Prime Minister Rishi Sunak has promised to “max out” North Sea reserves – but the plan fails on economic, energy security, and climate grounds

The topic of North Sea oil and gas licensing has shot up the UK’s political agenda as all three elements of the “energy trilemma” – sustainability, affordability, and security of supply – have taken centre stage. What was previously a technocratic procedure, managed by a little-known regulator and largely insulated from the cut-and-thrust of politics, is now hotly debated.

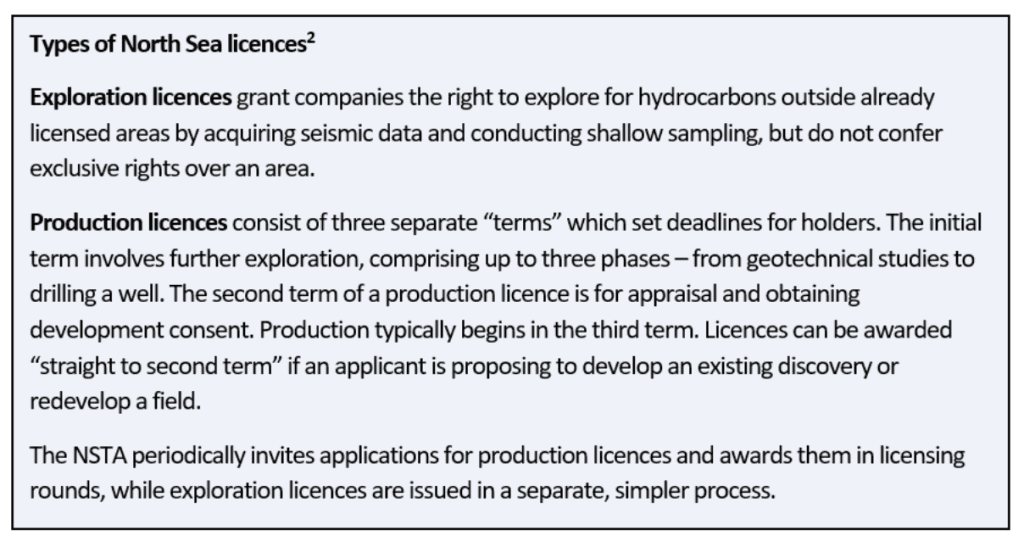

For the first time since 2019, a new licensing round was launched last year during Liz Truss’s short-lived premiership and the first licences have just been offered[1]. The government has followed by mandating annual rounds – a return to the pre-Covid frequency. As promised, the North Sea Transition Authority (NSTA) – formerly the Oil and Gas Authority – has begun by distributing permits for mature areas with known reserves, echoing Norway’s approach, but it has also made blocks available across UK waters. Twenty-seven licences, at various stages along the road to production (see box), have been issued, with Shell winning the lion’s share.

As a general election approaches, the rhetoric in the UK has become increasingly fiery. Scotland’s ruling SNP, which previously held up North Sea oil as the prize of independence from Westminster, now lambasts the UK government for supporting new drilling. Sunak, meanwhile, says it would be “economically illiterate” not to.

But would further North Sea licensing really be in Britain’s long-term interest?

As fossil fuel use declines, new projects are a risky bet

As Carbon Tracker – amongst others including the IEA – warns, if the world follows through on its climate pledges, significant fossil fuel reserves will need to stay underground. At the same time, the deployment of clean technologies is accelerating and will make increasing inroads into oil and gas demand, driving down prices – as our recent Navigating Peak Demand report and the IEA’s latest forecasts highlight[3].

While hydrocarbon prices may be high currently, both the principal causes – Russia’s invasion of Ukraine and OPEC shutting in millions of barrels amid weakening global demand – will come to an end eventually.

High-cost, long-cycle developments, such as those in the North Sea, therefore face a particularly high risk of stranding – a point former Bank of England governor Mark Carney recently acknowledged (and something companies are more broadly failing to disclose). The government’s own environmental assessment of its licensing plan notes exploration can take up to 9 years, appraisal and development planning up to 6, and production 18+ years.

So licences issued now will likely result in production well into the 2040s, when lower-cost producers will be much better placed to compete for any remaining demand. The recently approved Rosebank project, which had its production licences issued in the early 2000s and has an estimated field life of 25 years, provides an indication of how long the process can take.

No second boom is coming

Even if policymakers are unconcerned about stranded asset risk, the inescapable truth is that the North Sea has long been in decline and production is forecast to continue falling. The UK has enjoyed decades of extraction but the chances of making major new discoveries at this stage are small. Promising otherwise simply creates false hope for workers and communities dependent on the industry. The latest figures show 46.4 billion barrels of oil equivalent (boe) have been extracted, with 4 billion remaining in reserves and a further 6.4 billion in “contingent resources” which, like the reserves, may or may not end up being commercially viable.

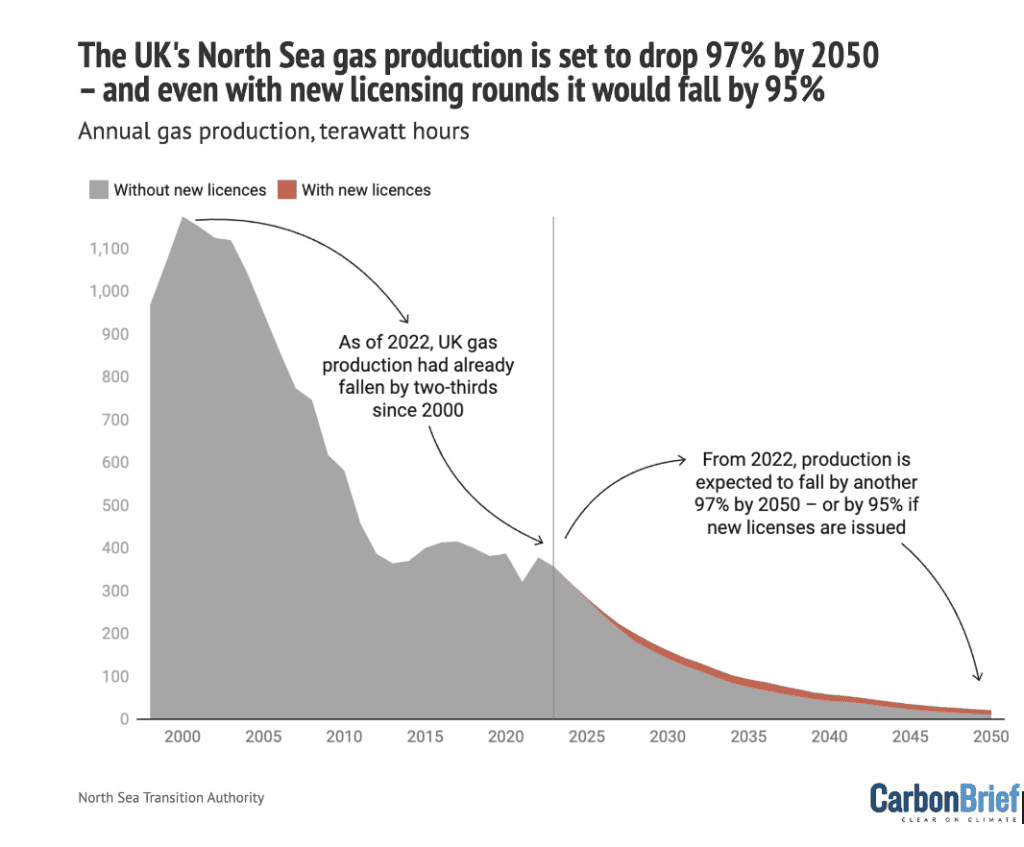

Production of gas, which accounts for roughly 30% of the remaining reserves/resources, has fallen by two thirds since 2000 and new licences would still result in a 95% fall by 2050, as opposed to 97% without. The outgoing head of the NSTA, which works to “maximise economic recovery” of the basin, said last year that new licences would make only a marginal difference to the UK’s dependence on imports.

The NSTA’s forecasts may be conservative, but if recent history is anything to go by, it would be unwise to bet on it: since 2010, only five new oil and gas fields have been discovered and seven existing fields have been developed, despite hundreds of licences being issued[4]. They contain just nine weeks’ worth of current UK gas consumption and only sixteen days’ worth have been produced from them so far. The UK is undermining its ability to persuade other countries planning much larger production to scale back, for very little potential gain.

Figure 1: NSTA forecasts of North Sea gas production, with and without new licences[5]

More North Sea production likely means higher global emissions

As the North Sea industry has come under pressure for its climate impacts, an argument has emerged that further drilling can be compatible with climate goals. The NSTA now has a duty to support net zero and an agreement struck between the industry and government seeks to decarbonise the sector with a range of measures, such as electrifying platforms. But while production-related emissions have been falling – mainly as a result of falling production volumes – this is a long way from being able to call further licensing climate-compatible.

First, there are doubts about the reliability and impartiality of the data, as Chris Skidmore’s government-commissioned review noted. Second, new lower-emission projects would only reduce the sector’s footprint if existing fields were closed early, which is not being planned.

Third, and most importantly, these emissions typically only account for 10-15% of the full lifecycle emissions of oil and gas, according to Shell. Most of the climate impact comes from the end-use combustion of the products – known as scope 3 emissions. Claims that North Sea gas is up to four times cleaner than liquified natural gas (LNG) imports ignore these emissions, which when included narrow the gap to around 17%[6]. By contrast, UK gas imports piped from Norway – which account for a larger share than LNG – are lower-emitting.

The government’s own climate advisers have criticised the tests designed to assess the climate compatibility of further licensing as weak and called for a “presumption against exploration” and “tighter limits on production”. Two new tests recently announced[7] appear to be even weaker: one says that UK gas must have a lower carbon footprint than imported LNG – which will always be the case because of the liquefaction and shipping process (and says nothing about oil production). The second stipulates that expected oil and gas production must be lower than future UK demand, which will remain the case unless demand plummets.

Ultimately, adding to overall global supply will mean more oil and gas consumed, unless production elsewhere is correspondingly cut – something no one can guarantee.

Road to energy security isn’t paved with fossil fuels

Another misleading narrative argues that further licensing will cut energy bills and strengthen UK energy security. But despite being the second largest oil and gas producer in Europe after Norway, the UK has been no less vulnerable to the ongoing energy price shock, because both are sold on the open market to the highest bidder.

Additional hydrocarbons would add a negligible amount to global supply and therefore have limited downward pressure on energy prices – something the Energy Secretary admits[8]. Extracting all proven reserves and resources would only meet around 1% of European annual gas demand out to 2050[9], while around 80% of North Sea oil is currently exported. Because fields typically take years to begin production and are notorious for delays, they would not help ease the still-high energy prices UK billpayers are suffering, as Carbon Tracker has previously highlighted.

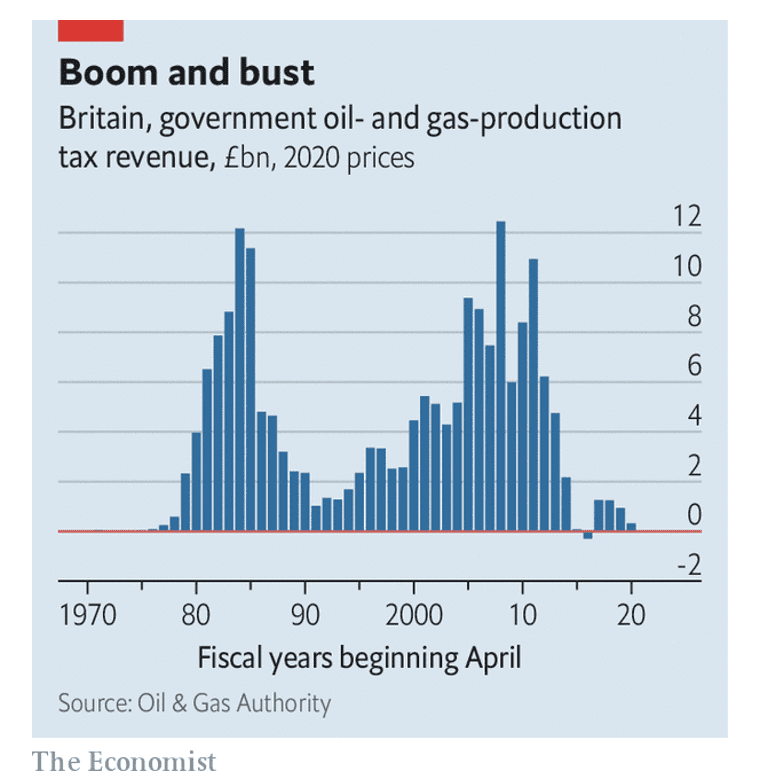

There is also no guarantee that the North Sea will continue to generate significant tax revenue into the future. If oil and gas prices fall, we will be back to the mid-2010s landscape, with decommissioning costs borne by the taxpayer if projects become uneconomic prematurely and companies are not forced to stump up the cash themselves.

Figure 2: Historic tax revenue from UK oil and gas[10]

Ensuring energy security therefore means ramping up renewables and energy efficiency – which can be achieved more quickly and will permanently cut import dependence – at the same time as supporting North Sea workers to find alternative jobs. Unfortunately, the government appears not to have fully appreciated this, with onshore wind developments still facing high planning barriers; a recent offshore wind auction resulting in no new projects because of the government’s unwillingness to make adjustments for current inflation; bottlenecks on grid and port infrastructure; and moves to block solar farms.

Future governments could increase costs

Those hoping to profit from further North Sea projects should keep another operational point in mind. Recent governments have bent over backwards to encourage companies to keep investing in the UK Continental Shelf, first through slashing taxes in the mid-2010s – when a price slump highlighted the North Sea’s vulnerability to volatile global markets – and now through a generous investment allowance. Future governments may be less kind, further threatening the profitability of developments.

In addition to a less sympathetic tax regime, a government may well introduce tougher regulations, such as on methane emissions, and refuse to shoulder so much of future decommissioning costs (estimated in 2019 to be £24 billion out of £45-£77 billion). Companies developing new fields may come to feel they have been led up the garden path in the future.

New licences are only one part of the story

Finally, while licensing has become a key focus of the debate, it is important to remember that this is only one piece of the puzzle. Projects like Rosebank already have production licences, and there could be many more to come given the large areas sitting under licences.

It is unclear whether Labour, who are current favourites to win the next election and have said they would stop issuing new licences to explore for hydrocarbons, would continue approving licensed projects or issuing “second term” production licences. A 1.5˚C-compatible policy would put an end to all new projects, not simply licences.

To conclude, stakeholders should do the following:

- Investors should challenge companies on the commercial viability of new projects

- Experts and the wider public should challenge policymakers on the climate compatibility of new licensing