Our July research has been focussed on a major new report – Loading the DICE Against Pensions, written for Carbon Tracker by Professor Steve Keen of UCL – which shows the growing systemic risks to financial and institutional investment and pension markets from the under-pricing of climate change.

It underlines a central element of the Carbon Tracker view that companies, regulators and investors now need to implement transition, and stop just talking about it, as the risks of failing to act grow exponentially.

Pension funds are risking the retirement savings of millions of people by relying on economic research that ignores critical scientific evidence about the financial risks embedded within a rapidly changing climate.

The report reveals that many pension funds use investment models that predict global warming of 2 to 4°C will have only a minimal impact on member portfolios, relying on economist’s flawed estimates of damages from climate change.

The report then underscores that such economic studies cannot be reconciled with warnings from climate scientists that global warming on this scale would be “an existential threat to human civilisation.”

Loading the DICE Against Pension Funds is a call to action for investment professionals to look at the compelling evidence we see in the climate science literature, and to implement investment strategies, particularly a rapid wind down of the fossil fuel system, based on a ‘no regrets’ precautionary approach.

Behaving now to attempt to avoid a 1.5°C increase climate change above pre-industrial levels (let alone the 4°C outcome featured in this report) will enable future generations to secure the prosperity and quality of life that comes from a healthy planet.

As Mark Campanale, founder of Carbon Tracker, notes in his foreword to the report:

Since 2011, when Carbon Tracker published its first report “Unburnable Carbon: Are the World’s Financial Markets Carrying a Carbon Bubble?”, Carbon Tracker’s mission has been to translate climate science into financial risk in order to align our financial system within a sustainable global temperature outcome.

However, the relationship between climate science and financial risk is not a comfortable one: in our special report –we show how the scientific and the economic literature are conflicted on the topics of how much damage climate change will do to the economy, and crucially – when.”

Within the global financial system, one of the critical areas where this conflict between climate science and financial risk plays out is with long-term institutional investors, especially pension funds.

To ensure that the world moves into a new climate secure energy system, it’s crucial that pension schemes send the market the right investment signals.

Today, they may be sending the wrong signals by relying on general equilibrium economic models that struggle to keep up with dynamic developments, and using economic inputs that seem far off from current trends.

As we note in the report – this matters well beyond a mathematical debate: if the consensus on climate risk management by long-term investors such as pension funds is far adrift, then there could be systemic mispricing of a range of major assets from bonds and stocks through to physical infrastructure if investors do not take immediate preventative actions.

Alternatively, inaction, a bias toward “business-as-usual” , and relying on outdated risk management models is increasingly likely to have large negative and systemic financial consequences across multiple investment sectors.

The huge disconnect between what scientists expect from global warming, and what economists are claiming means that a “Climate Change Minsky Moment” could occur at a time well within the investment horizon of existing firms.

This disconnect could therefore cause a plunge in asset market valuations, not as the result of a collapse in credit-based demand as in previous financial crises, but as the result of divergence between the optimistic predictions of economists, creating a massive under-pricing of long-term risks on the one hand, and the reality of global warming on the other.

To that point, research by climate scientists implies that the impact of a 3°C increase of planetary temperature above pre-industrial levels (or even lower) could be “catastrophic”, that climate tipping points could be triggered even at 1°C of warming (the situation now), and that changes to our climate which could trigger tipping points are “too risky to bet against” by major institutional investors.

Contrast this with the central economist’s point of view.

For example, some of the tipping points noted in our paper that were considered by high-profile economists, but then dismissed as low economic impact include:

- Loss of summer sea ice in the Arctic;

- Slowdown of the Atlantic Meridional Overturning Circulation (AMOC);

- Increased variability of the Indian summer monsoon;

- Release of carbon from permafrost;

- Release of carbon from ocean methane hydrates;

- Dieback of the Amazon rainforest;

- Disintegration of the Greenland Ice Sheet; and

- Disintegration of the West Antarctic Ice Sheet

Add to this other issues such as urban pollution and attendant health issues, sea-level rise near high-density coastal cities and impacts on agricultural productivity, you may expect concern about the global impact on economies to indicate significant or devastating outcomes as we rise up the temperature curve.

Yet many high-profile economic analyses put the impact in this way: “Tipping points reduce global consumption per capita by around 1% upon 3°C warming and by around 1.4% upon 6°C warming “

So – after all these events and issues are incorporated, classic economic risk modelling concludes a barely perceptible impact – even though insurers on the front-line of climate change financial management are having to increase premiums by the year as more extreme events such as wildfires, droughts and higher wind speeds start to assault the highly complex set of infrastructures we have built worldwide.

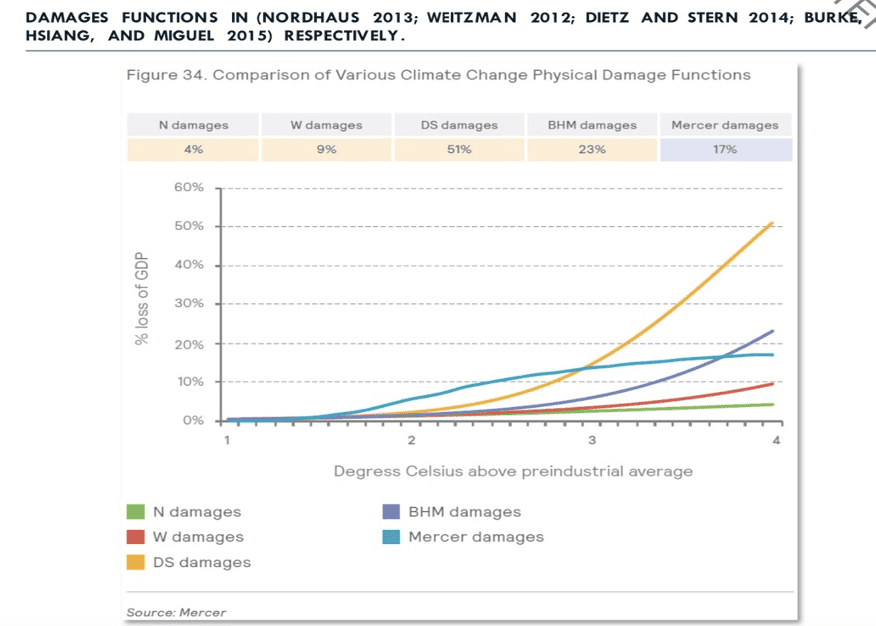

The chart below shows how a range of senior economists forecast or in effect downplay the impact of climate change up to 3°C, and also manufacture models to see 4°C as unproblematic.

In the report we quote the economist Robert Solow’s classic “smell test”: where he notes that any major macro-economic proposition should be able to pass a basic smell test – does this really make sense?

Does it really make sense that such planetary-wide risks and changes would barely shift the needle on the global economy? That floods, droughts, displacements, property damage and so on – many of which would be irreversible – would barely dent the world’s economic growth, and by inference not reduce it in any way?

A complex world system like ours, able to continue resiliently in the face of major environmental assaults, must assume the refresh rate of nature is steady, and robust to all events. This seems an irresponsible assumption, strewn with moral hazards.

For as we saw during covid when a major force collapses this system many careers, business models and institutions vanish – rapidly – for good.

And global GDP, rather than only mildly impacted, fell by over 3.4%., with EU GDP falling by over 6%.

Covid was transitory (for now), an acute disorder. Climate change is a chronic one, and to expect a minimal long-term impact seems illusory – unless it is dealt with at source.

Our report analyses the many factors, from the mathematical (quadratic versus logistical equations) to the institutional that cause these head-scratching conclusions – but the core issue is that a wide range of financial businesses and companies including many pension funds and global and local governments, incorporate these potentially risk-blind models into their investment strategies.

This puts all their investors at risk: if no action is taken by policymakers and investment managers – from central and local government, to corporations large and small, to the individual pensioner carrying out daily life assuming the portfolio is being actively risk-managed, when instead it is being passively governed.

For, if the economic risk models used to guide investment decisions trivialise the extent of the financial impacts of climate change – a worrying key finding of this report – then it is unlikely that finance officers and trustees will have the incentives

In fact, it will play to a natural institutional fund tendency to be relaxed over managing long-term risks, and to continue to invest passively in portfolio funds that will often have fossil fuel investments within their structure, exacerbating the climate change risks they are meant to be managing.

In summary – here is our paper’s Key Findings, and below we suggest key actions finance officers and trustees should now enact.

Key Findings

- Investment consultants to pension funds have relied upon peer-reviewed economic research to provide advice to finance officers and scheme trustees on the damages to asset values that will be caused by global warming.

- Following the advice of investment consultants, pension funds have informed their members that global warming of 2-4.3°C will have only a minimal impact on their portfolios.

- The economics papers informing the models used by investment consultants are at odds with the scientific literature on the impact of these levels of warming.

- The economics of climate change is an interdisciplinary subject, but papers on the economics of climate damages were refereed by economists alone. Properly refereeing these papers required knowledge of the science of global warming that economists typically did not have.

- Consequently, economic referees approved the publication of papers that made claims about global warming that are seriously at odds with the scientific literature.

- These claims have been fundamental to the predictions by economists of minimal impacts on the economy from global warming.

- Economists have claimed, in refereed economics papers, that 6°C of global warming will reduce future global GDP by less than 10%, compared to what GDP would have been in the complete absence of climate change.

- In contrast, scientists have claimed, in refereed science papers, that 5°C of global warming implies damages that are “beyond catastrophic, including existential threats”, while even 1°C of warming—which we have already passed—could trigger dangerous climate tipping points.

- This results in a huge disconnect between what scientists expect from global warming, and what pensioners/investors/financial systems are prepared for.

- Consequently, a wealth-damaging correction or “Minsky Moment” cannot be ruled out, and perhaps should be expected.

- Pension funds have a fiduciary duty to correct the erroneous predictions they have given their members.

- Similarly, financial regulators, who have used the same erroneous and misleading economic damage predictions to stress test the exposure of financial institutions to climate change, must drastically revise their stress test studies.

- This report calls on all stakeholders, from governments, regulators, investment professionals,all the way to civil society groups and individuals, to ensure that climate change policy fully incorporates the work of scientists.

- Climate change must be treated as a potentially existential threat to the economy, rather than an issue which is suitably addressed by economic cost-benefit analysis.

Recommendations for Finance Officer and Trustee Actions

At Carbontracker we believe the primary form of engagement should be to pressure companies and funds to actually implement transition, and not merely describe it in Net Zero documents. That time has gone.

Below we outline the key actions that UK-based and international pension providers officers and trustees and consultants could take to intervene and avoid these high risk outcomes for fund wealth.

Whilst the creation of Net Zero plans and activities is helpful – they are also easy to produce, typically self-monitoring and to date have resulted in a passive approach to climate change actions that avoids hard targets and actual delivery of change.

It is important to note here a simple adage from environmental analysts: the economy is a subset of nature, and not the other way around. In other words, nature rules.

In a recent related paper on climate risk mismanagement Market Myopia’s Carbon Bubble, a reinforcing point is made:

“A growing number of financial institutions, ranging from BlackRock to the Bank of England, have warned that markets may not be accurately incorporating climate change-related risks into asset price

The under-pricing of corporate climate risk contributes to the negative effects of climate change itself, as the mispricing of risk in the present leads to a misallocation of investment capital”

To underline this point of misallocating capital and subsidizing the continuing cycle of fossil fuel development Exxon will now invest over $12 billion over the next five years in Guyana adding a further 850,000 b/d to global supply, making it the largest producing country in Exxon’s portfolio – at a time when many analysts and banks still hand-wring about under-investing in oil and gas output.

And many investment portfolios retain Exxon directly and via passive indexing. Plenty of other such examples are available.

Overall, market actors continue to rely on outdated means of assessing risk, with the consequence that there is much more longer-term investment in oil and gas production than required, increasing the risk of abrupt and major financial stress via a massive market correction.

Quite simply, more creative methods of risk management need to be applied now by fund managers to avoid system-wide shocks.

As detailed in our analyst note, the lack of institutional expertise or even feel for systemic risk is not just an under-pricing of climate change: it is a fundamental part of creating it.

Key actions for investors – institutional pension funds, corporations and individuals alike – is to take more active control of these risks.

We consider below the implications of the more active approach as far as investment policies are concerned.

But investors should not be passive with governments either.

It is in their interests to ask of policymakers and regulators that their policy approach is clear, consistent and provides a direction of travel based on a timeline. This is the minimum requirement if finance and investment is to manage regulatory risk.

As the Wall Street maxim has it: If you are going to panic, panic early.

Relying on oversight bodies, consultant risk calculations and passive index investing will not protect investments against the climate change phenomena and risks we have outlined.

Pension funds and investors – without panicking – should now start to realise the high risks they are taking with nature’s finite wealth, and consider that current plans are at far higher jeopardy than proposed by current mainstream economic models.

More open discussion between funds, regulators and investors about underlying assumptions, models and inputs will help uncover the key risks, and bring pricing and investment strategies in line with the increasing hazards of continuing with fossil fuel investments and production.

Specifically, we propose:

For Pension Scheme providers

- Obtain second opinions on the likely scope of economic damages resulting from climate change, including outside the investment consultancy world – directly from climate scientists

- Ensure training on climate risk provided by investment consultants includes latest updates to the findings and recommendations of climate scientists – and does not rely on the estimates of economic damages provided by economists.

- To the extent possible, make consultant’s climate risk assessments and scenario analysis available publicly to scheme members and citizens, so that methodologies and assumptions can be subjected to wider scrutiny and refinement

For Investment Consultants

- When conducting scenario analysis for clients – always present damages/ losses on a cumulative basis, not in annualised form within tables – which has the effect of trivialising the estimated damages

- Make methodologies and simplifying assumptions for your models available for member and public critique, so that practices can be both better understood and improved – understanding that the alternative is likely greater regulatory oversight

The risks are clearly there and are growing.

To reiterate: pension funds are risking the retirement savings of millions of people by relying on economic research that ignores critical scientific evidence about the financial risks embedded within a rapidly changing climate.

We hope this latest energy transition monitor and the main analyst note and its recommendations will help all parties to address the major shortfalls in the current assessment of climate risk which may seriously damage planetary health, and, as a consequence, global economic wealth.