The fossil fuel industry is having a bad energy transition:

It is misaligned with stakeholders, climate targets and is under-investing in future energy needs.

By Harry Benham

The fossil fuel industry is not handling the energy transition well.

It is habitually misaligned with global climate targets, and also with basic corporate risk management on behalf of stakeholders.

In our research this month we highlight three key areas in oil and gas and one in coal where it is pursuing short-term gains at the expense not just of climate risk, but also its stakeholder returns.

In oil and gas we highlight three major chronic and mounting risks, misaligned with the Paris goals to limit warming to 1.5°C —

- Misaligned executive remuneration still geared heavily to production growth that is not required, versus production management

- Misaligned Corporate goals – continued high-risk investments in new oil and gas project sanctions, watered down emissions targets and negligible investment in renewables squandering growth opportunities

- Misaligned technology — Carbon Capture Utilisation and Storage (CCUS) is a costly diversion, with poor performance and practically no climate impact while adding to the cost of doing business

In addition we find misaligned Asia Coal – In the coal sector we note that one of the major coal-fired emitters, India, continues to invest in new capacity, when renewable energy would be a far better national investment.

Put together it adds up to a fossil fuel industry that is pursuing purely tactical transition thinking: continuing to focus on current production and over 40% of operational cash flow recycled to existing stakeholders without any longer-term energy aims.

The lack of alignment with Paris goals is one element – but the lack of efficient long-term investment planning in fossil fuels as well as renewables is also incoherent.

All built on the fact that it expects OPEC+ production cuts to preserve prices, and that fossil fuel consumption will continue to grow, even as new energy sources in power and transport are growing exponentially, meaning fossil fuel peak demand is more or less accomplished.

This continues to add risk upon risk of stranding assets leading to major financial write-downs, brought ever closer by their unrelenting devotion to growth.

It is a form of energy anarchy, even as the industry calls for an orderly transition.

Misaligned Remuneration

We start with the report Crude Intentions II where our oil and gas analyst Saidrasul Ashrafkhanov outlines the issues regarding executive remuneration and its continued departure from Paris goals.

As the energy transition continues to accelerate, demand for each of the fossil fuels is likely to peak well before 2030. Oil and gas companies must plan for an economy with falling hydrocarbon use; for most, this means setting a strategy that includes planning for declining hydrocarbon output.

To ensure that transition strategies are duly executed, executive remuneration should be framed accordingly.

Carbon Tracker has been analysing executive pay in oil and gas since 2019, and this note presents the latest update to the series. In this note, we delve into the executive compensation packages at 25 of the largest publicly listed oil and gas companies, analysing the incentives guiding decision-making at the C-suite level.

Key Findings:

- Our analysis shows that almost all companies studied continue to incentivise the growth of hydrocarbon output, the reverse of a prudent financial risk management strategy

- Worse, metrics that appear to superficially drive the transition from oil and gas are actually growth under a different name, e.g. LNG as part of “low-carbon” offerings.

- Overall, there was little change from 2021, so another three years closer to the consequences of stranded assets

The Bottom Line?

Most remuneration strategies are still couched in terms of direct growth of production which creates a multiplied risk: continuing investment into high-risk assets, and starving investment opportunities into new energy opportunities as we noted in Navigating Peak Demand

Misaligned Corporate Goals

Unsurprisingly in a sister report Paris Maligned II by Maeve O’Connor in the oil and gas team we note how this executive focus on continued production leads almost all major oil and gas companies to fail on basic transition metrics such as

- Modified production plans

- Recent project sanctions

- Emissions reduction targets

- Remuneration incentives

Leading to increasing risk exposure to the transition.

This report provides investors with analysis of climate alignment and transition risk exposures for 25 of the world’s largest listed oil and gas companies.

It is aimed at portfolio managers, analysts, sustainability and stewardship teams. It provides:

- Our first Combined Alignment Assessment, which identifies the leaders and laggards on Paris alignment, assessed according to Carbon Tracker’s key metrics:

- An update of our least-cost analysis of producers’ upstream projects, revealing the capital at risk and duration risk inherent in portfolios.

- Key considerations and areas which investors can influence to improve company performance on alignment and preparedness for a low-carbon future.

Key Findings

- Key to achieving Paris alignment will be planning for production declines and sanctioning fewer new developments

- Investor appetite for climate alignment assessments is increasing which this report attempts to address.

- Our climate assessments use key metrics to provide a holistic assessment of company climate alignment. Companies are graded from A (Paris Aligned) to H (Badly misaligned, not even trying).

Spoiler alert – most are F grade or worse!

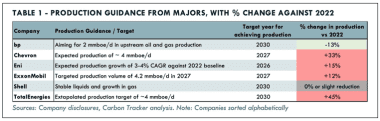

A brief look at the international oil majors sums up the state of play: almost all have aggressive growth targets egged on by their uncompromising incentive schemes, (and note even BP’s reduction targets have been scaled back since 2019).

Buyers beware.

See a related press release and for previous reports in the series, see Paying with Fire (2019), Fanning the Flames (2020), Groundhog Pay (2020), and Crude Intentions (2022).

Misaligned Technology

Oil and gas companies are also spending substantial marketing and investment energy on fossil fuel sustaining technologies such as Carbon Capture Utilisation and Storage (CCUS) which at best are a technological dead-end and at worst a diversionary tactic that will slow the transition.

In our Power sector research Curb Your Enthusiasm our review of the CCUS projects currently in operation has found a consistent trend of over-promising and under-delivering. Projects are delivered late and over budget, while the promised of levels of carbon capture are regularly missed.

Predictably the IEA have now revised down their CCUS targets to help achieve Net Zero by over 33% just in the past 2 years (we can easily guess next year’s revision.)

In this report, as an example, we analyse in detail the UK’s ambition for CCUS, where the government has an expensive strategy requiring £20bn of taxpayer funds to back private firms in this problematic and Paris misaligned technology.

We find the UK’s CCUS strategy risks locking consumers into a high-cost, fossil-based future, despite cleaner and cheaper alternatives (wind, solar, battery storage) being available.

Lorenzo Sani, Carbon Tracker’s Power and Utilities analyst, explores the risks related to this strategy including a review of the global history of CCUS, and an assessment of its ongoing delivery obstacles at any scale.

An associated press release here

Misaligned Asian Coal

And from the oil and gas sector to India’s coal industry, where the transition risks being badly managed are similar.

In a corporate review of the state owned National Thermal Power Corporation (NTPC) of India analyst Lee Ray notes that NTPC does not appear to be Paris-aligned.

It is a microcosm of the Asian coal industry’s continued reliance on fossil fuels over lower cost renewable options.

Instead, the company is targeting a reduction in emission intensity over the medium-term, rather than absolute emissions, whilst continuing to build new coal plants and expand captive coal mine production.

This should not be surprising because in spite of supportive policies for renewables the Indian government is providing a clear policy signal promoting coal-fired power investments over the medium-term.

ECINO : Energy Companies in Name Only

What is the point now of oil and gas (and coal) companies?

The irony is that even with production incentives, most oil and gas firms continue to reduce capex in new output to increase cash pay-backs to shareholders in the form of dividends and buy-backs. They recycle typically 40% of free cash flow into financial engineering rather mechanical engineering.

And at the same time invest just enough into renewables to avoid widespread negative reporting in the press.

This is a retreat from fossil fuel energy development in the long-term, and simultaneously an exit from renewable energy technologies closing off growth options.

They are energy companies now in name only: with withering investment in their core assets and refusing to invest in alternatives.

As our research this month shows, their culture and hence performance has not adapted to the new energy environment.

Investors should be clear and unblinking on these issues and ask the hard questions we outline in detail in the reports.

They should not be distracted by the cash pay-outs today, because they undermine the longer-term viability of these companies.

The transition will carry on even if the fossil fuel industry tries to ignore it, and being unprepared the consequences for it will be far more severe.

Wait too long and suddenly your business options quickly diminish.

The oil and gas and coal industries are having a bad transition, because the choices they have made mean their chances to lead it have now probably timed out.

CTI Reports

Crude Intentions II

For previous reports in the series, see Paying with Fire (2019), Fanning the Flames (2020), Groundhog Pay (2020), and Crude Intentions (2022).

Paris Maligned II

https://carbontracker.org/reports/paris-maligned-2/

CCUS Curb Your Enthusiasm

https://carbontracker.org/reports/curb-your-enthusiasm/

NTPC Corporate Review

https://carbontracker.org/reports/corporate-research-national-thermal-power-corporation-ntpc/

CTI Blogs

Paris Maligned Press Release

CCUS Press Release

https://carbontracker.org/ccus-press-release/

Are we ready for Trump Mark II

https://carbontracker.org/trump-mark-2/