When oil companies defer saving for asset retirement obligations (AROs), the liabilities accumulate.

Meanwhile production, and expectations for cash flow, inherently decline. Thus, the remaining obligations become significant by comparison to projected cash flow, and, at some point while still turning a monthly profit, known liabilities exceed all projected net future cash flow. The event horizon when an asset turns into a liability can be crossed without warning and even without recognition. Further, without regulatory intervention, such properties can be transferred from owners more likely to be able to fund the decommissioning to owners more likely to bequeath the liabilities to the public.

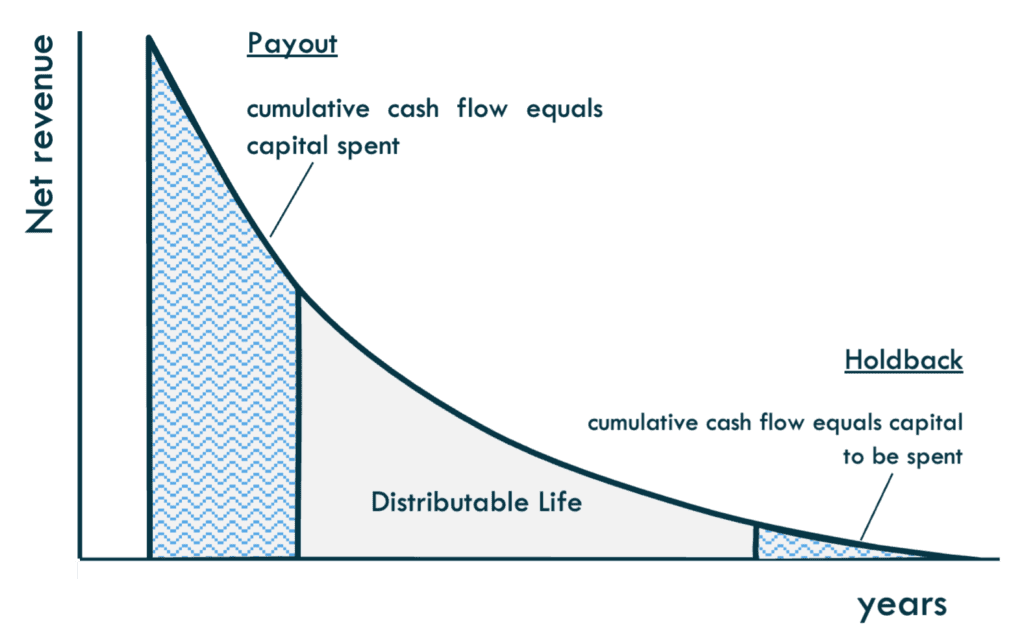

This event horizon can be anticipated with suitable analysis, but it has gone largely unrecognized by conventional economic analysis, which discounts future cash flows both in and out. Ironically, cash-flowing oil and gas fields can look like an asset on a net present value basis even when projections show they cannot fund their own retirement. We recommend and demonstrate the use of a novel economic yardstick to identify this turning point in the life of a field: Holdback.

Holdback is analogous to payout but in reverse (see Figure 1). Rather than the time forecasted to recoup capital costs incurred at the beginning of life, it is the time forecasted to fund the undiscounted capital costs at the end of life.

Figure 1: Phases of Economic Life of a Well

Source: Carbon Tracker analysis, produced by authors

Key Findings

- Deferred plugging combines with depleting production to set up a cash flow trap. Asset retirement obligations (AROs) of oil and gas assets can equal the entire net cash flow of the last 10 to 15 years or more of profitable operations.

- Conventional financial measures, namely current cash flow and discounted present values, can wrongly imply financial health even after known retirement obligations exceed projected profits.

- This last period of life – when decommissioning liability exceeds future net cash flow and a cash-flowing “asset” has turned into a liability – can be called “holdback,” and it can be calculated using standard cash flow analysis.

- When they have not used this kind of analysis, owners and financial partners may not recognize the inversion from an asset to a liability until years after it occurs, and regulators may allow property transfers that imperil public safety and welfare.

- The economic limit of operations, and thus holdback, can occur sooner than expected due to fluctuations in production and/or commodity prices. Companies may extend operations of late in life wells by cutting operating costs below sustainable levels, but temporary profits at the tail end of life are unlikely to satisfy the property’s retirement obligations, and even if they were, companies generally do not set aside funds to fulfill AROs.

- A case study using holdback analysis on two sets of wells transferred to KP Kauffman –a private oil & gas producer – suggests that at the time of transfer, future net cash flows were marginal at best and years past the point when the wells could fund their own AROs.

- A range of stakeholders, including regulators, investors, and oil and gas companies can benefit from utilizing holdback analysis to assess the economic health of assets and companies, improve asset retirement planning, and ensure funds are available to plug wells at the end of their economic lives as required by law.