There must have been a time in the 1920s some 20 years after the introduction of the Model T Ford in the United States, and with millions of them on the road, when someone referring to motor cars as “iron horses” may have been taken quietly aside and told: “Really? Time to move on”.

Perhaps, a 100 years on, we are at that moment now with the “green energy” transition.

Twenty years after the emergence of major green energy technologies – wind, solar, electric vehicles, batteries and ancillary technologies — they have become the new energy system. Green has far less to do with it – they are just better.

Each of these technologies have grown well over a 10 times since 2000, and continue to grow at rates of 15-20% per year – meaning they could be up to three to four times bigger again by 2030: wind and solar already are 12% of the global power industry, EVs are already at 15% of global new car sales.

Play with energy scenarios galore – but the maths takes you to some unambiguous conclusions.

Green energy technology is the new energy system. Perhaps time to retire the colourful adjectives: green energy is energy.

The new energy annual deployment numbers of erstwhile “green technology” is now in the trillions, as modern large-scale energy production continues its rapid move from extraction to manufacturing.

Bloomberg New Energy Finance (BNEF) noted this month that investment in new energy technology – mostly wind, solar, EVs, batteries — reached over a trillion dollars in a single year for the first time.

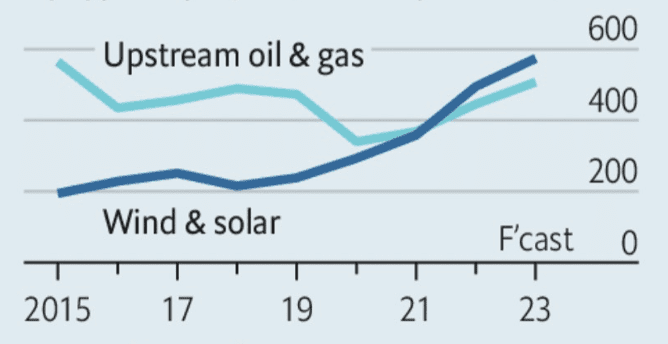

Although investment in electric vehicles (EVs) is 50% of the growth, and contrarians will argue what about the continued investment in conventional cars, the surge in wind and solar technology alone is already outpacing global capital expenditure in oil and gas for the first time ever and at what blistering pace.

Figure 1: Global capital expenditure by type of project, excl. exploration, $bn

Source: Rystad Energy

And in the case of wind and solar power (20% pa growth) and EVs (50% pa growth) the surge in new energy development at this scale pushes it to the centre of global industrial strategy.

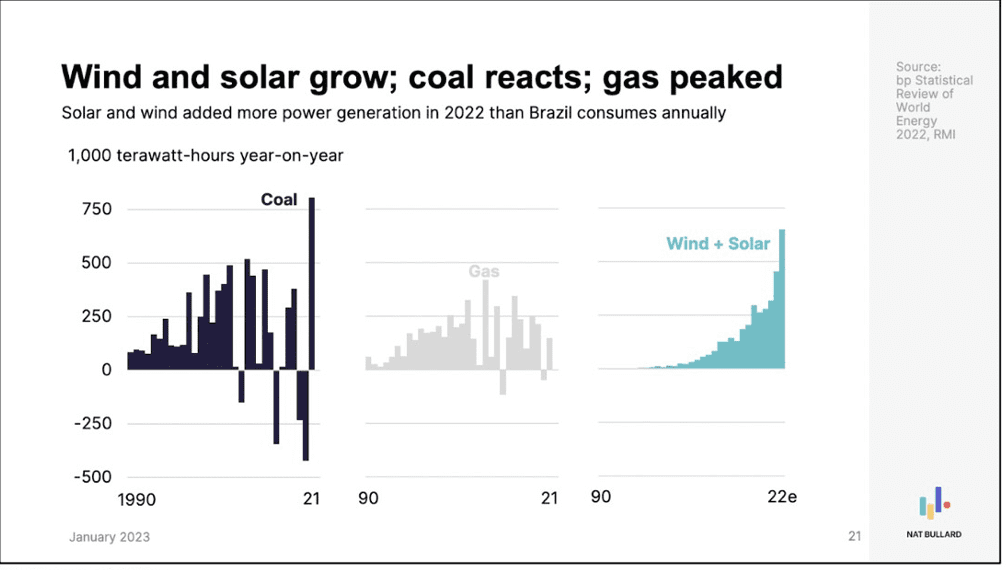

As noted here by Azeem Azhar, a technology entrepreneur, in his influential Exponential View column, citing work by Nat Bullard, the chief content officer of Bloomberg New Energy Finance, in 2022 wind and solar added between 600 and 700 terawatt-hours of new generation, about as much as Canada or Brazil generate in a year. Azhar notes:

“That is more incremental generation than natural gas has ever added in a year; it is twice as much as nuclear added at its peak in the mid-1980s. It is even more than any year of incremental growth in coal-fired power in the past three decades, with the exception of 2021 when generation increased as part of the post-2020 rebound in economic activity and power consumption.”

And it is only just getting started.

Figure 2: Wind and solar grow, coal reacts; gas peaked

Source: bp Statistical Review of World Energy 2022, RMI

No longer at the fringes as a “green alternative”, the new technologies are at the forefront of the national industrial strategy of the world’s major economic powers.

Those major economic powers are thus reacting to this reality.

When energy production flips from being an export-import commodity competition, to a home-grown manufacturing alternative the rules of the energy game have suddenly changed. Perhaps at last challenging the view that primary energy demand is now monotonic. We’ll come back to this in future posts.

The US Inflation Reduction Act (IRA) has placed up to a $1 trillion dollar bet on this new home-grown energy opportunity, the EU has reacted in kind with its own $1 trillion investment plan over the next decade.

And China, like the EU, oil and gas bereft, has for a long-time pursued a future of manufacturing energy via renewables – its 14th five-year plan released June 2022 called for 33% of power from renewable technology by 2025 (the year after next), and a sharp focus on “new-energy” vehicles.

All of this shows how the energy transition has moved from the edge of the industrial conversation to the mainstream. The notion of “green or low-emissions” technology has now dissolved into the centre of industrial policy and strategy.

This is because the new technologies — due to constant investment, improvements via learning curves and supportive governmental policies — are now cheaper, more local, provide more jobs, provide more energy options for the future and almost as an aside, emit far less carbon.

That last point is important: it means the new technologies can stand on their own two feet without the prop of subsidies or appeals to “green” principles. It allows President Biden in the US, for example, to push through the Inflation Reduction Act by focussing on these benefits, and avoid a culture war reaction to green terminology.

That is how far the new energy system has come, as the numbers show.

In a Carbon Tracker blog this month we reviewed the US IRA impact and its centrality to the energy transition: Is President Biden living up to his campaign rhetoric on climate ?

Mark Campanale, Carbon Tracker Founder and Director, said: “I think the Inflation Reduction Act (IRA) is a huge part of Biden’s legacy, so he deserves 8/10. He would have got a nine if he could have figured out the international trade implications of it first though, and a 10 if he abandoned further U.S. oil, gas, and coal development.”

In summary new energy technologies have now moved to the centre of industrial policy in the major world economies. In the US via the IRA, in the EU via their new “EU IRA” investment strategy and in China via a continuation of their long-term domestic energy production strategy.

A further Carbon Tracker piece on the theme surveyed the UK Net Zero Review, and queried:

“How to manage an energy transition which not only places the climate emergency front and centre, but does so in a way which supports and accelerates growth, jobs and investment at scale.”

The blog suggests the UK develop a Net Zero investment plan and publish its transition plans to achieve it with investment in new technologies and phase out of fossil fuels.

The piece stresses that the new energy technologies are core to industrial development.

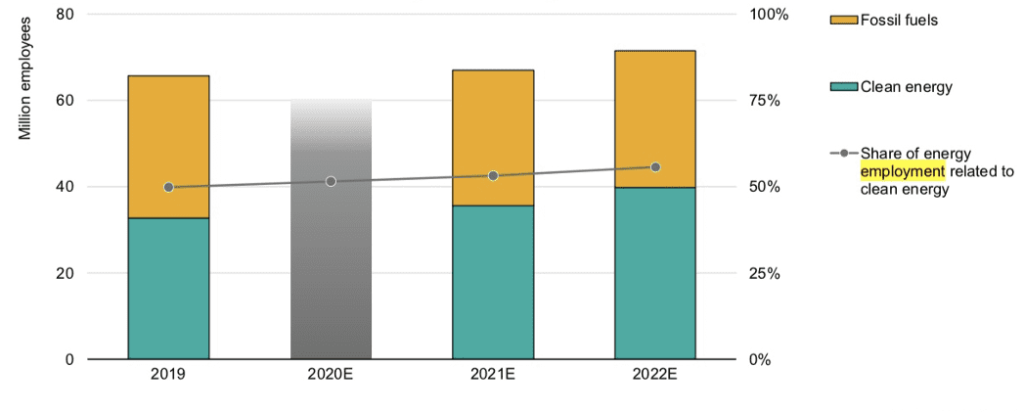

The International Energy Agency (IEA) in its latest Energy Technology Perspectives shows that employment in new energy technologies is already 55% of global energy jobs, and continues to grow as fossil fuel employment declines. The IEA sees new technology employment growing at circa 1.5 million per year to 2030, as fossil fuel jobs decline by 0.5 million annually – a net increase of 1 million jobs per year in a more efficient system.

Figure 3: Global energy sector employment by technology

Source: IEA

This combination of more jobs and lower emissions is the starting point of the new generation of industrial policy design both in the OECD and developing world. At best it is a benign “green technology” arms race, with each major bloc looking to outbid its competitors in developing competitive advantage in new energy technologies.

There are risks aplenty – trade wars, mineral dependencies, developing nations being left behind. But as energy moves to manufacturing, and becomes more dispersed, major extant risks from current fossil fuel suppliers recede too. Net risks appear to be getting lower.

As this new energy system quickly emerges we have to adapt other structures such as the pricing mechanisms of electricity supply, and to accelerate decarbonisation of the power grid – now that we have the renewable tools to do so at lower economic rates.

In 2022 Europe was caught out in the massive price swings of fossil gas into its electricity prices due the to the Ukraine war. Effectively the energy transition compressed from years into months.

In Marginal Call, Carbon Tracker analysts reviewed the reaction of the UK power market during the gas price spike induced by the Ukrainian war. As it stands the UK wholesale market prices electricity at the highest marginal cost of technology, in this case gas, even though a large part of UK electricity is provided by wind, solar and nuclear.

Their conclusion is to find a marginal price mechanism that continues the growth of renewable form of technology that will inevitably make up the majority of the grid, and not split the prices into renewables and non-renewables. A properly hedged market would have saved $8.5 billion during the price spikes in 2021-22. Ultimately, a fully renewable grid will be the best hedge against fossil fuel price risks. Key takeaways are:

- GB’s wholesale power market grid procurement expenditure over 2021-22 was not reflective of the makeup of technologies supplying electricity. Estimated grid costs turn out more than £7 billion lower on a net basis when calculated instead using a generation-weighted average of technology output over that period.

- Policy makers should consequently introduce measures to protect against future gas market price spikes which skew power market prices under marginal pricing design. These could include imposing hedging obligations on utilities for their future fuel requirements.

- The continuation of marginal pricing is still preferable to a significant shift in market design. A complete change in the market design used for the pricing of GB electricity generation may risk denting investor confidence in renewables and low-carbon forms of flexible generation by creating renewed uncertainty over project revenues. This could consequently threaten the UK’s 2035 deadline for completing power sector decarbonisation.

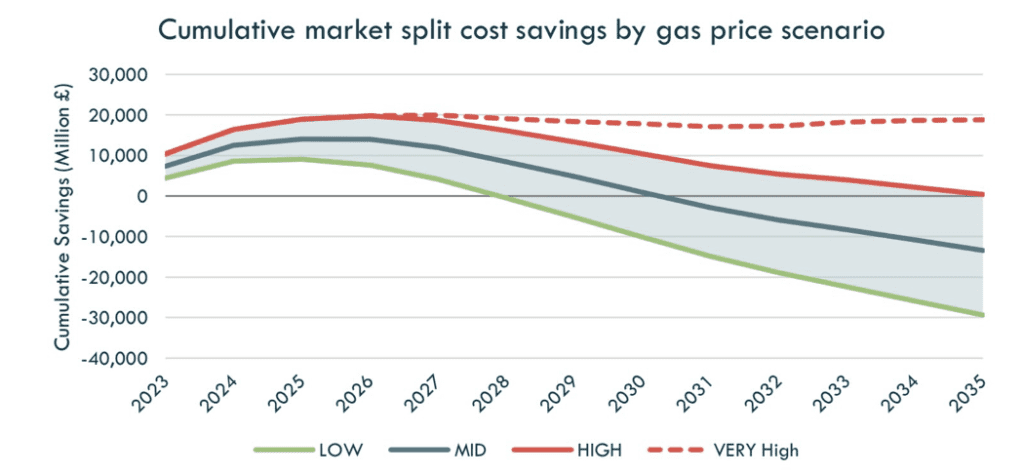

Figure 4: Gas prices would need to remain high for market split design to achieve long-term cumulative cost savings

Source: Carbon Tracker, November 2022

The sudden dependence on gas was also felt acutely in Europe. As outlined in the report EU Gas Summary , which looks at our current progress to decarbonise the EU grid. Spoiler – could do better.

“The current issue is less whether gas is a transition fuel to net zero but more whether additional import capacity solves short-term European security of supply but locks in long term supply contracts”

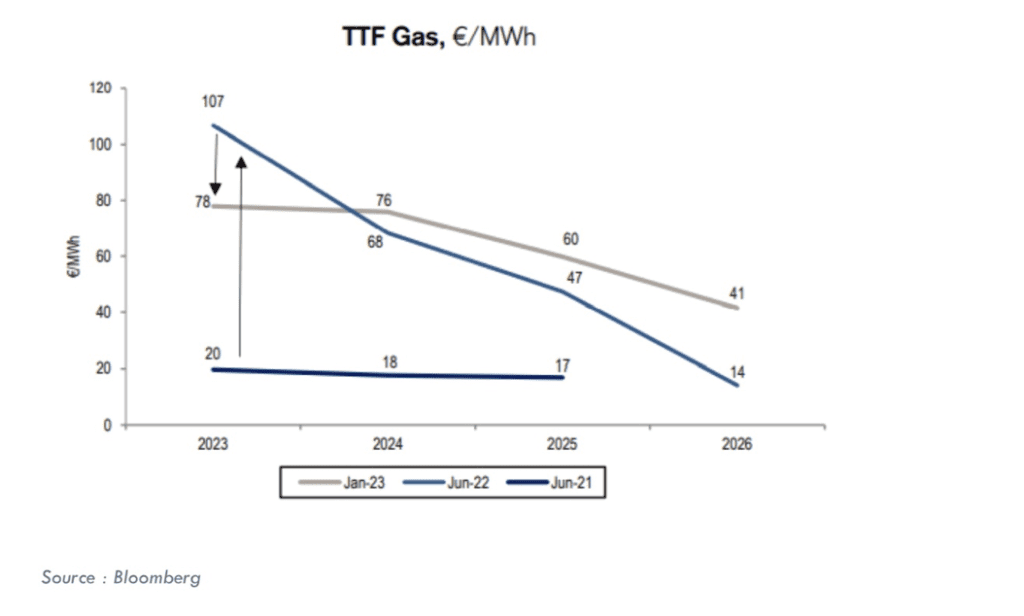

Figure 5: European gas forward prices (TTF Rotterdam), June 2021 – January 2023

Source: Bloomberg

The costs of a slow transition shown above indicates the economic impact of remaining with gas when renewables now offer a far cheaper alternative – forward gas prices are double the value in 2021.

The report digs deeper into the EU gas market by reviewing the corporate strategies of three major gas players, signed up to the CA100+ protocol, and provides a research note on each of them separately: Engie, Naturgy and Centrica.

Together these firms contribute over 300 million tonnes per year of CO2 emissions in Scope 1 and Scope 3 emissions – almost 1% of the global total.

The report also provides a detailed overview of how the companies are also looking to create “hydrogen-ready” gas capacity – a major technological and commercial challenge at a time when better solutions such as renewable are already available.

False solutions are a well-known delay tactic. It’s almost as if incumbent fossil fuel firms want to drag their heels on the transition, despite the consequences to consumers and the environment.

The report concludes:

- Engie needs to consider retiring merchant CCGT capacity. Its plans to reduce carbon intensity for scope 1 and 3 emissions from generation are not fully aligned with the goals of the Paris Agreement and current levels of profitability are probably unsustainable.

- All three companies need to deliver on plans to accelerate the renewables capacity build, particularly Naturgy.

- Absent a regulatory framework for the remuneration of investment in biomethane and hydrogen Engie and Naturgy’s gas grids risk being stranded as Government policy is full decarbonisation by 2050.

- The biggest challenge facing all three companies is scope 3 emissions reduction. In view of the scale of the task, particularly in the UK, government policy needs to set dates and develop funding support for the decarbonisation of heat.

- Investors need to ask companies three questions:

- What steps are you taking to accelerate your renewables build?

- What are you doing to push for governments and regulators to produce a regulatory framework for the remuneration of biomethane and hydrogen?

- What measures are you taking to reduce scope 3 emissions by 2030?

Related to this we also provided a response to the Financial Conduct Authorities consultation request on Sustainability Disclosure Requirements. A key input was:

“We believe that the FCA can take further steps to support the provision of useful information to the market and to align more closely with key regulations and standards — namely by providing additional implementation guidance and requiring that sustainability — related disclosures that impact financial reporting are provided, at a minimum, in annual financial reports.”

It’s worth leaving the last word to the Carbon Tracker founder in this piece, originally published in Brink News.

It returns to the classic theme of Stranded Asset Risk – but what makes it so central now, is that the peak in oil and gas is clearly in touching distance and the large-scale entry of the new energy system clearly underway as outlined in our notes this month.

This shift moves the new energy system from abstract scenario and prediction into the realm of implementation, rapidly-improving products, global-scale deployment and the quickly changing adaptation of policies on permitting and pricing.

The implications as laid out by Mark are no-nonsense:

“The energy transition is happening rapidly. Clean technologies are on S-curves of rapid, exponential growth, displacing fossil fuel demand. The two things to look for, and we’ve seen it in coal, is firstly when demand peaks for a core fossil fuel product. The key ones are obviously oil and gas because that’s where the most capital is tied up.

When you see millions of barrels of oil demand destruction a day, then you’ll see a very strong negative sentiment in the investment community toward oil and gas.

When that happens, the market will punish you by de-rating you. But at this point, with electrification happening all the way through the energy and transportation systems, it will be permanent and structural, not cyclical and temporary.”

If someone mentions to you this year that wind, solar, EVs and batteries are just fringe green technologies you might want to take them aside and say: “Really? Time to move on.”