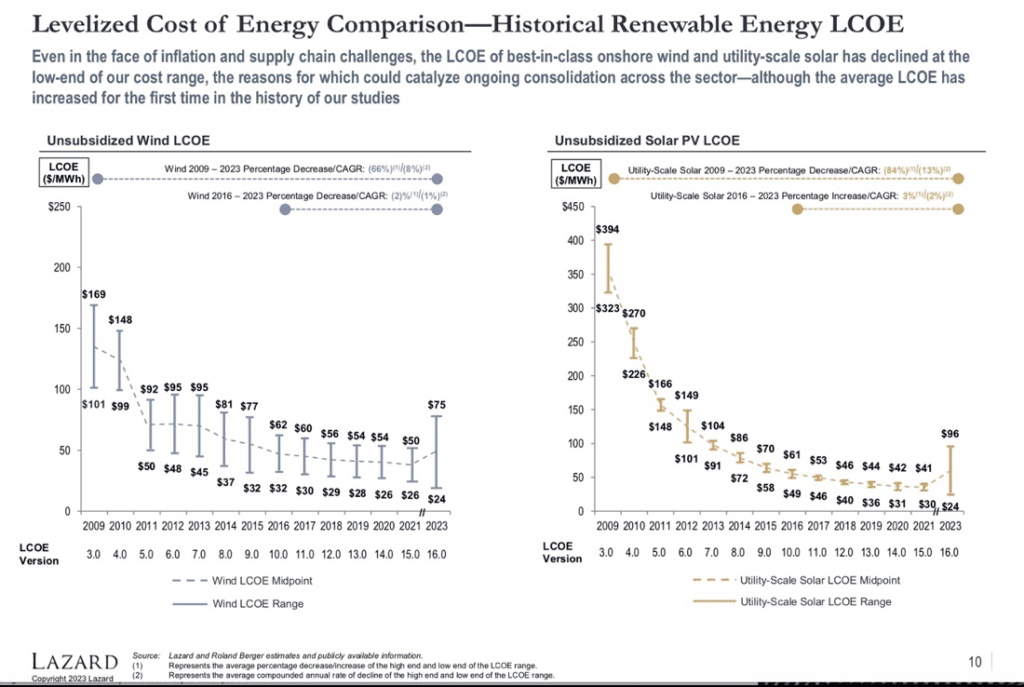

All of this is more puzzling when you consider that the levelized cost of electricity (LCOE) for wind and solar, as noted in last month’s note, is lower than gas not just for new build but for existing operating costs. So no, you can’t use that delay tactic any more either.

And they are getting cheaper – even after considering cost inflation – which hits all fuel generation sources of course but due to Wright’s Law of manufactured technologies, there is a structural change in energy costs underway at global scale – not a cyclical one.

And as Lazard note in their report – very carefully – “the LCOE of best-in-class onshore wind and utility-scale solar has declined at the low-end of our cost range, … which could catalyse ongoing consolidation across the sector”.

There is a signal here that the renewable energy sector is starting to consolidate into winners and losers. Investors take note.

Source Lazard 2023

As the CTI note concludes, the US regulatory authorities have a major role to play in re-setting fossil fuel phase out targets. It is no time to use the delay tactic of policy perfectionism: technology and the IRA / BIL act have already done their job, as we discussed in previous posts.

And Europe?

As an example we examine large utility EDF SA which has major markets in France, Italy and the UK.

As in the US, phasing out coal from EDF’s generation capacity is on track, but its nuclear legacy requiring $5bn of capital maintenance per year, and its current plans to build 5.5GW of gas generation capacity, is squeezing out a focus on renewables such as wind and solar.

A familiar story by now: retire coal (tick), retire gas (well behind plan and in fact new capacity being invested in – but all high risk).

Policy failure, regulatory capture, incumbent delay, other – pick your reason, commission or omission, but the transition in power markets is not on track.

Yet.

But the technology is there and getting better all the time and with a policy push in the right direction, such as the IRA/BIL, very fast progress can be made.

And so to conclude on optimism, which the delay lobby resists.

Why Net Zero 2050 won’t delay the transition

So on the pessimism and delay side of the ledger, many campaigns and schemes are piling up.

Incumbents and policymakers have created, for example, Scope 1 – 4 emissions targets, hoping to get analysts lost in a forest of targets, sub-targets and back-tracking on targets half-forgotten.

Engineers and financiers who should know far better are creating these false solutions, and think they are delaying investment into better alternative technologies.

It may seem very clever and divertive right now, serving various masters, but it is obvious and thus doomed.

Some of this is rational as corporations such as car firms deal with widescale structural change. But they still run the risk of ceding to new entrants who have less delay-based cultures.

Some of it is just self-serving, with oil and power companies protecting their turf. Every dollar they spend now in new oil and gas capacity should have a bright red flag fluttering above it, as we have detailed in this month’s papers.

But the recognition of limited time seems to have taken hold.

The LCOE of wind and solar has now emboldened new policy initiatives released this month such as the North Seas development project – the language signed off by nine heads of state in Northern Europe could not be more blunt:

“We cannot wait years for permitting processes while global temperatures rise, and autocratic regimes have the power to turn the lights off in our living rooms and halt production in our industries. “

Net Zero 2050 was a start.

Yet, it has grown old well before its time.

The gulf between now and 2050 allowed delay games to be created, targets to be played.

Scalable new technologies and new more realistic and rapid policies will take it from here.

In transport new entrants and new technologies – BYD and sodium-ion batteries entering the passenger car mass-market for example, are gaining market share quickly as incumbents stumble in the transition.

In power, the massive drop in cost of wind and solar have essentially scrubbed coal from the sector, and now blunted the rise of gas.

And in general, the global rise of these highly scalable technologies – electric power-trains, electric power grids and electric heat pumps – will transform the energy sector far, far faster than the incumbents expect, and want to admit.

We will likely meet Net Zero much much quicker than 2050 – technology and new policy initiatives have already realised this.

This means the 1.5 C target, already dismissed by many analysts, is still very much in play.

To exclude it now would be to fall into the hands of the delay tacticians who have much to gain from the energy transition being much slower than it should be.

Of course it will be complex and difficult – but the reality is we are making great progress, at scale, with now industrial size global technologies, growing fast, that are continuing to surprise.

As project and football managers are often caught saying: never exclude success as an outcome.

The incumbents are starting to lose ground more quickly than thought, and investors should be actively aware.