With UK and European leaders continuing to ponder the long-term future of power market design, common themes continue to arise across discussions as to the priority areas for reforms.

One of these is the need to increase the amount of low-carbon flexible capacity in the system to fulfil the role that polluting gas-fired units currently play in reacting quickly to swings in supply from variable renewables capacity.

This was highlighted as a key theme in responses to the UK Government’s Review of Electricity Market Arrangements (REMA) consultation, which were published in early-March. Some 35% of respondents disagreed that the Government was considering all “credible” options for the reform of the mass low-carbon power sector, with the need to focus on incentivising flexibility identified as a necessary priority in this area.

Providing sufficient incentives and pricing signals to low-carbon forms of flexible power supply will be vital to support a renewables-dominant system.

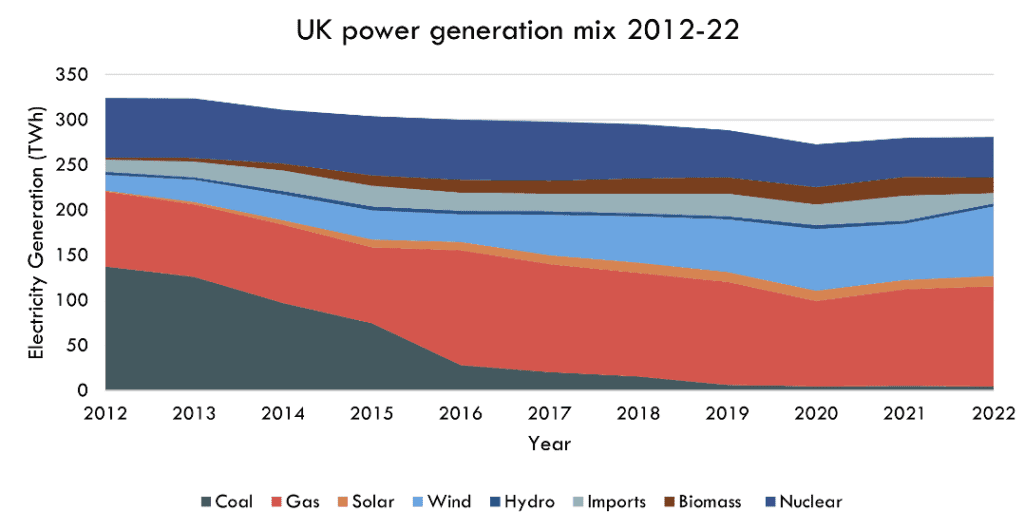

The UK currently has close to 35 GW[1] of gas-fired capacity that flexibly adjusts around fluctuating supply from renewables to maintain system stability. The use of unabated gas plants will need to end by 2035 however for the UK Government to deliver a carbon-free electricity sector within a timeframe that is aligned with economy-wide net zero by 2050 targets.

Figure 1:UK flexible gas-fired capacity has maintained system stability during coal phaseout but now needs replacing with cleaner alternatives

Source: Electric Insights

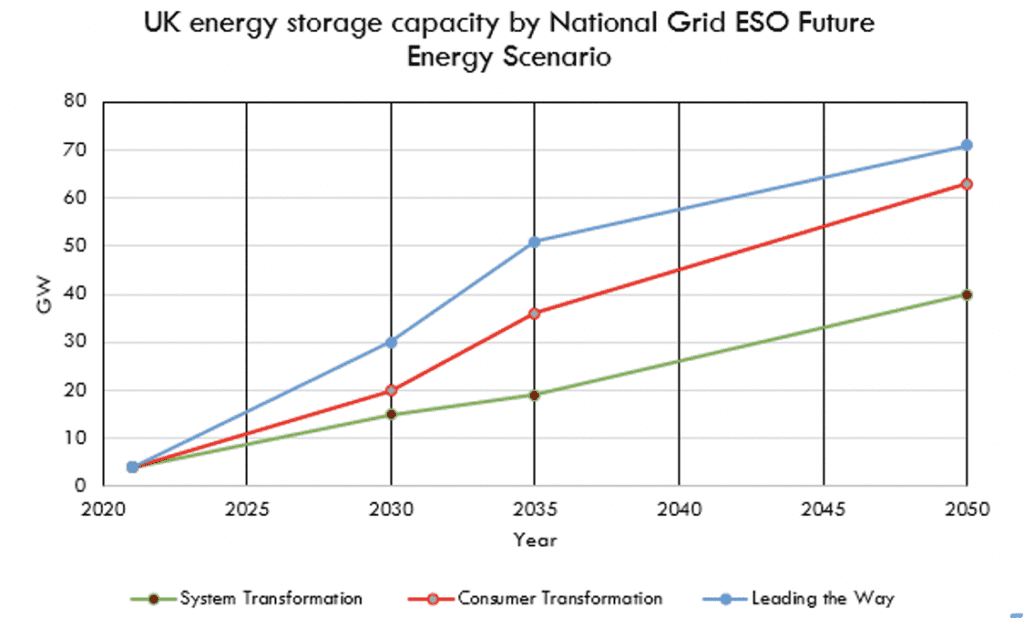

Energy storage consequently requires rapid scaling up and deployment over the next two decades in the UK to fulfil the current role of gas, but with zero emissions. Current UK storage capacity stands at only around 2.4 GW[2], but electricity system operator, National Grid ESO, last year estimated under its Future Energy Scenarios that this will need to reach at least 15 GW by 2030, and 40 GW by 2050, to deliver NZE2050.

These minimum capacity figures assume a significant scaling up of the UK’s hydrogen infrastructure under the “System Transformation” scenario, with more than 60 GW of energy storage required by 2050 if this proves not to be possible (“Consumer Transformation” and “Leading the Way” scenarios).

Figure 2: At least 40 GW of storage capacity is required by 2050 under all three National Grid ESO Future Energy Scenarios that deliver NZE2050

Source: National Grid ESO

Need to maintain intraday price volatility, but deliver long-term price stability

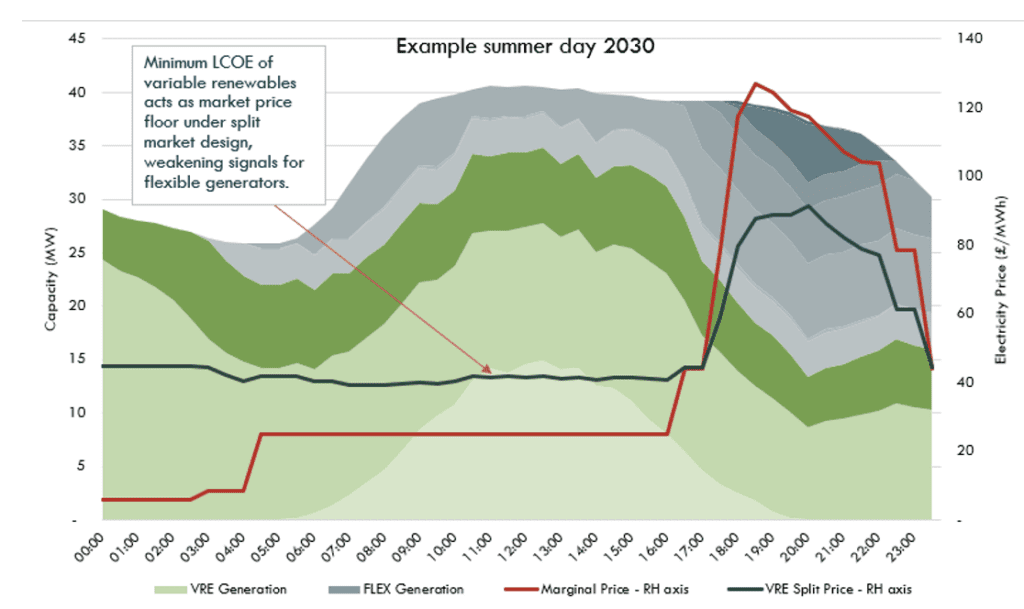

In early-February 2023, we published Marginal Call, which explores some of the UK’s most likely options for power market design reform, with a particular focus on the feasibility of a split market design that would separate the pricing of electricity produced by variable renewables from other dispatchable sources.

We concluded that a market split is unlikely to be a feasible design option[3] not only on a cost basis (only under our “very high” gas price scenario did the split market deliver cumulative savings relative to marginal pricing out to 2035), but also owing to the weaker pricing signals that would be generated under such a design for flexible forms of supply.

Our modelling work showed that given the greater influence on price formation that renewable generators are afforded under a market split, their levelized cost of energy (LCOE) effectively acts as a market floor price. While this would allow Government to unwind the green levy support schemes which currently bridge the gap between in-market revenues and the levels required to cover fixed operating costs, it would also minimise the intraday volatility that provides pricing signals for flexible technologies.

Figure 3: Low price periods would be restricted under a split power market design compared with marginal pricing

Source: Carbon Tracker analysis

Splitting the market would also risk a further collapse in wholesale power market trading liquidity, which would have a negative impact on the effectiveness of pricing signals for flexible sources, especially given the wider detachment of renewables from flexible sources that this design would bring. The increased market fragmentation that would come from a move to a locational power market design would present similar challenges.

The shift between low price periods signalling the optimal time for battery storage refill and green hydrogen production, and higher price periods for supply or generation, will be an important feature of a carbon-free electricity market which must provide these necessary incentives for clean flexibility providers to ensure system stability.

The marginal pricing design structure that the UK wholesale power market operates under has historically provided strong pricing signals to facilitate the establishment of extensive forward markets. The intraday volatility that this design allows for has also provided the incentives and business models for small-scale “peaking” gas-fired units to deploy over the past two decades, to meet the system’s growing need for flexible capacity that can react quickly to changes in output from renewables.

Policy makers must ensure that future market design continues to allow for such intraday price swings whilst protecting against longer-term spikes driven by external factors which risk pulling market prices to levels that are not reflective of the makeup of technologies supplying power.

Persisting price spikes have been seen across Europe over the past 18 months as the global gas market’s extreme volatility has fed into the gas-dependent power market, highlighting the benefits of shifting away from fossil fuels and to a cleaner power system as quickly as possible not only to deliver climate goals, but in delivering a more stable price environment for consumers.

We highlighted in our report that temporary measures may be necessary such as imposing hedging obligations on utilities for their future fuel needs, to lock in price stability for consumers, until the time comes when the gas market’s influence on the UK power system is naturally phased out through completed decarbonisation.

Ensuring sufficient price signals and incentives are in place for the rapid deployment of low-carbon forms of flexible capacity required to replace gas in the generation mix will be essential however if the GB power system is to be able to completely escape influence from the global gas market’s volatility.

Incentive schemes likely to be required to scale up flexible capacity

While sufficient pricing signals within wholesale electricity markets will be vital in allowing forms of low-carbon flexibility to operate efficiently, wider incentive schemes are likely needed first to scale up the capacity that the grid requires to be installed.

The UK capacity market has been used as the Government’s primary mechanism for ensuring that the grid has a sufficient level of flexible capacity available to deliver power system stability, with gas capacity procurement having been a prevalent feature of the scheme since its inception in 2014.

Capacity agreements handed to gas-fired generators have been accompanied by contracts issued to other forms of flexible generation in recent auctions, however, with some 1.29 GW of battery storage capacity having been successfully exiting a capacity market auction for 2026-27 with contracts earlier this year[4]. Whilst this represented positive progress, the number of such projects will need to increase significantly over the coming years if the UK is to be able to deliver a carbon-free electricity system by 2035.

A recent consultation into the future of the capacity market scheme included proposals to lower further the emissions limits imposed under the eligibility criteria for units for the scheme, which should help in assisting the allocation of contracts away from unabated gas units to cleaner forms of flexibility. Carbon Tracker’s response to this consultation called for such limits to be lowered as early as possible, and urged for long-term capacity agreements to be made available to low-carbon forms of flexibility to provide much-needed certainty for project developers.

Further reform measures which could be introduced include the launch of specific low-carbon flexibility auctions. While this would risk reducing auction liquidity, it would mean that such forms capacity are only competing with other low-carbon options and ensure that Government is able to secure a pre-determined level of such capacity that rises each year.

Alternatively, the REMA consultation document referenced the consideration of “multipliers” to the clearing price received by low-carbon flexibility providers which would mean they receive a greater annual fee for their services under the scheme than more carbon-intensive generators, improving the incentive to press ahead with the projects that are needed to come forward to continue delivering the aims of the capacity market but in alignment with long-term climate ambitions.

Cap-and-floor regime success can be replicated across UK energy policy

In our Marginal Call report, we suggested that building on the success of the UK’s cap-and-floor regime for international interconnector investment, such a regime should be considered for low-carbon infrastructure investment. A revenue-based cap-and-floor scheme would ensure that generators’ revenue streams are not impacted by the risk of the current Contracts for Difference policy not paying out during periods of zero or negative prices, which are likely to grow in frequency over time in a renewables-dominant system. Such a policy would also be more reflective of the reality that generators will source revenues from multiple sources (wholesale market, capacity market, balancing market, ancillary services) moving forward.

Linked closely to this, and proposed in the REMA document, could be a similar cap-and-floor regime for low-carbon forms of flexible technology, with projects competing with one another for contracts which would provide certainty to investors and lower the cost of capital, whilst continuing to expose such assets to the operational signals they require within the wholesale market.

While the REMA decision process on market design appears likely to roll on for at least several months more, we would urge Government to bring forward decisions for key subsections such as ways to prioritise sufficient pricing signals and incentives for low-carbon flexibility, to ensure that the UK is not steered off course from delivering the carbon-free electricity sector that is needed in just 12 years’ time.