A clear example of how the energy transition is changing quickly due to strides in cheap and scalable electrification is in the area of heavy duty vehicles, detailed in a new Carbon Tracker report.

This builds on earlier work here and here that the auto sector team have released in the past months.

But before the detail, let’s reverse up a little bit.

Vocabulary and terminology can sometimes act like a mental bind allowing you to accept an idea as fixed and settled. Scrutiny then passes on by.

“Energy transitions take a long time” is one adage often used by incumbents to lower the motivation of new entrants, even though there have been very few transitions on a grand scale.

Another example is the phrase “hard-to-abate” sectors.

This entered the energy lexicon early in the transition and has become widely used to label some sectors as just a “bit too difficult” at the moment, as we attend to other sectors with easier solutions, such as removing coal from the power grid.

But, as the world of energy transitions quickly, it is time to revisit this classification.

Technologies such as wind, solar, lithium-ion batteries and supporting tools such as policy frameworks and financial innovations are being deployed throughout the energy world.

And many of these have strong learning curves, meaning as we deploy a technology we reduce costs and increase quality, and so deploy more and the virtuous loop begins again: this process is well-known enough in many industrial areas to have earned a mathematical expression, Wright’s Law.

So, is the initial hard-to-abate branding still accurate?

Most analysts apply it to five sectors of the world energy system they deem difficult to fix in terms of decarbonisation.

And these segments do matter: together they amount to 30% of global energy use, and 27% of global emissions.

In rank order of emissions they are:

- Iron, steel and cement: 14%

- Heavy-duty trucks: 5%

- Chemicals: 4%

- Shipping/rail: 5%

- Aviation: 2%

Of course, the other 70% is what we tend to correctly focus on: emissions from the power sector, passenger cars, industry processes, and commercial and residential heat and light.

But putting the hard-to-abate activities into a “too difficult” file can overlook the fact that advances in the mainstream sectors, adapted, can quickly make the hard-to-abate much less problematic.

This month, Carbon Tracker’s automotive group launched a detailed report on the Heavy Duty Truck (HDV) market – No2 on the hard-to-abate league table above: Heavy Lifting Required – an associated webinar recording is here, and the press release has more details.

The report assesses the size of the challenge facing the industry and is relevant to asset managers, buy/sell side analysts, investment banks, policymakers, and of course HDV Fleet manufacturers and operators whom we review in depth.

We highlight the heavy-duty truck market here – but innovations can also spread to the other areas as deployment drives emerging solutions.

As noted by Greg Jackson, CEO and Founder of Octopus Energy when interviewed recently on the energy transition

“The reality is that it just boils down to electrification.”

So let’s look under the bonnet of the world heavy truck market and see what abatement options we now have, versus even just a few years ago.

——————

Big picture – transport emissions are 22% of the world total, 8 billion tonnes – potentially soon to be the largest contributor as power sector emissions decline quickly. It is a $4 trillion pa energy market, so there is much at stake.

And when you think of transport emissions, think first land and road – in prime position passenger cars, then trucks, then everything else that moves via air, sea and rail.

Road transport emissions amount to 6 billion tonnes per year: 4 billion tonnes from the 1.4 billion passenger cars being driven and 2 billion tonnes from the 50 million heavy trucks (> 6 metric tonnes weight) and buses on the road.

Despite being just 3% of all road vehicles, heavy trucks and buses create 30% of road transport emissions – a small but dense sector of waste in the world energy system: they emit more CO2 than all world shipping, aviation and rail emissions combined.

But we know there is also a potential solution.

And for simplicity we should keep this short: electrification.

This may sound obvious, but only a few years ago heavy duty trucks and buses were either seen as too hard to abate at all, or needed the introduction of new technologies such as hydrogen fuel cells.

Fossil-fuel fired cars and trucks are very inefficient engineering designs and produce a lot of waste.

Cars and trucks only use about 25% of the energy input of fuels such as gasoline or diesel.

The other 75% is wasted as CO2, heat and other polluting products.

Irrespective of the climate impact of this process, it is uneconomic, and harmful to the users of the product and those exposed to it.

We have covered the emissions of the global passenger car market in a recent report – Oil companies in disguise – as many legacy combustion engine manufacturers stay locked into fossil fuels, with firms such as Toyota creating tail-pipe emissions per year as high as many large countries such as the UK or France.

But Carbon Tracker has also noted the rapid ingress of ever-cheaper electric vehicles and batteries into the passenger car market, attracted by its high costs and wastefulness.

In our case study of this in the UK – S curves in the driving seat of the energy transition we show how quickly the improvement in battery technology at scale is transforming large-scale transportation.

Already EVs are 85% efficient to drive, produce no tail-pipe emissions and cost on average 15% of the equivalent fossil fuel car to run. And these numbers are improving all the time thanks to Wright’s Law.

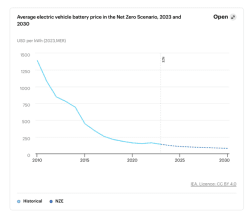

Lithium ion car batteries have decreased in price by over 95% in the last 15 years, on a learning curve of 20% pa that continues today, and is in fact in line with IEA’s most rapid Net Zero Energy scenario.

As of 2024 there are about 35 million EVs on the road, growing at about 40% pa.

And the growth rate of larger batteries for energy storage is also reaching exponential rates – with a growth in capacity of over 200% last year.

This means the solution for light duty vehicles emissions reduction – cheaper and cheaper electric batteries – can now be applied to heavier trucks.

This is far from theoretical – it has moved into the world of mass-scale deployment.

In 2023 over 100,000 electric trucks and buses were sold globally, a rise of 35% over 2022.

This only represents a market share of 1-2%, but at these growth rates the take-off in electric trucks is likely to be rapid. As a reminder: the market share of sales of light-duty EVs in 2018 were 1-2%, and are now 20%.

And when technology solutions arrive at scale they develop major policy support.

As our report notes, the EU has for example set targets of 65% reduction in emissions (from a baseline of 2019) from sales of new heavy trucks by 2035, and 90% reduction by 2040: new buses are set to be 100% emission-free by 2035.

Other countries especially China have similar targets, initiatives and policy frameworks.

Carbon Tracker calculates that for heavy trucks and buses to meet their share of global emissions reduction in the IEA NZE scenario cumulative sales of 13 million of HDVs will be needed by 2035.

That implies a continued growth rate in sales of about 40% pa – compared with today’s 35% which looks achievable.

Clearly this will need a concerted effort by manufacturers, fleet operators and policymakers to maintain the growth.

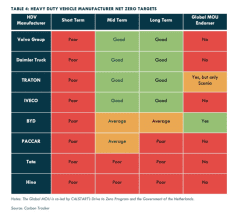

As our analysis outlines however, short-term target setting by the eight major international heavy duty manufacturers we studied is patchy, and misaligned with global emissions-free targets, especially in the short-term. Although there are some leaders such as Volvo Group and operators such as Coca-Cola.

So despite technological and deployment breakthroughs, achieving the emissions reductions required will require constant backing – especially the short-term aims, and avoiding the softness of long-term targets.

And there are of course risks to this transport “hard-to-abate” transition — key among them geo-political manufacturing disparity and associated trade wars, higher interest rates and supply chain bottle-necks slowing production.

Add to that infrastructure requirements for charging, although for heavy duty trucks this may be simpler than cars due to the use of depots and more point-to-point journeys.

But as the report advises, the background innovations will also create major opportunities:

The decarbonisation of the HDV sector will have profound effects on truck manufacturers and investor portfolios.

Once electric HDV operational savings are realised, there could be huge demand from truck fleet operators who could effectively replace their existing fleet with battery electric alternatives.

Truckmakers’ need to effectively transition to electric vehicle products to take advantage of this future electric truck demand, which means having credible emissions reduction targets working in tandem with an effective electrification strategy.

So, all stakeholders in the heavy truck sector — as elsewhere in energy — ought to be aware of how well their targets, investments, and wider strategies are adapting – or not – to the rapidly changing technologies of the energy transition.

Whether manufactures like it or not, it seems unlikely we can uninvent electric vehicles, including very big ones.

Decarbonisation is disruptive: the transition is not technology or policy neutral.

It will have a bias toward more effective technology such as ever-cheaper lithium-ion batteries, and well-designed policy incentives.

So as Greg Jackson notes above, this is not primary school: there will be winners and losers across the energy transition, and so in the heavy-duty transport market.

Today 65% of all electric trucks and buses are registered in China: the EU is developing greater market share now up to 20%, but despite new initiatives in the US, it only commands 2% market share of heavy electric truck sales.

Things will no doubt continue to change (quickly): so Carbon Tracker sees big opportunities in the heavy truck sector for those manufacturers and operators who adopt more effective targets and progressive strategies.

Things are just beginning in the trucking transition, but the road ahead is becoming clearer.

——————————–

CTI Main Links

- HDV Press Release

https://carbontracker.org/heavy-duty-vehicle-manufacturers-failing-the-ev-transition-challenge/

- HDV Full Report

https://carbontracker.org/reports/heavy-lifting-required-truckmakers-electric-transition/

- Oil Companies in Disguise

https://carbontracker.org/reports/oil-companies-in-disguise-2024-edition/

- UK Electric Vehicle Policy

- S curves in the EV market (UK)

https://carbontracker.org/s-curves-in-the-driving-seat-of-the-energy-transition/

External Links

Greg Jackson Octopus Interview

https://www.carbonbrief.org/the-carbon-brief-interview-octopus-energys-greg-jackson/

IEA HDV / Bus outlook 2024

https://www.iea.org/reports/global-ev-outlook-2024/trends-in-heavy-electric-vehicles

ICCT EU Analysis

https://theicct.org/wp-content/uploads/2024/03/ID-125-–-EU-R2Z-2023_final-1.pdf

IEA Oil Outlook – May 2024

https://www.iea.org/reports/oil-market-report-may-2024#

IEA Battery Report 2024

https://www.iea.org/reports/global-ev-outlook-2024/trends-in-electric-vehicle-batteries

Ember Global Electricity Review

https://ember-climate.org/app/uploads/2024/05/Report-Global-Electricity-Review-2024.pdf

IRENA