Key Resources

Replay Webinar

Replay Webinar

Supporting Slides

Press Release

Press Release

Read MorePolicy Brief

Résumé Analytique

Résumé Politique

Transition risks for petrostates are higher than ever

This report, an update of our 2021 Beyond Petrostates report, finds that petrostates are facing substantial risks from the energy transition, as falling oil and gas demand is set to put downward pressure on commodity prices and place future government revenues in jeopardy.

While a small handful of countries have reduced their vulnerability, overall the 40 petrostates we analyse are just as vulnerable as in our original analysis and in many ways face growing risks.

This update is driven by two key factors: the growing socio-economic challenges confronting petrostates and the availability of new data reflecting the impact on energy markets from recent geopolitical events. We apply a least-cost methodology used in our previous report to reassess how the energy transition could affect different petrostates.

Petrostates face major shortfalls in future revenue streams

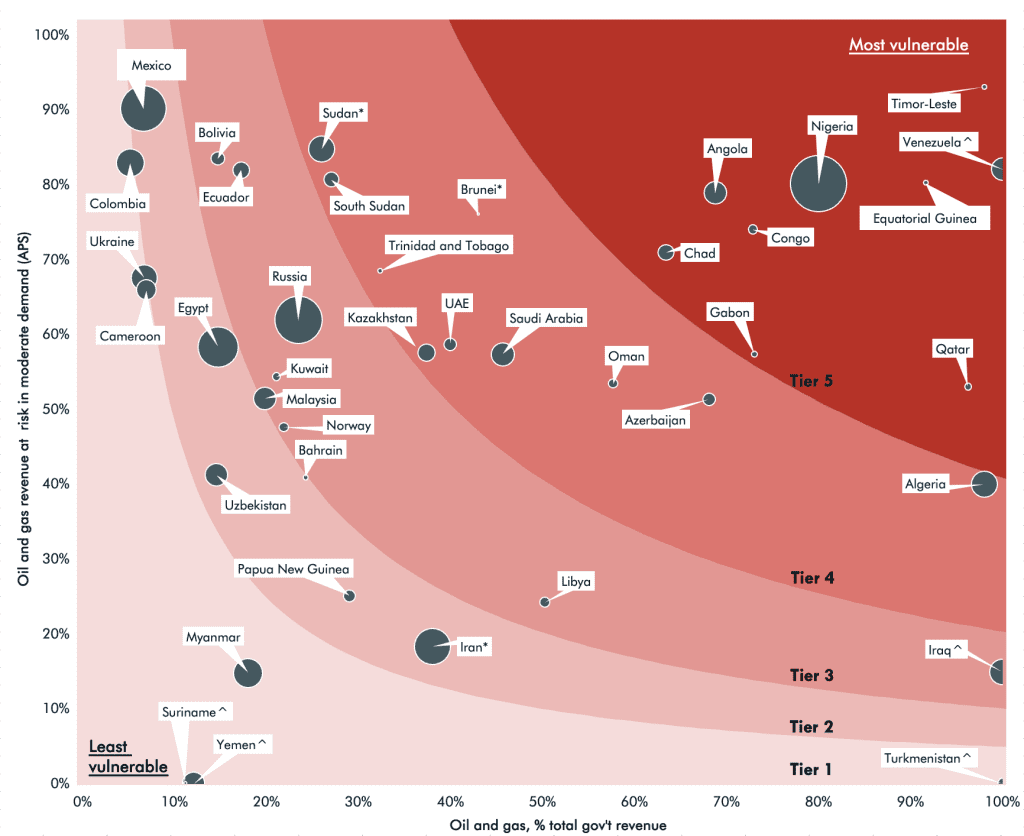

28 of the 40 petrostates would lose more than half of expected revenue under a moderate-paced transition (vertical axis, Figure 1), in line with governments’ current climate pledges (represented by the IEA’s APS scenario). $8 trillion worth of expected revenue would be wiped out between now and 2040, with different petrostates affected in significantly different ways.

Figure 1: vulnerability of petrostates’ total government revenues to reduced oil and gas demand resulting from a moderate-paced energy transition

Source: Rystad Energy, IMF, CTI Analysis

Notes: Bubble size indicates relative population size. * indicates countries where we have not been able to update oil and gas as % of total gov’t revenue data since our last analysis. ^ indicates either greater oil and gas revenue than total government revenue (Iraq, Venezuela) or improved oil and gas revenues in our moderate transition, due to unknown gas pricing and demand.

We categorise countries’ vulnerability into five tiers, reflecting the combination of their revenue shortfall and the dependence of government budgets on oil and gas revenues (Figure 1). Timor-Leste and Venezuela are found to be the most vulnerable but African petrostates – including Nigeria, Angola and Chad – make up the majority of the “highest tier” countries. This is particularly concerning given the continent’s rapidly growing populations and existing development challenges, exacerbated by rising climate impacts. While some petrostates appear low-risk according to our two key metrics, they may still be vulnerable in a wider economic context, as indicated by high fiscal breakeven prices.

No producer is safe from declining demand for oil and gas

While the highest-cost producers face the largest revenue losses per barrel, the lowest-cost producers – such as those in the Middle East – would also lose significant revenue under the moderate-paced transition scenario compared to any expectations under a slow transition.

Although oil and gas exporting countries in Europe and North America have relatively low dependence on hydrocarbons for government revenue – and are not, therefore, considered petrostates – their higher production costs mean they face greater relative losses from the transition.

Peaking oil and gas demand should make petrostates think twice about new investments

The International Energy Agency’s latest World Energy Outlook predicts demand for oil, gas, and coal will all peak by the end of this decade thanks to the falling costs of clean technologies, even if no additional climate policies are introduced. While current high inflation and interest rates have interrupted the downward trend in these falling costs, this is likely to be a temporary setback in sustained long-term trajectories.

The increasing economic competitiveness of clean technologies has given governments (mainly in the Global North) the confidence to announce future bans on the sale of new petrol and diesel vehicles and gas boilers, wiping out a substantial proportion of fossil fuel demand permanently.

There is growing momentum around COP28 for governments to agree on a target of tripling renewable energy capacity by 2030 and a doubling of energy efficiency measures, setting a clear direction of travel.

Recent events have highlighted the need to cut dependence on volatile imports

Since our original Beyond Petrostates report, the world has been rocked by a number of geopolitical events with significant implications for global energy supplies – most notably Russia’s invasion of Ukraine but, more recently, conflict in the Middle East. Many countries, particularly the G7 and European Union, have accelerated efforts to cut dependence on fossil fuel imports in response. This further threatens Petrostates’ customer base in the coming decades.

There is a growing global consensus to curb fossil fuel use

While fossil fuels have largely been a taboo subject at UN climate summits, the tide has now begun to turn. The final agreement at COP26 in 2021 included language on fossil fuels for the first time – specifically a “phasedown” of unabated coal power and a phaseout of inefficient fossil fuel subsidies. The COP also saw the launch of the Beyond Oil and Gas Alliance, which aims to facilitate the managed phase-out of oil and gas production, and recently welcomed its first petrostate – Colombia – as a “friend”.

Emerging petrostates are setting up their industries at the worst possible time

While the focus of our analysis is on existing petrostates, we also warn of the risks faced by countries that are only now beginning to kickstart their oil and gas industries. Since our original Beyond Petrostates report, we note that many of these “emerging petrostates” have seen delays to major planned projects and are still launching new rounds of licensing, further increasing transition risks.

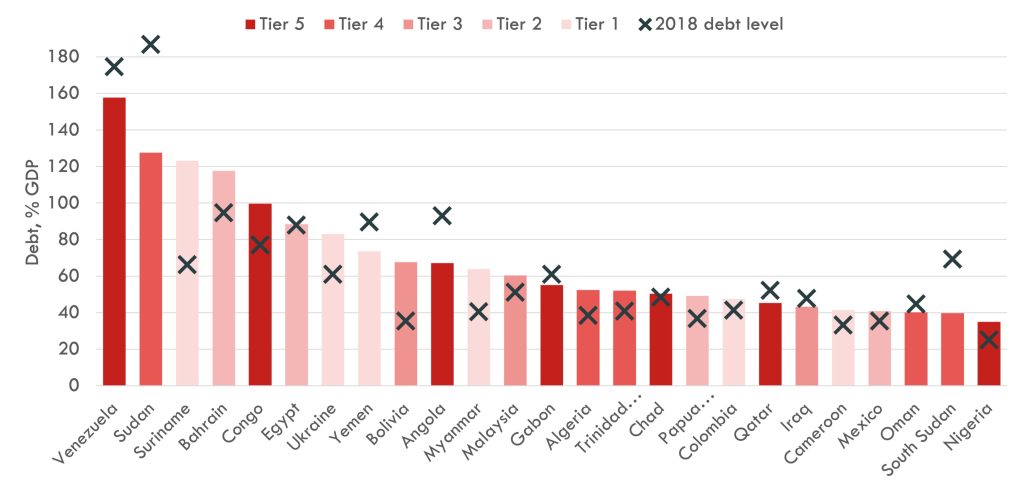

Another trend we note is of increasing national indebtedness (Figure 2) among the 40 petrostates and an attendant worsening of creditworthiness, with several countries – including Bolivia, Cameroon, Egypt, Kuwait, and Colombia – experiencing downgrades in recent years. Poorer credit ratings undermine petrostates’ borrowing ability, both for day-to-day spending and to support new industries, further trapping them in fossil fuel dependency.

This adds to the picture we set out in our original report, which highlighted the petrostates’ near-doubling average debt since 2010, compounding their vulnerability to a reduction in national income from fossil fuel exports.

Figure 2: government debt-to-gdp levels for the most indebted petrostates by vulnerability tier, with comparison to 2018

Source: IMF, CTI analysis

Notes: Newly sourced actuals for 2018 included, to enable a 2018 to 2022 comparison for Turkmenistan, Russia, Uzbekistan, South Sudan, Myanmar, Yemen, Ukraine, Egypt, Venezuela. Data collected is primarily Central Government Debt, though figures for Uzbekistan, Egypt, Russia, and UAE are General Government Debt. Figure includes the top 25 most indebted petrostates in our analysis, from IMF 2022 data.

Petrostates have a number of options on the table…

In the face of these risks, petrostates must consider a series of measures that would reduce their vulnerability to the energy transition. These include economic diversification, fossil fuel subsidy reform, the creation of sovereign wealth funds, and the establishment of new taxes (e.g. on fuel and VAT). The adoption of forward-looking policy approaches, which address the transition and can mitigate its negative impacts, is increasingly urgent.

… But international cooperation is needed

Many countries have undertaken such reforms and could serve as models for others to follow. Fora including OPEC or the Beyond Oil and Gas Alliance would be well-suited to facilitate peer-to-peer learning and share best practice.

The international community more broadly has a clear stake in supporting petrostates through this process, both for development reasons and to mitigate the very real risk of conflict and instability if these countries are hit hard by the energy transition. Just Energy Transition Partnerships could be extended beyond coal to oil and gas as a means of financing the necessary changes.

Key Findings

- Fossil fuel demand is facing irreversible decline, as a revolution in technology is driving the energy transition and will likely be accelerated by further policy action.

- Oil and gas exporting nations are particularly vulnerable to the transition as hydrocarbon revenues weaken. Those countries with highest fiscal dependence and higher cost project options are most at risk.

- Russia’s invasion of Ukraine has accelerated the transition by encouraging countries to reduce dependence on fossil fuel imports, increasing the risk for exporting countries.

- We identify and update our analysis of 40 ‘petrostates’ which rely on oil and gas revenue to balance fiscal budgets. Of these, 17 petrostates derive over 40% of total government income from the sale of oil and gas.

- The majority of the petrostates would see over 50% of expected oil and gas revenue lost under a moderate-paced energy transition, represented by the IEA’s Announced Pledges Scenario (APS).

- We identify 9 highly vulnerable petrostates with over 60% of total fiscal budget at risk under a moderate transition, including African countries Nigeria, Congo and Gabon.

- Even the lowest cost producers will not be shielded from heavy revenue losses in a moderate transition, despite OPEC+ gaining an increased overall market share.

- Petrostates must urgently seek to diversify their economies – particularly those identified to be most vulnerable. We outline a number of options for policymakers, including subsidy reform, sovereign wealth funds, and alternative taxes.

- Support from the international community will be needed. Transition finance could play an important role in future-proofing hydrocarbon-dependent economies, taking inspiration from recent efforts to assist coal-reliant countries.

- OPEC+ is already at significant spare capacity, suggesting a weakening market; recent supply restraint from member states questions the industry narrative around persistent high demand for oil and gas.

- Indebtedness among petrostates is increasing, with two of the nine most vulnerable petrostates facing debt to GDP ratios above 80%, a level at which economic growth becomes increasingly difficult.

- For investors, the reduction in future revenues may reduce the creditworthiness of countries and impact sovereign debt markets. We note that credit ratings for Bolivia, Cameroon, Egypt, Kuwait, and Colombia have been downgraded by major rating agencies since our 2021 analysis.