With oil and gas firms announcing executive pay packages, some have come under fire for the bumper payouts awarded to their top employees[1]; critics say the size of the paycheques is at odds with the current cost-of-living crisis affecting millions of people in the UK and beyond.

Size and merits aside, these pay packages raise an interesting point about executive compensation in the oil and gas industry in the context of the energy transition, and the need to rapidly reduce emissions to address climate change.

What message are chief executives receiving through these paycheques? By sharing in the industry’s windfall will they be tempted to slow down transition efforts, or will they be directed to stay the course, short-term signals from the market notwithstanding?

Remuneration policies may reward market conditions more than executive performance

The oil and gas industry posted record-breaking profits for 2022.[2] While these results involved some measure of cost-cutting, outsized revenues played a much bigger role, as prices skyrocketed in the wake of Russia’s invasion of Ukraine, as illustrated by 2022 data for Chevron (Table 1). As the name suggests, these windfall profits effectively came by chance, not by design.

Table 1 – Key financial and operational performance figures at Chevron for 2021 and 2022

| 2021 | 2022 | Change | ||

| Financial performance, $bn | ||||

| Sales and operating revenues | 155.6 | 235.7 | 51% | |

| Costs | 140.8 | 196.6 | 40% | |

| Net income | 15.6 | 35.5 | 127% | |

| Operational performance | ||||

| Liquids (mb/d) | 1,814 | 1,719 | -5% | |

| Natural Gas (mmcf/d) | 7,709 | 7,677 | – | |

| Total hydrocarbons (mboe/d) | 3,099 | 2,999 | -3% | |

| Average international sale prices | ||||

| Liquids ($/bbl) | 65 | 91 | 41% | |

| Natural gas ($/mcf) | 5.9 | 9.8 | 64% |

Source: Chevron, 2023

Note: Data does not account for M&A activity, and thus figures may not be directly comparable

Judging by some of the directors’ remuneration reports disclosed in recent days, the same may be true for executive compensation. Sudden jumps in executive pay from last year suggest that directors are being rewarded for favourable market conditions rather than individual performance.

Questions of fairness aside, tying pay packages and, by extension, company performance to benchmarks outside executive control may fail to incentivise prudent governance. This is especially true if the said arrangement does not work both ways, i.e., if top employees do not get penalised for ‘bad luck’.[3] Put simply, executives are likely to be rewarded for the whims of the market, rather than strategic decisions.

Compensation structures should align with long-term corporate strategy

Even during years without windfalls, executives cannot be assumed to be acting in the best interests of their companies. Corporate behaviour can be tweaked to maximise returns this year, next year or the year after, at the expense of longer-term strategy; the effects of which may not be felt until sometime in the future, likely long after the individual executive has retired.

To ensure that executives play the long game, their variable pay must be aligned with long-term corporate strategic aims. Annual bonuses, performance share plans, and deferred bonus plans should reward action that promotes a company’s continuity well beyond executives’ own tenure, rather than incentivising short-term profits at the expense of longer-term corporate goals.

Related, the nature of ‘long-term’ incentives within compensation plans could be addressed. For example; pay schemes generally run up to three years, barely medium term on a market scale. If companies extended performance periods, that could help further align executives’ actions with long-term corporate need.

Oil and gas executives should be incentivised to adapt to the energy transition

Action to address climate change is moving into a higher gear, with pressure mounting for society to cut greenhouse gas emissions; simultaneously, the development of new technologies such as electric vehicles and energy storage means the energy transition is accelerating. Oil and gas companies must face the harsh reality that sooner or later, demand for their products will fall.

The main way to deal with this will be to plan for production output to decline, and while many companies have announced plans to prepare for the coming of the low-carbon economy, few have publicly-acknowledged that production volume of crude oil, and fossil methane (aka natural gas), will fall. To ensure that executives’ interests are aligned with long-term corporate goals, company boards should decouple the compensation plans they set from those metrics that incentivise production growth, and instead target executives on generating value for shareholders.

Further, investors seeking climate-aligned investments should look beyond simple value metrics to explore to what extent variable pay incentivises action on climate, be that in reducing emissions or actively investing in the new energy system.

Our research shows oil and gas executives are still rewarded to chase fossil growth

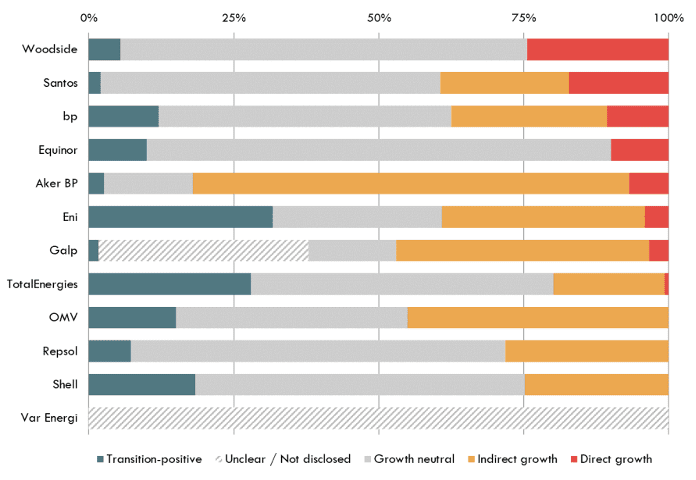

In our recent analyst note Crude Intentions, we examined compensation structures at the 35 largest listed oil and gas firms, and arrived at an alarming conclusion: most industry executives are still incentivised to keep fossil output growing. [4]

To assess how growth incentives compare with transition incentives, we group metrics into four categories[5]:

- Direct growth metrics, which incentivise fossil output growth explicitly, e.g. reserves replacement ratio, production growth, and specific fossil project milestones.

- Indirect growth metrics, which encourage fossil output growth implicitly, e.g. EBITDA, free cash flow, and net income.

- Growth neutral metrics, which are not tied to fossil output, e.g. Return on Average Capital Employed (ROACE), production costs, Total Shareholder Return (TSR), and safety and diversity targets.

- Transition positive metrics, which incentivise alignment with the requirements of the energy transition, e.g. emissions reduction targets, methane flaring targets, and renewables capacity.

Having categorised each metric, the proportion of total variable pay (across both short- and long-term incentives) that is incentivised by each category can be determined, as shown in Figure 1 for the European and Asia-Pacific companies covered. As the figure shows, there is significant variation between companies in both the proportion of variable pay linked to growth, as well as incentives that encourage progress on transitioning the company away from legacy oil and gas production activities.

Figure 1 – Target Variable Pay (With Conditions) by Metric Type – Europe and Asia Pacific (2021)

Source: Company Disclosure, CTI Analysis

Note: Var Energi does not disclose the metrics it uses to determine executive performance

While European companies may be keener to include transition-positive metrics than their Asia-Pacific and North American peers, players in all three regions have some way to go before their compensation plans can be considered transition-aligned. Direct and indirect growth metrics continue to be factored into executive paycheques.

Stakeholders wishing to see their investments aligned with the requirements of the energy transition can use their votes on executive compensation plans as leverage. The actions that they can take include:

- Challenging companies on the inclusion of direct production growth metrics, given the background of the accelerating energy transition

- Pushing for metrics that incentivise a focus on generating value ahead of volume growth

- Inspecting ‘low-carbon’ incentives with care, to see which business activities are incentivised,

- Ensuring that incentives that support emissions reductions are consistent with corporate climate goals.

[1] Lawson, A. (10 March 2023). “Doubling of BP boss pay to £10m is a ‘kick in the teeth’, say campaigners”, The Guardian, https://www.theguardian.com/business/2023/mar/10/bp-bernard-looney-pay-package; Reuters, (9 March 2023). “Former Shell CEO’s pay jumped 53% to $11.5 mln in 2022”, https://www.reuters.com/business/energy/former-shell-ceos-pay-jumped-53-115-mln-2022-2023-03-09/#:~:text=LONDON%2C%20March%209%20(Reuters),its%20annual%20report%20on%20Thursday.

[2] Wilson, T. (2 February 2023). “Shell profits more than double to record $40bn”, Financial Times, https://www.ft.com/content/b929ba6f-9e89-44f1-8f82-a12660bbc2ba; Valle, S. (31 January 2023). “Exxon smashes Western oil majors’ profits with $56 billion in 2022”, Reuters, https://www.reuters.com/business/

energy/exxon-smashes-western-oil-majors-earnings-record-with-59-billion-profit-2023-01-31/.

[3] Hausman, C. & Davis, L. (18 January 2019). “As luck would have it: Executive compensation at energy companies”, Centre for Economic Policy Research (CEPR), https://cepr.org/voxeu/columns/luck-would-have-it-executive-compensation-energy-companies; Garvey, G.T., & Milbourn, T.T. (2006). “Asymmetric benchmarking in compensation: Executives are rewarded for good luck but not penalized for bad”, Journal of Financial Economics, 82(1), pp.197-225, https://doi.org/10.1016/j.jfineco.2004.01.006.

[4] O’Connor, M. (2022). “Crude Intentions: How oil and gas executives are still rewarded to chase fossil growth, despite the urgent need to transition”, Carbon Tracker Initiative, https://carbontracker.org/reports/crude-intentions/, pp.2-3.

[5] While some metrics like fossil output growth or renewables deployment can be straightforward, others can be trickier to classify. Some companies use metrics measuring ‘low-carbon’ segments, which include, among other things, rebranded fossil hydrocarbons. To figure out which of these incentivise transition strategy and which stimulate fossil output growth, these metrics are split into proportionally between categories.