Oil and Gas company narratives about the future of fossil fuels remain positive, their bank accounts are full.

But their strategies show they are not investing much in their own assets or in renewable energy.

Their strategies show they recognise how risky new long-term fossil-fuel investments will be: leaving them now strategically stranded whether they invest heavily in oil and gas, or quietly retreat from it.

Oil and gas buyers beware.

We focus on two key Carbon Tracker reports this month that cover this theme in detail:

- Avoiding Stranded Assets

- Absolute Impact 2023: Progress on oil and gas emissions targets has stalled

These two papers say two big things backed up by data and details:

Oil and gas companies despite talking about lack of investment, have large windfall profits they are not investing in capital assets.

This indicates their real worldview: demand is lowering, long-cycle investment is too high risk, the fossil fuel world will now turn to squeezing returns from existing assets, and those run by the lowest-cost producers (spoiler, OPEC) as supply outpaces demand with renewables accelerating globally.

Rather, their bank accounts are being used to pay down debt, increase dividends and buy their own shares: new production is not a priority despite their comments on energy security.

Oil and gas companies are not meeting Paris climate goals and are only investing at the margins in new energies such as wind and solar.

They will not lead an energy transition, they will seek instead to maximise their returns in their declining demand markets, and largely ignore global emissions targets and pass that effort by default to new energy firms.

They will be laggards in the transition, not at the head of it.

Quelle surprise – as Carbon Tracker has noted a number of times.

Carbon Tracker has raised these issues many times – and these latest two papers show again how these themes are playing out and what it means for investors.

The stranded asset theme we have proposed for many years is increasingly forcing rethinks at a corporate level – and as we noted, the power of such an idea has stopped un-needed assets being created: leading to CO2 unemitted, and investor cash secured.

Please contact us if you wish to discuss in any more detail at info@carbontracker.org

Energy Monitor – two key papers

The first paper – Avoiding Stranded Assets looks at how, despite bullish claims by the oil and gas industry that oil demand is robust, their actions suggest they believe the opposite.

The second – Absolute Impact 2023: Progress on oil and gas emissions targets has stalled – shows that effectively none of the international oil and gas companies are anywhere close to meeting Paris 2015 pledges on oil and gas transition, or spending on alternative energies.

Taken together, this shows oil and gas firms recognise that useful oil and gas demand growth is over (whether a peak or not, economic growth is gone) and they have no credible plans or perhaps even the desire to transition to any other form of business model and help the energy transition and lower emissions.

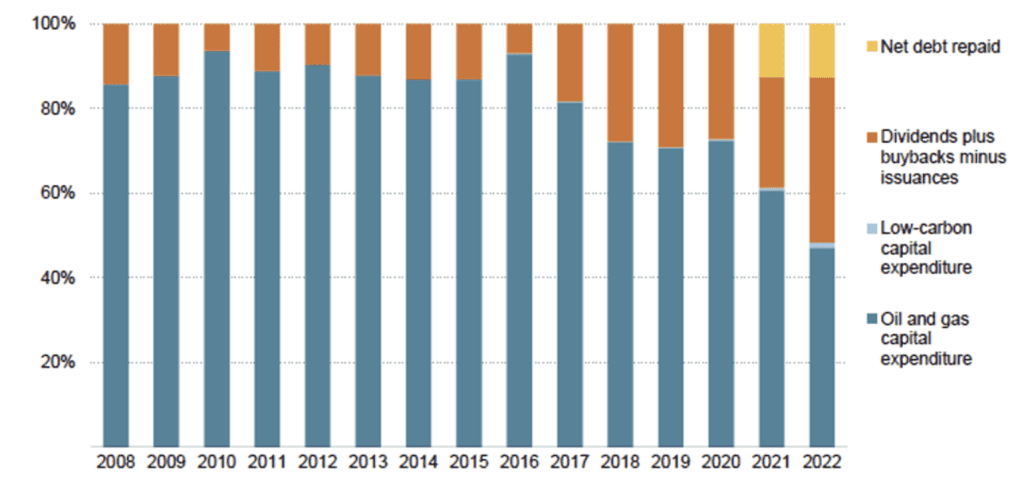

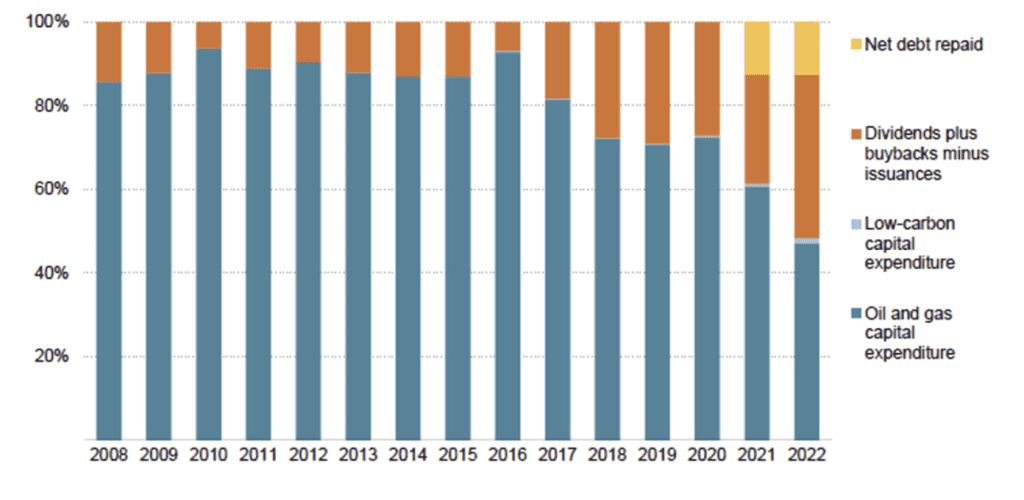

If you do nothing else, please look at this chart from the first paper that shows the reality of oil and gas investment and – importantly – non-investment over the last 14 years.

Today the majority of cash spending by oil and gas companies is not into new assets, or renewables: it is recycled as dividends, debt pay-down and share buy-backs.

In other words, despite bullish noises from the sector, and its bankers, they are in harvest mode.

This is the key take-away from this month’s Monitor – and the finer details are outlined below.

We are not stating at Carbon Tracker that we have caused this decline in carbon-emitting asset investments: but we do confidently declare that we have played a part in it.

Numbers are crucial: words are critical. We do both, as we discuss below.

Distribution of cash spending by the oil and gas industry (2008-2022), reproduced from IEA

Source: IEA (World Energy Investment 2023)

Oil and gas companies are not investing that much in oil and gas, or the alternatives

Carbon Tracker has long-warned of the risk of investing in future oil and gas stranded assets; i.e., assets that fail to generate the returns expected when sanctioned. And create un-needed emissions which cause long-term planetary costs.

Carbon Tracker has therefore advocated that the oil and gas industry should take a more cautious view of the future – rather than its typical engineering zeal to build projects that it can, rather than those it should – and to avoid a massive emissions overhang that will take far more effort to solve than create.

Yet some high-profile analysts and banks are advocating that the industry should return to its old high-investment ways in the name of energy security.

However, many oil companies are resisting the investment urge – for the simple reason that increased demand is not there.

It is a somewhat cynical response from the industry to raise energy security as a major issue and then not invest significantly in new supply, but mainly in financial improvements to their own balance sheets and profits. In the short-term – but as note with increasing short-medium term high risk to investors.

Since 2014, Carbon Tracker has highlighted the potential risk to oil and gas projects that are sanctioned without allowing for the impact of climate policy and the substitution effects of renewable technology development.

Carbon Tracker has considered a range of demand profiles from energy transition scenarios corresponding to temperature outcomes of 2°C, and 1.5°C (low overshoot [1]).

The risk from lower future demand is that long-term commodity prices are lower than anticipated, and thus many projects would fail to generate an economic return becoming “stranded.”

Clearly this would result in a marked fall in returns for shareholders. This was exactly what happened after 2014 following the industry capex-binge between 2010-2014. See Exxon note.[2]

In response, Carbon Tracker has advocated that the oil and gas industry should take a cautious view of the future.

Management should impose higher hurdle rates to compensate for increased risk, with capital expenditure limited to only the most cost-competitive projects.

And indeed the industry is resisting investment in new assets despite recent high prices

Instinctively the oil and gas industry now see now long-term asset building as an investment in complicated, expensive and hence ultimately stranded projects – leading to a very large, and possibly quick, increase in balance sheet liabilities.

OPEC has responded to this for years: its production levels in 2015 were 36 million barrels per day: after 8 years of production cuts (to preserve prices) production is 34 million barrels per day in 2023 – a 6% decline: not the actions of an industry that expects robust demand growth or the need for supply security.

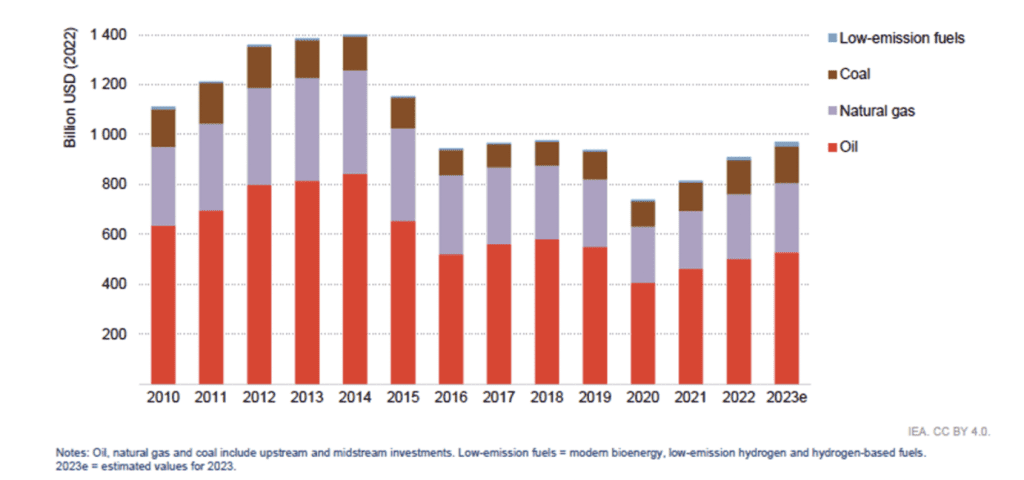

Looking wider at the global picture for oil capex, from the IEA’s World Energy Investment 2023 report, it is evident that total capex has been subdued since 2014 through 2022, although partially rebounding, as noted by Goldman Sachs.

But even based on Goldman Sach’s subset of global data (the Top 70 giant projects) it shows that oil development capital spending almost certainly peaked in 2014-15.[3]

Which makes sense if forward demand is now declining – investing in 20 year-long projects when demand is booming is a classic commodity profit story: investing when growth has gone, and the projects are getting more expensive is a classic commodity stranded and loss story.

Global investment in fuel supply, 2010-2023e, reproduced from IEA

Source: IEA

In explaining the post 2015 and post 2019 falls in capex, Goldman Sachs point to the role that decarbonisation constraints and ESG issues have put on investor and finance thinking. “The energy industry has been so risk-averse in the last few years, and under such tremendous pressure from decarbonization to not invest.”

Goldman Sachs sees this as “underinvestment.”

They are misguided.

In Carbon Tracker this “underinvestment” is seen as prudent risk management: as the IEA shows it has been dividends and not capex that has been the major recipient of company cashflow.

Industry capital spending is now 30-40% below its peak in 2014, and unlikely to ever reach those levels again.

In addition, oil and gas industry investment in green energy has also been very low despite the free cashflow that was available: the second paper we discuss below goes into this in more detail.

So new energy investment is not their aim either. So, what now is the point of oil and gas company investment?

Harvesting it seems.

Distribution of cash spending by the oil and gas industry (2008-2022), reproduced from IEA

Source: IEA (World Energy Investment 2023)

Taken together these financial realities suggest that the oil and gas industry has used recent windfall profits to not invest in energy security: but to invest in corporate financial restructuring, pay dividends, lower debt and increase share buy-backs.

Lower investment in core oil and gas, minor investment in new energy, recycling cash.

In summary: harvesting and exit from high-risk, likely-stranded assets.

Our decade long message from Carbon Tracker hitting home.

The oil and gas industry therefore appears to see the energy world ahead as reduced fossil fuel demand, and increased renewables, which is a world where their role is to maximise current asset return, and use cash for other purposes such as dividends.

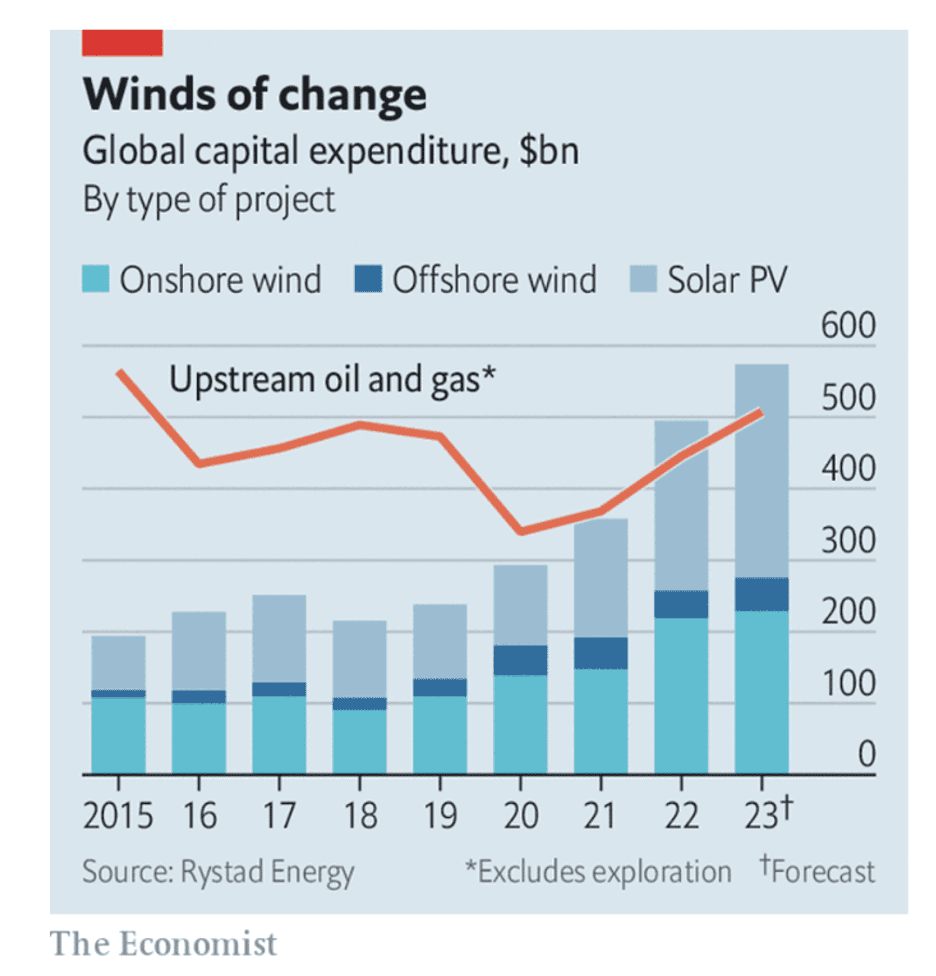

Indeed, in 2022 as we noted in a previous monitor, global investment in wind and solar on an absolute capital basis, and more so on an energy unit basis, overtook oil and gas investment for the first time.

Energy now has many options for investments: oil and gas management has awakened to this fact

Indeed, if the pre-2014 boom exuberance had continued, there would likely have been even more oversupply, and investor harm – and that case remains the same today even though Goldman Sachs seems to believe the opposite.

It vindicates the benefits of investor caution based on analysis carried out by Carbon Tracker.

Thankfully for the planet the oil and gas industry have decided to cede to the economic logic, and meme of stranded assets we developed, and have decided not to put that cash into long-term risky assets.

The lowest-emitting, lowest-risk oil and gas asset is the one that will not be built, as we propose and that the IEA acknowledge.

Despite the siren calls of investment bankers.

Where to from here – OPEC Returns?

We argued in Managing Peak Oil, that the industry should be very cautious about committing to new long cycle projects, as demand would be peaking out and starting to decline before the end of this decade [4].

We pointed to short cycle projects as less risky.

Recent industry investment behaviour has corresponded to these risks and as even Goldman Sachs notes recent capex has been short cycle: “Most of the capex growth last year was driven by U.S. shale. It was clearly a U.S. onshore-led capex recovery.”

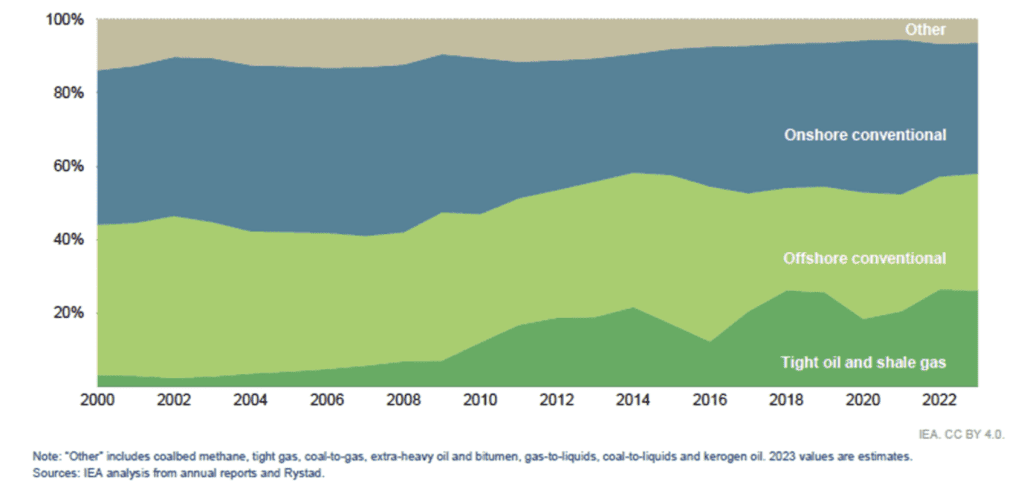

Share of oil and gas investment by asset type, 2000-2023e, reproduced from IEA

Source: IEA

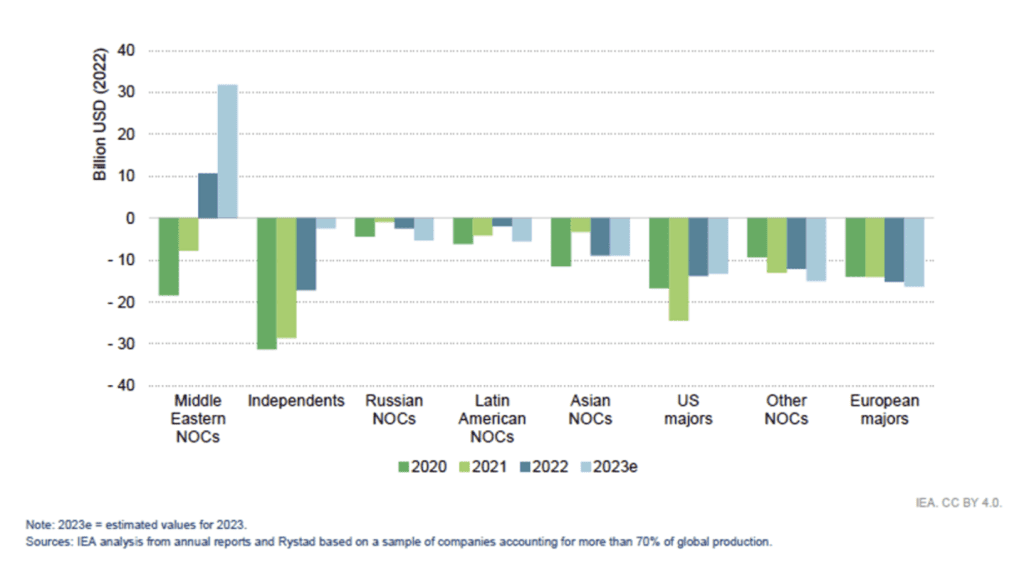

But in the longer-term, it has been those firms least exposed to capital market pressures that have invested most in a business-as-usual way: according to the IEA, it is Middle Eastern National Oil Companies that are raising capex the most.

Change in upstream oil and gas capital investment relative to 2019 by company type, 2020-2023e, reproduced from IEA.

Source: IEA

This likely means over time as capital reduces in the industry overall, but OPEC NOCs continue to invest, their share of global production will rise, as the IEA predict.

That may mean their hold on oil prices could continue.

Increasing risk means hurdle rates should rise, not fall

Following the Ukraine War and a gradual recovery in oil demand post covid, with prices at $70-90/bbl, Goldman Sachs argues the hurdle rate for new investment will need to fall from 20% to 15% to generate supply expansion.

We disagree.

If anything, industry hurdle rates (cost of capital) should be staying up, not go down.

We see no reason for the industry to move to a lower hurdle rate: hurdle rates in an industrial sector should be set by macro-economics and fundamental of demands – not wishful thinking from fund manager playbooks.

Were industry to lower hurdle rates, we believe it would lead to an increased risk profile for oil and gas portfolios because it would encourage investment in higher cost, lower return assets that are not needed, yet would be operated at a loss creating more emissions, and lower investor returns: stranded, but emitting, the worst of both worlds.

Maintaining high hurdle rates is rational and avoids all that complexity and risk – literally at the stroke of a pen.

In sum: Don’t invest for the long term based on short-term signals

This is a recipe for deteriorating investor and shareholder returns. This is exactly what happened post the 2010-2014 investment binge, which led to underperformance by Big Oil and the ejection of ExxonMobil from the S&P500 and the Dow Jones.

Given tight conditions at present, the oil industry may get its $80-100 oil price dream in the short term.

But how long might that last?

Our second paper this month tackles this question.

What is the point of oil and gas company investment now?

If investment in core commodity oil and gas production is declining – perhaps investment in new energy options is an alternative.

But global energy does not seem to work that way.

Diverting capital at vast scale from extraction of oil and gas and into the manufacturing of for example wind and solar and batteries is not trivial, it is incredibly complex.

And almost certainly cannot be done by single energy corporations – it needs new entrants with technical skills distinct from incumbents.

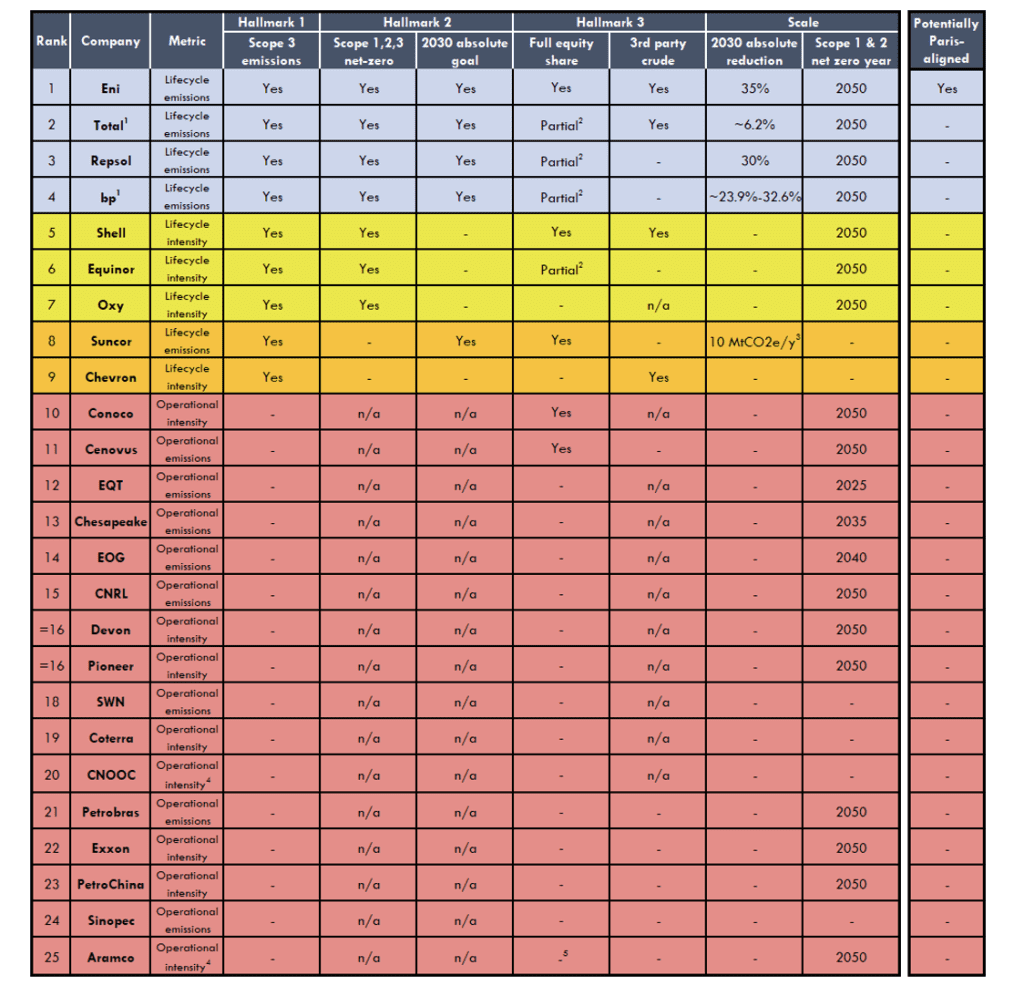

Aligned to the blog piece above – Carbon Tracker launched the 4th edition of our Absolute Impact series, in which we assess and rank the climate goals of some of the largest publicly traded oil and gas companies.

To set the scene: emissions are a direct measure of waste and inefficiency.

The more you emit the more you put waste into the air, and the less efficient your operations are.

Oil and gas combustion creates CO2 and other pollutants such as NO2.

Only about 40% of fossil fuels are used directly in useful things such as heat, light and transport: the rest, 60%,flows into the atmosphere around us as heat and pollutants.

An oil and gas firm not committed to reducing scope 1 and 2 emissions – those directly created by their operations e.g. oil and gas exploration, or refining, is not focussed on emissions control and climate risks.

But it is also not focussed on corporate efficiency and profitability.

And a management that does not target scope 3 emissions, those created by its products e.g. gasoline emissions, is not recognising a key metric for structural changes in future demand.

A company not setting interim emissions reduction targets is betting that any threat to profitable demand is a long way off.

And a company that is using unrealistic offsetting targets is doubling down on that approach.

Let us delve deeper into how oil and gas companies are really approaching global climate goals (rather than just accept corporate advertising).

To get the key point: the report found 24 of 25 large oil and gas companies have emissions goals that are not aligned with Paris commitments.

These goals can be used as a key indicator for how companies are responding to the dual threats of global warming and the energy transition.

Even as pressure mounts to meet the goals of the Paris agreement and conversations evolve about energy security and new technologies, the fast-growing new energy system is expanding at speed and accelerating the decline in demand for oil and gas.

In its World Energy Investment 2023 report, the IEA show that less than half of the industry’s cashflows are going back into traditional supply, as opposed to over 80% a decade ago – a foreshadowing of fossil fuel decline that we have already reviewed

To summarise:

- 24 of 25 of the world’s largest oil and gas companies have emissions goals that are not considered Paris-aligned when assessed against our three Hallmarks of Paris-Aligned Emissions Targets.

- Progress on emissions goals set by oil and gas companies has stalled – some have gone backwards since our previous analysis.

- As demand for fossil fuels weakens through the transition, this analysis shines a light on the pace at which companies see the transition unfolding. Investors seeking to screen companies for transition risk exposure can use this analysis to complement analysis of investment and production plans.

- Asset managers and banks seeking Paris-aligned portfolios can use this analysis to assess corporate positioning on climate.

This report, Absolute Impact 2023

- Shows you which management is preparing itself for a different future and which is not.

- Is designed to be used in conjunction with other investor bespoke screening methods to monitor existing investments or pick out future ones.

- Will provide investment and engagement teams questions to ask your current or target management teams.

- Should help compliance and C-Suites navigate the threat of falling foul of “greenwashing” claims against the marketing of your sustainable products.

A summary table below evaluates, company by company, the lack of progress on key climate milestones. It is a systemic issue in an industry that seems to view these targets as either too difficult and costly, or marginal to today’s priorities. Perhaps both.

Please read the report, study the tables, but the issue is clear.

The oil and gas industry will not lead the energy transition, but by its inaction will be led by it, as have many commodity sectors before such as fellow-traveller coal.

It has had many chances to reform, and taken few of them, as Carbon Tracker has indicated in previous reports.

Perhaps this is because of corporate strategy. Perhaps because the shift to non-fossil energy and into renewables is just too complex: as in assuming car firms can start to be expert aviation companies.

Whatever the case the two reports show clearly that oil and gas companies have started to re-invent themselves as cash-generating machines, rather than leaders of a new energy sector.

Stranded by strategy.