Oil and gas industry resistance to transition is a major investment risk for the industry and its stakeholders – as new technologies develop around them regardless

No one said the transformation and decarbonisation of the global energy system would be easy. But here we are, perhaps halfway through it, within the scope of a human lifespan.

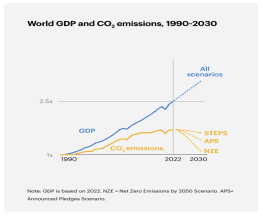

Global carbon emissions in most energy sectors are likely closing in on a peak according to the International Energy Agency (IEA).

The new technologies of wind, solar, batteries, electric vehicles (EVs) and other manufactured energy systems have pushed down the emissions curve and uncoupled it from economic growth as the IEA chart shows. The speed of transition remains the key risk, but the direction is clear.

This progress is despite the headwinds of the well-funded, incumbent fossil fuel industry, living off OPEC-manipulated cashflow, defended by a cabal of supportive academics and lobbyists. Incumbents argue that rapid change is too uncertain, and perhaps the energy sector needs to pare back ambition, innovation, investment and its renewable energy targets.

There we have the context and the key jeopardy: the transition is being resisted and delayed by powerful forces, resulting in a major emerging investment risk: energy transition opposition.

Business as usual from oil and gas is actually a high risk strategy

The oil and gas sector suggests an energy transition slow down, a pause, more business as usual. These seem like unthreatening phrases – until the consequences of them are spelled out.

For example, a recent study published in Nature, calculates that up to 20% of global economic value, GDP, could be lost by 2050 with unmitigated climate mismanagement. This aligns well with the Carbon Tracker sponsored research authored by Professor Steve Keen, and showcased in last July’s energy monitor

But the fossil fuel industry is selling a narrative that sticking with things as they are is the best way forward. The only noticeable adaptation is to recycle cash-flows from operations more into financial engineering such as buy-backs and dividend hikes.as we highlighted here in September’s monitor –the rest still goes into standard oil and gas capital, whilst renewables get an even smaller slice of the pie.

The incumbent energy industry also encourages business as usual by bowing to near-term stakeholder and political pressure to avoid emphasis on alternative energy solutions.

As multiple Carbon Tracker reports indicate there is a lot of jeopardy in this approach: net zero by 2050 by itself may not be enough because it is the pathway that matters, and most oil and gas companies are behind on key metrics to achieve even this as we have noted continuously.

For example, even two of the more progressive international oil firms, BP and Shell are dropping targets for clean energy investments, and retreating from commitments to lower emissions (see BP and Shell detailed profiles for more context).

BP has all but dismantled its Renewables division, with its chief executive leaving to “spend more time with family,” and folded the renewables unit into a standard fossil fuel department.

Shell is also paring back its transition targets in terms of lower emissions goals and lower focus on renewables and as Carbon Tracker noted under its new CEO it seems more inclined toward more traditional oil and gas investment, as we previously reported. It is also considering a move to the US which they believe has a more supportive investment environment for fossil fuel firms.

This accords with Carbon Tracker’s Paris Maligned reports where US oil and gas companies score lower in most alignment metrics compared to their current European counterparts.

Whilst such delay is a major risk to the energy transition, as Carbon Tracker noted in recent reports Navigating Peak Demand, Paris Maligned II and Crude Intentions II, it is also risky to the incumbents and their investors.

Why?

Consider oil demand

Carbon Tracker research explores the energy transition in the road transport sector, now the largest emitting sector in many regions, and one undergoing rapid change from oil-fired cars to electrified ones (with related shifts in the source of that electricity).

In our recent report Oil Companies in Disguise (2024 edition) we note:

“Car companies remain amongst the highest emitters in the world – for example, if Toyota Motor Corporation were a country, its greenhouse gas emissions including those from its products would surpass those of countries such as the UK, France, and Italy.

“Investments in legacy internal combustion engine (ICE) car manufacturers are, on average, 18% more emissions-intensive than investments in oil companies, with Hyundai and Kia being more carbon-intensive than ExxonMobil.”

This leaves the door wide open for EVs to enter the oil demand stronghold of road transport fuels.

And so, it has occurred – according to this month’s IEA review of the world 2023 EV market.

EV sales continue to grow at around 35% globally, whilst sales of oil-fired cars are declining after peaking in 2017.

Indeed, 60% of all EVs manufactured today are made in China, and China is now the world’s largest exporter of EVs.

The EU and US each hold 15% EV market share: but the titan of the oil engine, Japan, barely registers 2% market share of the world electric vehicle market.

Even if business as usual is your desired strategy, the impact on investors of Japanese original equipment manufacturers (OEMs) like Toyota could be significant if the world changes.

This is how quickly things shift when energy pivots from extracted fuels to manufactured technologies such as wind and solar and EVs– and when incumbent firms are deluded by focussing on backward-looking strategies.

The Displacement of Oil

The impact on oil demand of the change in the global car industry toward electrification is not hard to imagine (see Navigating Peak Demand noted above).

According to the IEA’s accelerated transition scenario, by 2030, 6 million barrels per day of oil will be displaced, by 2035 11 million barrels per day gone – and this in an oil market that has essentially now plateaued, so this shift is real barrels, one for one, although petrochemicals growth may reduce this impact to a limited extent.

A market losing over 10% of its demand in ten years is less business as usual, more going out of business.

If car companies are oil companies in disguise, then these major changes in energy use will visit the oil companies suddenly too as transport fuel demand dwindles, and then collapses.

A glut of LNG supply soon is widely predicted – so gas is not a safe haven from oil demand decline.

The Right Side of History?

In a recent podcast from Origin Story, What is the Right Side of History Anyway – the narrator argues there is likely no pre-ordained right way forward in politics, history or science.

Exponential curves of growth or learning curves do not just walk in the door and solve humanity’s problems.

If that were so, the logical way to fix transport emissions and dependence on oil producers would be to allow efficient Chinese EVs to dominate markets globally as soon as possible.

But that is politically unacceptable.

Yet look at the choices oil and gas companies are making. They continue to try and slow the transition, and so retain investment plans.

Clearly, these are risks to both the transition and the required pace of it.

But betting all on business as usual is a risky strategy. Trapped by inertia, the oil industry and its investors show few signs of trying anything new, and as we have noted already also recoiling from investing capital in even traditional oil and gas areas – a harvesting strategy without saying it.

Carbon Tracker continues to highlight the risks of this high-wire energy transition balancing act that will impact oil companies and their investors when they fall.

We should stick with the plans and ideas we have created that have already got us to the cusp of peak emissions a key milestone in the history of energy development- (see the Carbon Tracker reports listed above) and ignore voices who say we should slow down or resist change.

For the rest of us, now the target is to avoid stranded assets and pivot to sustainable ones, given we have the technologies required.

From pursuing growth to maximising value in decline

As noted in recent reports, especially Navigating Peak Demand (essentially a manual for efficient investment management post-peak) it is time to move from a focus on fossil fuel production growth to managing investment and planning for production to decline over time. From extraction maximisation to extraction management. And the creation of metrics and pay incentives to achieve this.

This is all feasible for incumbent firms, who could still reap profitable outcomes, but with less damage to both their stock prices and the planet.

To be clear, business as usual will only take us all to expensive and dangerous energy, as the Nature report indicates, and as shown in another Carbon Tracker report released this month analysing oil and gas well decommissioning costs in the US state of Wyoming. It is a microcosm of the risks of not adapting to energy changes: only about 4% of decommissioning costs in the state are covered, leaving a bill of maybe $900 million dollars for Wyoming residents.

Apply this calculation globally, and one can see the fossil fuel industry is storing up multi-billion-dollar liabilities for us, as it refuses to pare back its investment strategies.

The danger of business as usual

Oil and gas firms need to confront the world as it is, not as they want it to be.

We all have a stake in persuading incumbent oil firms to abandon the hubris of constant investment and transition resistance, or they risk the near-term future the ICE car industry is going through a rapid switch to new energy leaders who have manufacturing expertise or where the coal industry and its investors ended up 10 years ago after multiple bankruptcies.

Fail, and we will all have to bear not just the costs of stranded, rusting and abandoned oil wells, but also the lasting impacts of climate disruption on our economies.