The UK’s energy security strategy is back at the forefront of political debate.

As the government looks to show leadership on climate policy, it must also tackle two urgent and closely linked issues: rising energy prices and the country’s dependence on international energy imports. The next quarterly energy price cap will be raised by an eye-watering 80% at a time of rampant inflation, and Russia has demonstrated the impact major exporting nations can have on global energy markets.

Number 10 is banking on fossil fuels to address these problems. Liz Truss, favourite to be the next Prime Minister, is planning to award 130 new drilling licenses in the North Sea if she gets into office, according to media reports. Moreover, British Energy Security Strategy, updated in April 2022, places an explicit emphasis on further domestic fossil fuel production[i] and continued tax relief and subsidies for oil and gas companies. Even when public opinion encouraged a windfall tax, the Energy Profits Levy, announced in late May, includes a significant 80% tax break for new oil and gas investment in the UK.

Given the clear message from the IEA in 2021, that to reach net-zero in 2050, no new fossil fuel projects are needed[ii], climate leadership and new fossil fuel production are clearly incompatible. But will more domestic ’home-grown’ fossil fuels help alleviate energy costs or even improve wider energy security for the UK?

Domestic fossil fuels do not mean lower prices

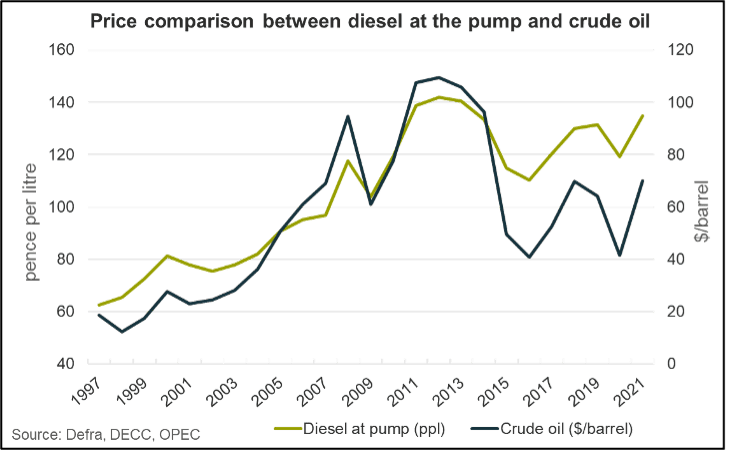

The price consumers pay for fuel at the pump is closely linked to the global oil price (Fig 1). Even if more domestic fossil fuels are produced in the UK, they will be sold to the highest bidder on the global oil market, and UK consumers will not see lower prices. For gas the situation is similar, even though the gas markets are more regional. After all, in the UK it’s the owners of the oil and gas – private and public fossil fuel companies – that will sell their products to their preferred market, which will be wherever the price is highest.

Figure 1: Correlation of global oil price versus UK diesel pump price[iii]. Approximate comparison, not accounting for fixed rate tax.

Fossil fuel projects take time

Could some quick drilling by fossil fuel companies solve the UK’s energy bill problems?

Messaging from the Cabinet has pedalled the illusion that more drilling will alleviate the energy crisis[iv], but to suggest that drilling more oil and gas will help solve these financial problems is avoiding the fact that projects often have significant lead times, typically 4 to 10 years for appraisal and development phases. Given that the UK needs more affordable energy right now, this really begs the question as to why the government is proceeding with another licensing round in the UK[v], and who will benefit from it. In contrast to fossil fuel projects, solar farms can be built in just weeks, onshore wind in months, and large 1GW-scale offshore windfarms in three years.

In addition to project lead time, much of the oil produced in the UK is not suitable for our energy needs (e.g., transport fuels) and as such, nearly 80% of the UK produced oil is exported. This means that oil from large projects West of Shetland in the North Sea (NS), like Rosebank and Cambo, will do little to provide UK consumers with fuel, let alone bring consumer prices down.

More diversification away from fossil is the key to energy security and price stability

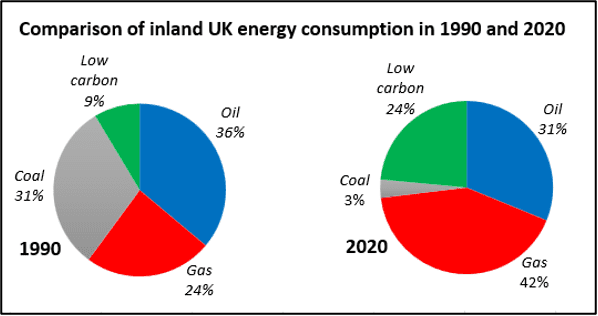

Although electricity generation from wind, solar and hydro has grown, the UK’s energy demands are still met predominantly from oil and natural gas (Fig 2). In total, fossil fuels make up approximately three-quarters of the UK’s energy mix; primarily gas and coal for generating electricity, gas for heating homes and oil providing fuel for transport[vi]. By expanding reliance on fossil fuels for the UK’s energy demands, government is not just failing to address the immediate energy crisis, but locking in a future of increasing exposure to global price volatility.

In contrast to fossil fuels, renewable energy is not exposed to the volatility of global markets. By diversifying UK energy away from fossil fuels and into renewables, prices will become more predictable. As will be discussed in the next section, increasing renewable energy will drive down consumer prices.

Figure 2: Comparison of UK energy source in 1990 and 2020, from UK Energy in Brief 2021[vii]. 2021 figures show <1% reductions to gas and coal, and <3% uptick in oil usage[viii].

Renewables costs are falling rapidly relative to fossil

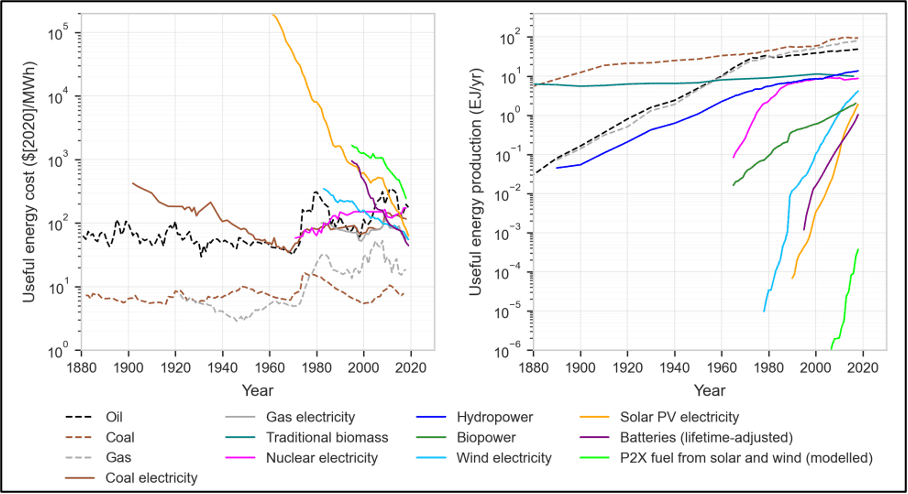

With the exception of periodic spikes, long-term fossil fuel prices have not changed that significantly for the last 100 years or so in real terms (black, brown and grey dashed lines in Fig 3, left chart). In contrast, the price of renewables has fallen exponentially and learning rates imply further cost reductions ahead. Solar energy costs have decreased by more than three orders of magnitude since first commercial use (yellow decline line in Fig 3, left chart), driving the 1,000 x growth in solar energy production (yellow line in Fig 3, right chart) since 1990.

Figure 3: Historical costs and production of key energy supply technologies (from Way et al, 2021)[ix]

That renewables costs are rapidly declining is yet another reason Britain should be prioritising renewable energy investments over fossil fuels. In fact, investment into renewables in the UK, supported by green levies, has already helped reduce energy bills, and had some climate policies (such as the zero carbon homes plan in 2015, and onshore wind in 2016) not been cut over the last 10 years, prices now would not be so high[x].

However, even if oil and gas projects could be sanctioned extremely quickly, and accepting that it would have little impact on consumer prices, could they deliver returns to the UK exchequer?

UK taxpayers picking up bill for encouraging continued investment in new fossil fuels

In a series of reports over the years, Carbon Tracker has shown the growing exposure of companies and their shareholders to stranded asset risk, as demand for oil and gas drops through the energy transition, and cash flows fall. Carbon Tracker has also shown how these same drivers can impact government revenues from oil and gas in Beyond Petrostates[xi].

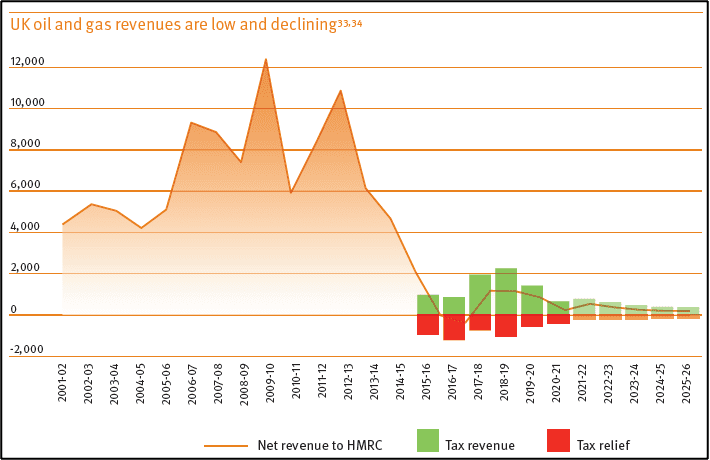

The UK oil and gas industry was once a source of major UK revenue, but that situation changed around the time of the 2014 oil price drop, when profits via taxation plummeted (Fig 4). To revitalise investment in the basin, significant tax relief and subsidies were introduced – for example, the Petroleum Revenue tax was cut and the Supplementary Charge tax was reduced – and consequently the Government made a loss from the industry in 2016 to 2017[xii]. In propping up a deteriorating fossil fuel market, No 10 is placing the country highly vulnerable to future revenue stranding.

Figure 4: Historic and forecast Government revenue from UK oil and gas industry[xiii]

The same risk and principle of asset stranding can be applied to the government’s generous decommissioning tax relief commitments in reverse, with the risk being placed on the taxpayer. In addition to revenue losses, around 40% of decommissioning costs in the UK will be paid indirectly by UK taxpayers[xiv]. This means that for every oil and gas project sanctioned, the government is committing capital to the continued long-term success of the industry. Commodity prices aside, this presents a deteriorating forecast given that decommissioning activity is increasing, and production rates are falling.

In recent years the UK has seen many large IOCs exit, usually selling up portfolios to privately funded UK specialist firms. But for many companies, such as BP and Shell, the UK remains a core region. Given the growing exposure of companies and their shareholders to stranded asset risk, described above, the UK presents a particularly dangerous investment. This is because in addition to transition risk, if tax reliefs and subsidies are withdrawn, the UK would be less economic and shareholder returns would be negatively impacted. So it’s not just the UK Government that needs to pull the plug on fossil fuels; if companies are acting in the best interest of their shareholders, they too need to think very carefully about new investment into UK fossil fuels.

UK at a critical juncture

The UK is at a political cross-roads in determining the future of its energy security, with major implications for consumers and the country’s ability to deliver on climate goals. Key points and recommendations are as follows:

- To improve energy security, the UK government must act to reduce its reliance on fossil fuels, rather than incentivising further development. By reducing fossil fuel reliance, consumers will become less exposed to the volatility of global oil and gas markets and associated price spikes.

- Increase investment into renewable energy sources through continued use of successful green levies but also more effective taxation on the oil and gas industry. This will continue to help reduce costs to consumers and improve longer term energy security.

- With the UK oil and gas market so heavily propped up by tax reliefs and subsidies, more drilling will increase the risk of job and asset stranding. Currently, the UK taxpayer will pay for 40% of UK oil and gas decommissioning. This will continue to grow with more drilling.

- For companies and their shareholders, new investments may not deliver adequate returns as medium-term prices fall combined with the growing risk of the withdrawal of Government tax relief and subsidies.