Albert Einstein once observed: “We cannot solve our problems with the same level of thinking that created them” – and so it holds for investment consultants that have attempted to model the future impacts of climate change on pension funds, while assuming that historical levels of economic growth will continue largely unchecked, even as climate breakdown accelerates.

At root, this flawed mainstream economic thinking is drawn from the likes of William Nordhaus, who coincidentally is receiving the “energy economist of the year” award at this year’s Energy Intelligence Forum (previously known as Oil & Money). The London based event is widely attended by oil industry CEOs – and perhaps unsurprising, the oil industry prefers economic thinking that assumes the world can carry on with economic growth whilst suffering climate catastrophe.

In July – Carbon Tracker published Loading the DICE against pensions by Professor Steve Keen – pointing to the failings of academic thought on the economic damages from climate change which have, via critical failures of the peer review process, impaired an understanding of the financial risk models of investment consultants, market participants, central banks and regulators.

In the weeks following publication, investment consultant Mercer, whose climate scenario analysis was critiqued in the report, challenged the conclusions by arguing that Carbon Tracker’s analysis focussed on an ‘old’ scenario analysis model – which Mercer have since updated. And further, that Carbon Tracker didn’t analyse all of Mercer’s climate related advice and outputs, so in their view it is an “incomplete assessment” and therefore “misleading.”

Mercer did indeed update their scenario models in 2019, with aid from Cambridge Econometrics and Ortec Finance, partly in response to concerns it downplayed climate risks – we acknowledge this in our report on page 48. But the other points ignore the thrust of Loading the DICE Against Pensions, namely that the economic assumptions and inputs regarding the physical impacts of climate change, and therefore the economic damage estimates, remain largely unchanged, resulting in surprisingly low physical climate damage estimates.

In short, it is not the Mercer model that was subject to critique, it was the academic inputs, derived from mainstream economic thinking, that are the heart of the problem.

Asked to respond to the criticisms – report author Professor Keen says ‘he is disappointed’ Mercer chose to ignore the main thrust of his report, which was that the empirical assumptions made by economists are ignorant of what climate change actually means. “Mercer could have a model that was a perfect description of the real world, but it would still return ludicrous underestimates of the dangers of global warming if it were fed the empirical assumptions economists make about climate change. I am disappointed that Mercer didn’t read my report carefully enough to realise that I did not even mention the underlying models: it is the empirical assumptions underlying the models that make them so dangerous, and unless Mercer’s new model uses entirely different empirical assumptions, then it will be as dangerous a guide to the risks global warming poses to pension funds as was their old model.”

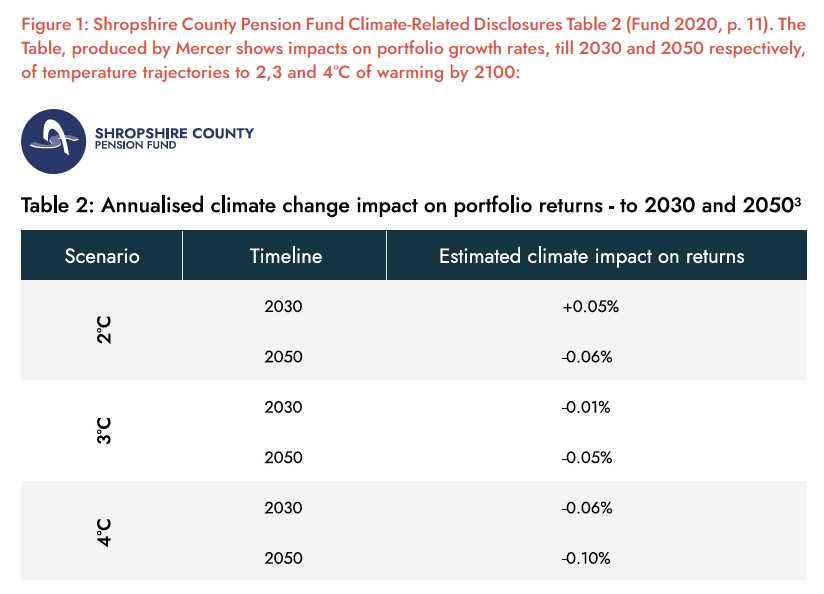

The lack of improved economic assumptions Is evident in the model outputs. Below, we reproduce Figure 1 from the report demonstrating Shropshire’s Climate Scenario Analysis output – produced by Mercer in 2020 – the first year Shropshire and LGPS Central undertook TCFD climate risk analysis, after Mercer’s “old” model was said to be updated in 2019.

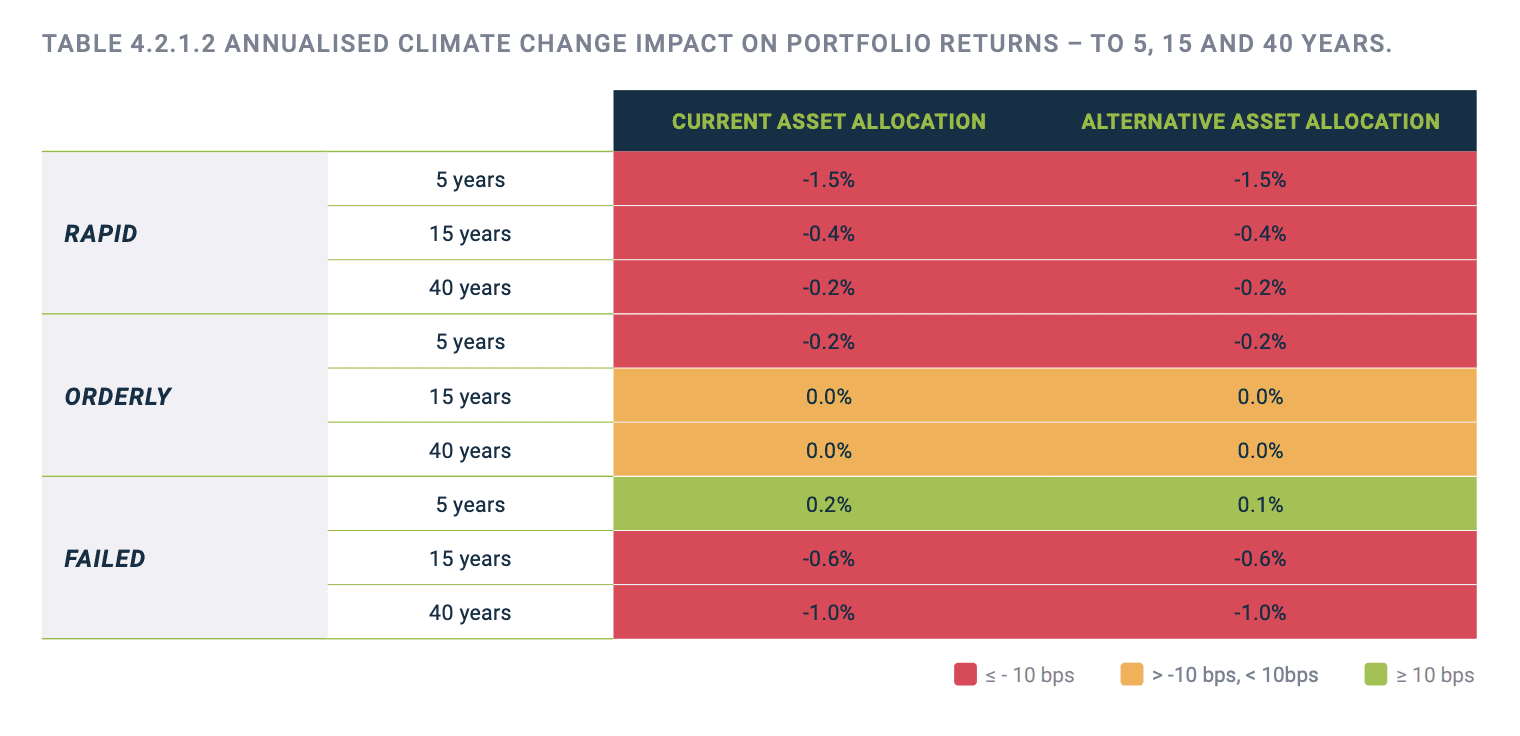

The most recent 2022 output from Shropshire LGPS does show a more significant jump in damages, (changes were made to increase damages in the model) – increasing to 1% losses per year in 2064, however the outputs are not directly compatible with 2020–- due to the reference date extending from 2050 (30 years) out to 2062 (40 years).

While a 1% reduction per year impact in portfolio returns is significant, it’s well below the 3-7% per annum annual growth rate typically achieved by share indices, meaning in the economists and investment consultants view, growth will still occur, and portfolio returns will still be positive, just by less than in the complete absence of climate change.

Fundamentally, this represents continued use of the same flawed economic literature being incorporated into Mercer’s modelling, resulting in advice that economic growth and fund returns will remain positive even in a failed transition scenario at 4C.

From the 2022 Shropshire example above–- the worst impact on annual returns, according to Mercer is under a “rapid” transition 1.5C scenario, where returns would decline by 1.5% per year in 2027 due to transition risks, a higher annual impact than from physical climate damages (-1%) with 4C warming in 2062 under a failed transition scenario.

Perhaps there are further changes that Mercer has implemented to its most recent models, but they are not readily evident from the results, which were obtained through Freedom of Information Act (FOIA) requests or published in TCFD reports. Mercer, along with other investment consultants, implored Local Government Pensions Scheme’s (LGPS) to withhold their models, scenario outputs & climate risk advice from public disclosure, so Carbon Tracker were unable to analyse much of their work.

The FOIA response of LGPS Central is typical, where the fund resisted disclosure of climate risk advice stating: “Having consulted with Mercer, both Mercer and LGPS Central consider disclosure of the correspondence would be harmful to Mercer’s commercial interests.”

This brings us to the final line of defence used by investment consultants – the notion that “even a bad model (no matter how flawed) is better than no model.”

Scientists are agreed that rapid action to drive down emissions now, will be substantially cheaper than delayed action to reduce emissions in the future. Models which trivialize the real-world impact of climate change may have the opposite effect. Loading the Dice highlights the shortcomings of current modelling and the need for a new approach.

The need for alternative modelling approaches is what drove IPCC Scientist Prof Tim Lenton at Exeter University to develop what he terms “decision useful” climate scenario models – providing the USS pension scheme with a richer narrative scenario, which has been shaped by sociologists, climate & policy experts – not just by economists.

We remain hopeful, given public comments made by The Pensions Regulator (TPR) – that key actors in the financial space recognise the deficiencies of current advice being offered to pension funds and investors, and are actively exploring alternatives.

Indeed, the TPR has called on pension fund Trustees to make climate scenario analysis “useful” and for a “revolution” in how modelling is undertaken. The TPR “recognises and shares” concerns that some climate scenarios may show impacts that seem at odds with established science, after research raised concerns that “flawed” climate analysis could be placing pension savers at risk.

Such changes would ultimately benefit investment consultants like Mercer by providing inputs that improved their climate risk modelling and therefore their advice to clients.