As the Colorado Oil and Gas Conservation Commission (COGCC) evaluates operator bonding proposals, and goes through hearings on the plans today and for the next few weeks, a clearer picture of the state’s financial assurance regulations is emerging.

The COGCC has touted their rules as the “strongest in the nation,” but it is clear that the financial assurance required will fall short of what is required. How far short depends on whether some of the most insufficient operator proposals are endorsed.

COGCC Director, Julie Murphy, acting on staff recommendations, has denied several of the most egregiously low bonding proposals, but the commissioners will have a final say. [1]

The bird’s eye view on operator proposals—a long way away from full bonding

First, the seemingly good news; for the operators who have submitted Form 3 plans detailing their proposed bonding to date[2], the overall financial assurance will go up slightly in year one.

The problem is that this is well below both what is presumptively required from these operators under the new rules, and even further below the amounts required to ensure Colorado is protected, should they default.

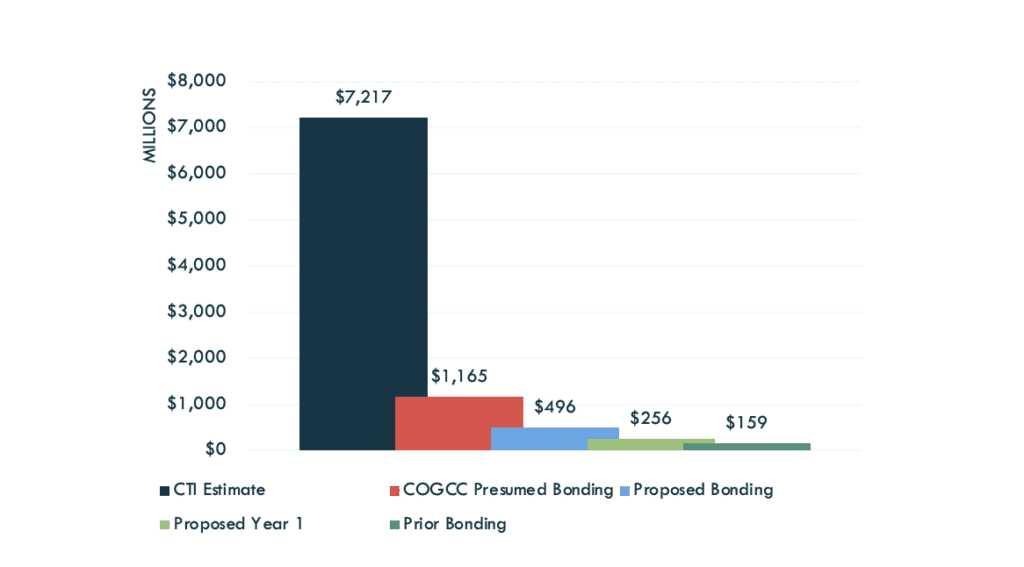

The presumed bonding for these operators would have seen them increase their total bonding from the existing $158,588,039 to $1,165,277,082, a ninefold increase. This amount is far below what Carbon Tracker has estimated all wells would require—an amount of approximately $7.2 billion.

However, operators are proposing far less than this presumed amount. To date, 58% of operators representing 93% of unplugged wells have proposed to fund an amount of $495,570,884 over a twenty-year period, with only $256,017,177 in year one (52%).[3] This represents a modest increase in funding in year one, from 2.2% of what’s needed to 7.4%.

Figure 1: Comparison of CTI’s plugging cost estimate with the presumed bonding, proposed bonding, and existing bonding[4]

Riskiest operators want to pay the least

Table 1 shows the enormous discrepancy between presumed and proposed bonding across the options. The aggregate bonding increase compared to the existing bonding is principally driven by large operators filing large blanket bonds. These operators with higher production values account for all of the year one increase. Meanwhile, some of the operators with low average production—COGCC’s primary measure of risk—are proposing extreme reductions compared to presumed costs and to such a degree that their bond coverage will be less in year one than it is currently.

Table 1 – Proposed financial assurance based on presumed plan

| Plan Option[5] | COGCC Presumed Bonding | Proposed Year 1 Bonding | Percent of Presumed Bonding | Existing Bonding | Proposed Year 1 Bond Change |

| Option 1 | $183,509,333 | $194,090,333 | 106% | $123,809,497 | $70,280,836 |

| Option 2 | $110,035,364 | $39,471,500 | 36% | $6,668,442 | $32,803,058 |

| Option 3 | $609,370,000 | $13,436,092 | 2% | $13,742,700 | ($306,608) |

| Option 4 | $262,216,385 | $8,923,251 | 3% | $14,307,400 | ($5,384,149) |

As explained in Feet to the Fire operators are classified under Options 1 through 4 based on their production values. The highest producers fall under Option 1, with production values shrinking as the options go down. The average production of an Option 3 operator’s well places it under stripper well status[6]. Operators under Option 4 have an average daily per well production below 2 barrels of oil equivalent (BOE), a level of production that is considered uneconomic.[7] Under Options 3 and 4, operators are required to contribute financial assurance annually to cover their bonding, rather than provide it all at the outset. Option 3 operators have 20 years and Option 4 operators have 10 years to fully fund. Twenty-six operators have filed under Option 5 and asked for different funding periods, with one operator requesting 40 years. [8]

The overall increase in bonding does not appear to address the orphan risk from high-risk operators which operate low-producing wells. The bonding provision in Table 1 shows Option 3 and 4 operators, the highest risk operators, will have a decrease in bonding in the first year compared to their existing bonding. In fact, out of 194 operators who have submitted their Form 3s, 117 will provide COGCC with less financial assurance in the first year than COGCC currently holds from them.

One example is O’Brien Energy Resources. This operator is asking for a $40,000 reduction compared to their current bond with an Option 5 proposal that would blanket bond their wells rather than the single-well financial assurance (SWFA) for all wells required in Option 4.[9]

Table 2 – Presumed vs. Proposed vs. Existing Bonding by Option

| Plan Option | COGCC Presumed Bonding | Presumed total bonding per well | Proposed Year 1 Bonding | Proposed Year 1 bonding per well | Existing bonding | Existing bonding per well |

| Option 1 | $183,509,333 | $7,085 | $194,090,333 | $7,494 | $123,809,497 | $4,780 |

| Option 2 | $110,035,364 | $23,833 | $39,471,500 | $8,549 | $6,668,442 | $1,444 |

| Option 3 | $609,370,000 | $111,975 | $13,436,092 | $2,525 | $13,742,700 | $2,469 |

| Option 4 | $262,216,385 | $119,189 | $8,923,251 | $4,056 | $14,307,400 | $6,503 |

Table 2 shows that in spite of being required to provide SWFA for all wells, with COGCC’s presumed costs between $110,000 and $140,000, Option 4 operators have managed to see an average of $4,056 in per well bonding in the first year. This amounts to less per well coverage than currently exists for these risky operators and is far below what COGCC has estimated it will cost them to plug the wells. Option 3 operators come in even lower at only $2,525 per well. These numbers are orders of magnitude smaller than estimated plugging costs, even though these operators are considered to be the highest risk. They are also lower on a per well basis than the presumably less risky operators.

Will the multi-decade funding arrangements be too little, too late?

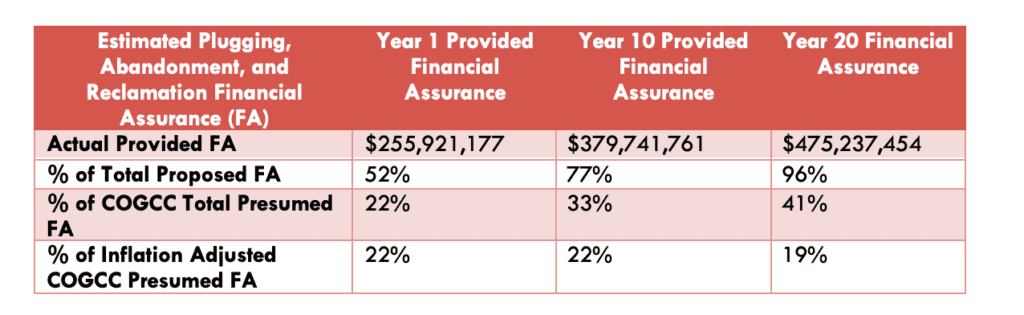

The foregoing discussion has ignored a critical gap in the rules, the timing of payments. The rules give Option 3 and 4 operators 10 or 20 years to fulfil their bonding obligations. While the COGCC might tout an increase in coverage to around $495,474,884, it will not receive that total. Not immediately anyway. At best, that will be funded over 20 years. That means that in the first year, assuming all plans were approved (which is not yet the case), COGCC would have only $255,921,177, with a total of 117 out of 194 operators actually providing a total of $60,758,082 less in financial assurance in year one than they currently have with COGCC, [10] contrary to the intent of SB-181 and the rules themselves. Financial assurance provides an incentive for operators to plug the wells, if approved these bonding reductions may well have the opposite effect.

What’s worse, the rules allow operators to fund their required bonds over multiple decades but fail to include any adjustment for inflation. They merely include an option to consider it in annual reviews.[11] The table below shows, using a 3.8% inflation rate, what the inflation adjusted amount of financial assurance should be in order to keep the same purchasing power as today.[12] By 2042, the end of the 20-year funding period, COGCC would need to have around $1.0 billion to be equivalent to $495,474,884, which again is not the amount they will have at the outset (nor at year 5 or year 10). This year, if all plans had been approved, COGCC would have $255,921,177 in the bank this year.

As of March 31, 2023, some plans have been denied but time will yet tell what changes are made to the amounts of those denied plans. Regardless, if proposals are unadjusted for inflation over the next 10 or 20 years, the plans will fall vastly short, 59% short of the presumed financial assurance today and 81% short of the inflation adjusted presumed financial assurance.

Table 3 – Financial assurance over time

Interestingly, COGCC acknowledged the recent increase in the cost of goods and services in recent years when rejecting Wiepking-Fullerton Energy’s proposal. The invoices submitted were from 2018 to 2021, which led COGCC to comment “The Operator has provided no documentation to indicate how prices might differ/increase from those provided in invoices based on recent, widespread increases in the price of goods and services.”[13] If COGCC can acknowledge that costs have increased in the past 3 years, it seems intuitive to build in an assumption that costs will continue to increase, using even a conservative estimate of inflation to ensure that costs are covered over the duration of these plans.

COGCC staff are rejecting low-ball bonding proposals—will the Commission do the same?

There are structural weaknesses in the rules themselves, but some of this can be remedied by an engaged regulator.

Why are many operators’ proposed financial assurance plans coming in so much lower than COGCC’s rule based presumptive amounts? There are a few reasons.

First, operators can simply apply for an Option 5 plan, allowing them to offer coverage that suits their needs. Almost invariably, companies are proposing far less financial assurance.

Second, rather than require companies to provide assurance to cover what Colorado expects it would have to pay (a proper yardstick for the risk to the state), it has allowed companies to provide their own estimates under the guise of “demonstrated costs.” A definition of “demonstrated costs” is conspicuously absent from the rules.

The COGCC’s willingness to accept “demonstrated” costs could yield perverse results. Rules aimed to increase financial assurance will actually decrease it for some of the riskiest operators, via Option 5 proposals and low “demonstrated” costs.

However, COGCC staff have rejected 10 of these proposals[14], including KP Kauffman and Omimex Petroleum, whose proposals Carbon Tracker reviewed previously.[15] These proposals were rejected because they failed to credibly demonstrate that those operators could plug, abandon, and reclaim wells for a fraction of the estimated costs under the rules. Whether the Commissioners also force these operators to provide evidence is now up for debate.

The impact of KP Kauffman and Omimex Resources using COGCC estimates rather than their own costs would be critically significant for improving the average bonding of Option 4 wells, considering those two operators hold 1,428 of the 2,200 Option 4 wells that are currently accounted for with filed Form 3s.

It is therefore important to highlight the significance of COGCC’s denial of proposed plans. Of the 10 rejected plans, four were Option 4 plans and the other six were Option 3 plans[16]. When rejecting plans on the basis of the proposed demonstrated costs, the notice of decision stated that “the Director will ask that the Commission enter an order requiring the Operator to implement the plan as submitted in the above referenced and attached Form 3 without Demonstrated Costs.” If the Commission supports staff and orders these operators to propose plans using COGCC’s costs, the bonding from these 9 operators alone will increase from $35,188,547 to $258,001,400, an increase of $222,812,853.[17]

In their denials of these plans, the COGCC staff made some key comments as to why plans were denied. The most common issue was insufficient support for demonstrated costs. This covered both operators who submitted “all but nonexistent” evidence or evidence that had “not addressed many of the aspects listed.”[18]

KP Kauffman’s demonstrated costs were put through the wringer, but one incredibly important piece stood out. In the Demonstrated Cost Review, it was written “deflated costs are not appropriate to determine the amount of Financial Assurance required for the state or a third party to pay market rates to plug and abandon stranded assets.” If this philosophy is applied to all operators, this means that operators cannot simply use the costs they themselves would spend on decommissioning but instead must provide financial assurance to cover the costs the state would incur to decommission the operator’s wells should they become stranded. This is the appropriate yardstick since financial assurance is intended to protect the state and its taxpayers.

Own Resources will be in the spotlight

As hearings continue, denying plans with vague and incomplete evidence of their costs and undeserved low bonding for high-risk operators will be crucial to protecting the state from decommissioning costs.

Perhaps the most prominent example of such a proposal that deserves the same level of scrutiny as these denied plans is Own Resources. They have proposed an Option 5 plan, though by production they would fall under Option 3. Their Option 5 proposal would see them provide a mere 2% of what is presumed by COGCC costs. Rather than the $338,460,000 that was presumed by COGCC, Own has proposed $8,306,200, a difference of over $330 million.

They used several cuts to get this lowered amount. First, they included a blanket bond for most of their wells, something not allowed under Option 3, with coverage of $700 per well, a lower rate than even the largest, highest producing operators are given. Secondly, they used their “demonstrated costs” for significantly reduced single-well bonding requirements. Finally, Own seeks to redefine a low producing well for SWFA purposes at less than 2.5 MCFE per day as opposed to 10 MCFE per day under the rules.

Conclusion: Proof will be in pudding

With the riskiest operators building their own Option 5 plan or proposing low “demonstrated” plugging costs for bonding coverage, and a Rule that allows multi-decade funding but does not mandate inflationary adjustments, the “strongest in the nation” rules display real weakness. However, the COGCC can turn this around, ensuring risk is not rewarded, by rejecting plans like they have already done that fail to meet the standards and intent of the rules.