This note responds to claims made by Exxon Mobil (Exxon) in a Schedule 14A Additional Definitive Materials and Rule 14(a)(12) material (Filing) relating to a shareholder resolution filed and lead by Legal & General Investment Management America, Inc. (LGIMA) and Christian Brothers Investment Services, Inc. (“CBIS” and together with LGIMA, the “Proponents”).

Some of the Proponents’ submissions reference Carbon Tracker Initiative’s (Carbon Tracker’s) analysis related to that resolution as well as other pieces of Carbon Tracker’s research and analysis of Exxon’s disclosures and corporate strategy.

We address Exxon’s arguments at the end. We would submit that these challenges are largely irrelevant to the question of whether Exxon should provide an aggregate assessment of its total potential asset retirement obligations (AROs) as sought by the Proponents’ resolution.

At root, this is about differing views as to the pace of the energy transition and its impact on the value of assets and timing of liabilities for companies like Exxon that are committed to further hydrocarbon production. Proponents have, in essence, asked Exxon for a sensitivity analysis relating to the potential for accelerated fossil fuel asset retirements. For its part, Exxon does not believe such information is useful or necessary because it views the prospect of the world meeting its climate targets as remote and contends that, generally speaking, its refineries could be repurposed and continue operating. The question that investors will vote on this proxy season relates to whether, notwithstanding its convictions, Exxon should provide these sensitivities to its investors.

About Carbon Tracker

The Carbon Tracker Initiative is a not-for-profit think tank focused on the financial implications of the energy transition for fossil-fuel intensive industries. For over a decade, Carbon Tracker has provided analysis of these implications to a range of interested parties, including investors. This analysis has included a range of assessments of whether and to what extent integrated oil and gas companies like Exxon are considering the financial risks of the energy transition in their financial statements.

The Paris Agreement and related scenarios

The Paris Agreement calls for reducing global warming to “well-below” 2 degrees Celsius, with then ambition to achieve less than 1.5 degrees Celsius warming. It has been signed by 196 parties, primarily governments, and virtually all major industrialized nations.

Recognized international bodies such as the International Energy Agency (IEA) have modeled the energy implications of the Paris Agreement through forward-ranging scenarios such as the “Net Zero Emissions by 2050” scenario (NZE), which envision precipitous reductions in fossil fuel usage over the next several decades.

Some investors have sought to understand how companies such as Exxon are planning for such an outcome, how they are integrating these material risks into their financial reporting, and how that financial reporting might change were the company to integrate such scenarios.

These inquiries have sought information that goes beyond management’s views on likely scenarios and asks firms to provide sensitivities to cases in which the world decarbonizes at a pace commensurate to the world’s climate goals. This is of particular importance for companies such as Exxon which, “do not incorporate into our financial statements those types of risks that are as remote as the IEA NZE path.”[1]

While Carbon Tracker considers the energy transition broadly, some work also addresses questions around whether a company’s financial statements have considered the impact of the transition and/ or corporate emissions reductions targets, the implications of meeting the goals of the Paris Agreement, and whether corporate reports have provided the information sought by investors.

Shareholder resolution filings

This year and last, investors filed resolutions at Exxon seeking information on how the energy transition would impact the company’s financial statements.[2] In effect, both resolutions seek information on how, in a low carbon scenario like the NZE (that Exxon currently believes is unlikely to transpire), Exxon’s existing asset base (and related liabilities) would be impacted. Importantly, neither resolution requires or even asks the company to change its current accounting practice.

While our principle focus here is on the resolution currently on Exxon’s proxy for this year, for context we discuss both.

For the 2022 proxy, a majority of Exxon’s shareholders supported a resolution (2022 resolution) calling for the company to analyze the impact of the NZE scenario on relevant items in Exxon’s financial statements:

Resolved: Shareholders request that ExxonMobil’s Board of Directors seek an audited report assessing how applying the assumptions of the International Energy Agency’s Net Zero by 2050 pathway would affect the assumptions, costs, estimates, and valuations underlying its financial statements, including those related to long-term commodity and carbon prices, remaining asset lives, future asset retirement obligations, capital expenditures, and impairments. The Board should obtain and ensure publication of the report by February 2023, at reasonable cost and omitting proprietary information.[3] (emphasis added).

For the current 2023 proxy, shareholders have focused on a specific dimension of Exxon’s financial reporting—its asset retirement obligations (AROs). These are obligations associated with the retirement of tangible long-lived assets.[4]

Many of Exxon’s assets have AROs, and Exxon records these obligations on a discounted present value basis (fair value basis) when it can reasonably estimate the cost and expected settlement dates of the obligations. Where Exxon’s management believes the life of the assets is indeterminate, it cannot identify a settlement date for the liability and does not record an obligation on the balance sheet. This is permitted under GAAP even though the timing of settlement and the costs of settlement can be considered distinct inquiries.[5] Crucially, Exxon is still liable for the AROs whenever they may occur—they are obligations that are unconditional even though uncertainty may exist around timing and method of settlement. In this sense, when the company holds a liability but does not recognize it on the balance sheet, it is an ‘off-balance sheet’ liability.

Carbon Tracker has issued a series of reports on AROs in the US, pointing out that these liabilities are largely funded from future cash flows and that the energy transition could result in ARO acceleration either through shortened economic lives of assets or regulatory responses to shore up financial assurance regimes as we have already seen in jurisdictions like Colorado.[6] In either case, these costs could come due sooner (via physical decommissioning or increased financial assurance requirements) than currently anticipated by companies. A larger variable is the risk that liabilities, which are not currently on the balance sheet since their economic lives are indeterminate, could come onto the balance sheet as that determination changes. We have seen this recently happen with Shell’s Convent refinery in Louisiana, for example.[7]

We find implicit endorsement from Exxon of the idea that useful lives might be shortened in an NZE scenario. Exxon states that “[l]onger term through 2050, we would continue to optimize and potentially expand our integrated sites with flexibility to produce lower emission fuels and chemicals while reducing their operational emissions. Additional integration with carbon capture and storage and/or fuel switching with hydrogen technology would further accelerate lowering greenhouse gas emissions intensity, with less advantaged sites potentially closed or converted to terminals.”[8] (emphasis added).

This reinforces why investors want additional information and can be understood by looking at the 2023 shareholder resolution (2023 resolution), which seeks information on the full extent of the company’s recorded and unrecorded AROs:

Resolved: Shareholders request that the Board provide an audited report estimating the quantitative impacts of the IEA NZE scenario on all asset retirement obligations. The report should disclose, as the Board deems appropriate, the estimated undiscounted costs to settle, in aggregate, related upstream and downstream AROs, and separately, identify both recognized and unrecognized amounts, as applicable. The Board should publish the report by February 2024 at reasonable cost and omitting proprietary information. Alternately this information could be disclosed in the 2023 consolidated financial statements.[9] (emphasis added).

Carbon Tracker has previously analyzed Exxon’s public responses to these resolutions. This involved comparing Exxon’s responses to what the resolutions sought. Our detailed responses analyzing Exxon’s response to the 2022 resolution are here, and the 2023 responses here. We note that our analysis of these resolutions was provided within documents we produced for the Climate Action 100+ (CA100+) which is comprised of investors concerned about the financial implications of climate change which, collectively, represent approximately $68 trillion AUM.[10] Consequently, only portions of those analyses relate to the resolutions. As noted below, many of Exxon’s comments are on work that is not related to the current resolution.

As described further below, our analysis of Exxon’s response to the 2022 and 2023 resolutions was and remains that while Exxon provided some qualitative information, it failed to provide the core information requested by these resolutions.

Exxon’s Filing

On May 10, 2023, Exxon Mobil’s Investor Relations (IR) team filed a 14A challenging our assessments of Exxon’s responses to the resolutions to date. The IR team Filing asserts that our analysis creates a “flawed narrative” about the company, “conflates” the resolutions, “confuses” key concepts and draws “false equivalencies” between Exxon and other oil and gas companies.

We have reviewed the underlying claims made by Exxon. We have determined, as set out below, that they amount to differing interpretations of the facts and/ or misinterpretations of our views or analysis. More to the point, almost all of Exxon’s comments are related to other elements of our work that are unrelated to the pending 2023 resolution.

We also identified one of our characterizations of Exxon’s statements that bear amending. It is a minor point on how we characterized $17 billion of proposed investments in carbon emissions reduction and is unrelated to the 2023 resolution.[11] We would submit that these challenges are largely irrelevant to the question of whether Exxon should provide an aggregate assessment of its total potential asset retirement obligations (AROs), even those that are not included on the balance sheet today.

Exxon’s Response to the 2022 Resolution

We start with the 2022 resolution which garnered the support of a majority of Exxon’s investors because it highlights the disconnect between what investors have sought and what Exxon has provided. The 2022 resolution sought an understanding of how the NZE would “affect the assumptions, costs, estimates, and valuations underlying its financial statements, including those related to long-term commodity and carbon prices, remaining asset lives, future asset retirement obligations, capital expenditures, and impairments.”

The focus was on the forward-looking inputs to its financial statements as well as the valuations that drive those conclusions. While accounts include many backward-looking components, some valuation tests (i.e., impairment tests) involve forward-looking assumptions that, in turn, could be significantly impacted by changes in the external environment. This results in expectations about the future being baked into the accounts.

Exxon provided a response, but it was not entirely responsive to the 2022 resolution. Exxon’s assessment outlined how its strategy might shift under the NZE scenario, rather than how its existing balance sheet asset would be impacted.

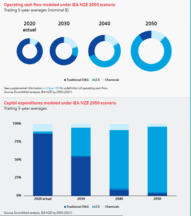

This can be seen in some of the key disclosures in its report, Advancing Climate Solutions- 2023 Progress Report (2023 ACS), published in December 2022. (Exxon’s Filing references, “information about potential nominal dollar impacts on our operating cash flow and potential changes to our capex through 2050”, which we believe refers to these charts):

While not responsive to how Exxon’s balance sheet (e.g., existing assets and liabilities) might be impacted by such a scenario, we believe these charts illustrate why a majority of Exxon’s shareholders supported Exxon disclosing such information.

The top chart shows Exxon’s traditional oil and gas business cash flows shrinking dramatically towards 2050, with replacement cash flows having to come from its “Low Carbon Solutions” (LCS) segment, a segment that is an immaterial portion of cash flows today. Exxon explains that in an NZE-like scenario, they would respond by “ceasing oil and gas exploration”[12] which articulates their strategic response but does not address the impact that these declines might have on the financial presentation–such as shortened asset lives, impairments, and/ or accelerated decommissioning costs.

The bottom chart reinforces this concern by demonstrating that Exxon would also have to radically pivot its spending from the traditional oil and gas business to the LCS business in order to make this shift. This is interesting but addresses only partly the capital expenditure portion of the 2022 resolution. In large part, the 2022 resolution sought information on the treatment of assets and liabilities that are on today’s balance sheet from such a shift; potential future investments are not recorded on the balance sheet today.[13]

In short, instead of quantifying the potential adverse impact of the NZE scenario on the financial statements, Exxon offered charts suggesting how its business and operating revenues might evolve if it were to plan around the NZE—which Exxon contends is, “disconnected from how the transition is unfolding today”.[14] While these charts suggest that investors should consider the financial implications of an aggressive energy transition, it fails to provide a complete answer to the 2022 resolution.

Exxon’s Response to the 2023 Resolution

The 2023 resolution sought the undiscounted cost estimate of all of Exxon’s AROs, whether currently on the balance sheet or not. It requested aggregate data relating to undiscounted AROs as a means of sensitizing the potential financial impact of accelerated retirement.[15] The Proponents acknowledged that where management believes an asset has an indeterminate life, non-disclosure of the estimated liability is “…permitted under existing accounting requirements….”[16] Because disclosure requirements do not require the disclosure of undiscounted costs of retiring assets with indeterminate lives, Proponents have had to seek voluntary disclosure from the Company.

Carbon Tracker evaluated whether Exxon fulfilled the Proponents’ request. We determined that Exxon’s response to the 2023 resolution, as with its response in 2022, failed to provide what investors were seeking. Exxon has not provided the estimated undiscounted costs to settle all the company’s AROs, upstream and downstream, recognized and not recognized, as sought by the resolution.

This lack of response is not genuinely in dispute. Exxon opposes the 2023 resolution, arguing that, “pursuing this sort of disclosure doubles down on a misunderstanding of our business and energy transition plans, and it could mislead investors and other stakeholders if we attempted to predict AROs beyond the estimates already provided on our balance sheet.”[17]

Additional Issues with Exxon’s Filing

We believe that some statements in Exxon’s Filing may leave readers with a misimpression. Exxon states: “We test our portfolio against a range of scenarios and projections, confirming that our flexible strategy enables us to adapt to the energy transition at the pace society demands. The notion that we are concealing AROs by treating them as ‘off-balance sheet liabilities’ is objectively wrong and demonstrates a basic lack of understanding about our business and the accounting rules that apply.”[18]

This assertion is problematic for several reasons.

- First, neither Carbon Tracker nor (to our knowledge) the Proponents accused Exxon of “concealing” these liabilities. To the contrary, and as noted in the Proponents’ 14A filing which preceded Exxon’s, the whole point of the resolution is to seek voluntary disclosure of material information that might not otherwise be required.[19] Exxon’s IR team surely was aware of Proponents’ 14A filing and therefore the rationale for the resolution, but nonetheless has insinuated that the resolution accuses the company of concealing information. We believe that such a claim risks confounding shareholders.

- Second, some readers may be led by this statement to believe it is ‘objectively wrong’ that Exxon has liabilities off the balance sheet. However, Exxon’s own filings acknowledge that such liabilities exist. Exxon’s 10-K notes that the company has generally not recognized legal obligations for retiring downstream and chemical facilities on the basis that, “these sites have indeterminate lives based on plans for continued operations and as such, the fair value of the conditional legal obligations cannot be measured, since it is impossible to estimate the future settlement dates of such obligations.”[20]

- Third, Exxon suggests that the foregoing demonstrates a basic lack of understanding of the business and accounting rules. This simply ignores the fact that: (a) the genesis of the proposal is because the accounting rules, as applied, might result in the omission of certain liabilities where settlement dates were indeterminate, (b) the Proponents have simply sought information about the undiscounted costs, not a change in the accounting treatment, and (c) the Proponents have sought this to understand the potential sensitivity of these liabilities should management not be able to repurpose its downstream assets. Similar arguments were made in the Proponents’ 14A filing in support of the 2023 resolution[21] but ignored in Exxon’s subsequent opposition Filing.[22]

- Fourth, Exxon’s own auditor, PwC, has provided general guidance on the disclosure of AROs with indeterminate settlement dates. PwC’s guidance states that when assets have indeterminate settlement lives, management should consider making the types of disclosures Proponents seek: “For example, if a reporting entity has an ARO associated with an asset with an indeterminate life, no reasonable estimation of the fair value of the ARO is possible and no liability is recorded. However, management should consider disclosure of the potential cash flows (based on current estimated costs) related to this unrecognized ARO.”[23] This suggests, at minimum, a reasonable debate as to whether Exxon should be providing such disclosures without engaging in a protracted battle with its shareholders.

Responses to Exxon’s claims about Carbon Tracker’s analysis

We believe the foregoing reflects the core issues related to the pending 2023 resolution. We now address some of the footnotes contained in Exxon’s filing.

With one exception, these challenges do not reflect arguments about factual statements, but instead interpretations and judgments of what they mean. Moreover, they also reference other Carbon Tracker research that has no bearing on the 2023 resolution.

We noted above one minor issue. We characterized Exxon’s $17 billion in investments as directed towards ‘reducing others’ emissions’ when in fact some of it is directed at reducing Exxon’s Scope 1 and 2 emissions. Our presentation identified the correct overall amount, and cited the relevant passage from Exxon’s disclosures, but omitted mention of efforts to reduce its own emissions, or the allocation thereto. This detail is not relevant to the 2023 resolution and did not play a role in the ultimate scores we provided Exxon in the benchmark process (discussed below). In other reports, we have segmented out these two amounts.[24]

For context, Carbon Tracker produces analysis against a published benchmark supplied for CA100+ for assessing whether companies and auditors are providing evidence of incorporating climate-related risks into the accounts. The rubric for this benchmark is published online.[25] Related Carbon Tracker assessments are published and available online.[26] The analysis looks at what companies are disclosing in annual and other reports and includes whether there is consistency between that information and the financial statements, whether firms have sought to quantify potential impacts, and whether auditors have complied with their respective obligations. While not necessarily required under accounting standards but of interest to investors, it also examines whether companies have aligned their businesses with the NZE scenario and if not, whether they have sensitized key financial statement line items to that outcome.

Many of the Filing’s criticisms in Footnote 5 relate to these benchmark assessments or the 2022 resolution rather than the 2023 resolution and simply express disagreement with our independent conclusions and judgments rather than the facts themselves.

- Exxon’s asserts that the NZE scenario is too ‘remote’ to be considered in the financial statements even though it identifies the transition to low-carbon fuels as a material risk factor.[27] Exxon is entitled to their view, though we would note that several European peer companies have considered the NZE scenario via sensitivity analysis in annual reports.[28]

- Exxon challenges our characterization of both the NZE and its Outlook as ‘hypothetical.’[29] Our intention with this word, used first by Exxon to characterize the NZE, was to show that both involve making a “guess” about future states—whether commodity or carbon prices or policy or other events. We would agree that Exxon’s Outlook takes a bottom-up approach to assessing the future, while the NZE takes a top-down approach using the stated ambition of the world’s governments. Clearly, different parties take different views on the drivers and pace of the energy transition. However, this is neither relevant to the 2023 resolution nor a matter of factual dispute.

- We analyzed Exxon’s response to the 2022 resolution and concluded that it was not fully responsive to the text of the resolution, as described above.[30] The resolution essentially seeks to understand how changing financial estimates and assumptions to align with those in the NZE would impact an array of items in the financial statements. In our view, this implies the same type of quantitative presentation that is already made in the financial statements. Exxon claims in effect that we have misinterpreted the resolution since the word “quantitative” is not mentioned. We believe the resolution sufficiently put Exxon on notice that quantitative information was sought, even though that word was not used in the resolution. Ultimately, this is a question of the resolution filer’s intent; other filings by the 2022 resolution filer further reinforce that they were in seeking quantitative information.[31]

- Exxon states that our assessment ignores the rigor of its analysis and the thoroughness of its disclosures. It references the Wood Mackenzie audit statement as further evidence of its work. Our assessment[32] of Exxon’s response and the Wood Mackenzie opinion does not question whether it properly used the NZE assumptions in its scenario analysis. Our central contention was that the work performed did not satisfy the 2022 resolution.

- Exxon notes that they use a broad range of commodity prices for planning, which is reasonable, and that our assertion of the range being ‘too broad’ ignores the cyclicality of the industry.[33] We agree that using a wide range of prices, from a business planning standpoint, is reasonable. But from the standpoint of valuing assets in the accounts which is what the resolution called for, a reasonable price forecast is used for the relevant asset(s), not a range. Providing a range of price projections informed by third parties and used in planning does not serve that purpose.

Finally, Carbon Tracker also has a Corporate Research team that does deep-dive analysis of selected companies, including Exxon. One of our senior corporate research analysts published a report earlier this year looking at the challenges facing the company.[34] This work does not relate to and did not address the 2023 resolution, but we nevertheless provide context for the points raised by Exxon.

- First, Exxon asserts that we quoted an old report— the ExxonMobil 2021 Outlook for Energy, and not the later edition. We did quote this report as part of our analysis of Exxon’s oil and gas demand forecast. We have re-reviewed and the conclusions we reached in that report would not be materially different had we quoted the new version.

- Second, Exxon contends that we mischaracterized Exxon’s CEO Darren Woods in his comment about new passenger cars being electric by 2040, in that he was discussing a sensitivity.[35] This quotes a Darren Woods interview with CNBC which is titled “Every new passenger car sold in the world will be electric by 2040, says Exxon Mobil CEO Darren Woods”. [36] However, we listened to that interview and, in discussing Mr. Wood’s comment in the report we characterized it as, “a possible scenario where all passenger vehicles in the world will be electric by 2040.” (emphasis added).

In sum, we believe the challenges to our work are at best a distraction from the question on the ballot; some investors want to understand the downside risk to Exxon’s balance sheet from a low carbon transition. Exxon’s board believes an NZE-like transition is currently unlikely, does not think the information would be helpful, and does not want to provide it. Investors will have to weigh in.

[1] See: https://www.sec.gov/Archives/edgar/data/34088/000119312523146870/d512031ddefa14a.htm, p. 3.

[2] CBIS also filed a similar resolution in 2021 which received 49% of the vote. See: https://www.iccr.org/sites/default/files/blog_attachments/cbis-xom-press-release-060421.pdf

[3] ExxonMobil, Notice of 2022 Annual Meeting and Proxy Statement, p76 (2022). https://investor.exxonmobil.com/sec-filings/all-sec-filings/content/0001193125-22-098314/0001193125-22-098314.pdf.

[4] https://asc.fasb.org/MasterGlossary

[5] Accounting Standards Codification 410-20-25-7: “The obligation to perform the asset retirement activity is unconditional even though uncertainty exists about the timing and (or) method of settlement.”

[6] See, e.g., There Will be Blood, https://carbontracker.org/reports/there-will-be-blood/ (2023); Event Horizon, https://carbontracker.org/reports/event-horizon-a-case-study-of-holdback-analysis/ (2022); Billion Dollar Orphans, https://carbontracker.org/reports/billion-dollar-orphans/ (2020); It’s Closing Time https://carbontracker.org/reports/its-closing-time/ (2020); The Flip Side: Stranded Assets and Stranded Liabilities, https://carbontracker.org/reports/the-flip-side-stranded-assets-and-stranded-liabilities/ (2020).

[7] Royal Dutch Shell plc, Form 20-F For the fiscal year ended December 31, 2020, p53, 198 (2021). https://shell.gcs-web.com/node/18726/html

[8] ExxonMobil, 2023 Advancing Climate Solutions Progress Report, p.32 (2022).

[9] ExxonMobil, Notice of 2023 Annual Meeting and Proxy Statement, p. 91 (2023). https://investor.exxonmobil.com/sec-filings/all-sec-filings/content/0001193125-23-100079/0001193125-23-100079.pdf

[10] https://www.climateaction100.org/

[11] Even here, the issue is simply that we failed to state in a summary note that part of the $17 billion that Exxon was committing to emissions reductions was to reduce Scope 1 and 2 emissions. In other, longer reports such as, ExxonMobil – the Existential Crisis, (https://carbontracker.org/reports/exxonmobil-the-existential-crisis/), we have segmented this out. (“Between 2022 2027, Exxon plans to spend $17 billion in low emissions investments…~60% of the $17 billion or ~$10 billion of this will be deployed toward supporting the company’s 2030 and 2050 Scope 1 & 2 emissions reduction targets.”)

[12] ExxonMobil, 2023 Progress Report Advancing Climate Solutions, p. 32 (2022).

[13] Our oil, gas and mining team looked at Exxon’s plans here: https://carbontracker.org/exxonmobil-is-planning-on-climate-failure-despite-advancing-climate-solutions/

[14] https://www.sec.gov/Archives/edgar/data/34088/000119312523140691/d502137ddefa14a.htm

[15] https://investor.exxonmobil.com/sec-filings/all-sec-filings/content/0001214659-23-006080/0001214659-23-006080.pdf. (“Proponents are not asking Exxon to recast its impairment tests. Rather, investors seek supplemental disclosure relevant to the resilience of Exxon’s existing assets in the face of a net zero scenario. Sensitivities, by definition, look at changes to noncentral case variables and there is no requirement that these be viewed as “reasonable” by management. Their purpose is to stress-test the central assumptions. Further, there is nothing in US GAAP that prohibits providing this type of additional sensitivity analysis.”).

[16] https://investor.exxonmobil.com/sec-filings/all-sec-filings/content/0001214659-23-006080/0001214659-23-006080.pdf

[17] https://www.sec.gov/Archives/edgar/data/34088/000119312523140691/d502137ddefa14a.htm

[18] https://www.sec.gov/Archives/edgar/data/34088/000119312523140691/d502137ddefa14a.htm

[19] See: https://investor.exxonmobil.com/sec-filings/all-sec-filings/content/0001214659-23-006080/0001214659-23-006080.pdf

[20] Exxon Mobil Corporation Form 10-K for the fiscal year ended December 31, 2021, p. 86 (2022).

[21] https://investor.exxonmobil.com/sec-filings/all-sec-filings/content/0001214659-23-006080/0001214659-23-006080.pdf

[22] https://www.sec.gov/Archives/edgar/data/34088/000119312523140691/d502137ddefa14a.htm

[23] PwC, Financial statement presentation – Partially updated April 2023, Chapter 11, p. 24. https://viewpoint.pwc.com/dt/us/en/pwc/accounting_guides/financial_statement_/assets/pwcfinlstmtpresentn0423.pdf

[24] Neil Quach, Carbon Tracker, ExxonMobil – the Existential Crisis, (https://carbontracker.org/reports/exxonmobil-the-existential-crisis/), p.17, we have segmented this out. (“Between 2022-2027, Exxon plans to spend $17 billion in low emissions investments…~60% of the $17 billion or ~$10 billion of this will be deployed toward supporting the company’s 2030 and 2050 Scope 1 & 2 emissions reduction targets.”).

[25] See provisional Climate Accounting and Audit Assessment methodology (2021) (updated version to be published later in 2023). The financial statement and audit report assessments are grounded in the existing requirements of the relevant accounting and audit standard setters, with investor groups also requesting information about alignment with Net Zero by 2050 (or sooner) and no more than 1.5 degrees warming.

[26] https://carbontracker.org/company-profiles/ (Accounting Assessments)

[27] See: https://www.sec.gov/Archives/edgar/data/34088/000119312523146870/d512031ddefa14a.htm, p. 3.

[28] Such as: Eni SpA Form 20-F for the fiscal year ended December 31, 2021, p. F-58 (2022), Eni SpA Form 20-F for the fiscal year ended December 31, 2022, P, F-58 (2023), Shell plc Form 20-F For the fiscal year ended December 31, 2022, Note 4: Climate change and energy transition (2023), and Repsol Group Annual Financial Report 2022, p. 61 (2023)

[29] See: https://www.sec.gov/Archives/edgar/data/34088/000119312523140691/d502137ddefa14a.htm, f/n 1, p.4

[30] See: https://carbontracker.org/wp-content/uploads/2022/04/Exxon_31Dec21_AcctgAssessment_2022AGMs-1.pdf

[31] See: https://www.sec.gov/Archives/edgar/data/34088/000121465922005292/o414225px14a6g.htm

[32] https://carbontracker.org/wp-content/uploads/2023/04/Exxon-FY22_Final_Acctg_Assessment-1.pdf, p. 11.

[33] https://www.sec.gov/Archives/edgar/data/34088/000119312523140691/d502137ddefa14a.htm

[34] ExxonMobil – the Existential Crisis, https://carbontracker.org/reports/exxonmobil-the-existential-crisis/ (2023).

[35] https://www.cnbc.com/2022/06/25/exxon-mobil-ceo-all-new-passenger-cars-will-be-electric-by-2040.html

[36] https://www.cnbc.com/2022/06/25/exxon-mobil-ceo-all-new-passenger-cars-will-be-electric-by-2040.html