Key Resources

Firms can avoid wasting $500bn with managed approach to transition in Inevitable Policy Response scenario even if oil demand rises short-term.

Managing Peak Oil considers the financial implications of a future where demand increases into the mid-2020s and then falls rapidly. It finds that the best route to meet that demand while preserving value is to maintain a conservative approach to long-term investment and meet short-term demand with shale projects that can deliver new production quickly.

This report explores a non-linear demand pathway using the Inevitable Policy Response consortium’s Forecast Policy Scenario (FPS), commissioned by the UN PRI, which is consistent with limiting global temperature rise to 1.8°C. It shows how companies can manage peak oil demand, while reducing the risk of wasting investment, and preparing to wind down production in line with the Paris Agreement target.

Two different ways forward for the industry in this complex future are explored – one risky and destructive (the ‘high investment case’), the other cautious and more tailored to the ‘bump’ shape of the FPS demand curve (the ‘managed case’).

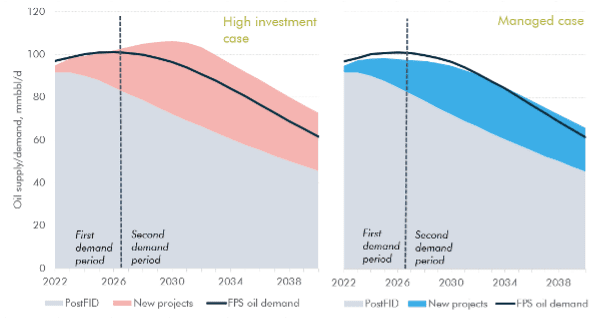

Figure 1 – High investment case severely oversupplies market in period 2 (2027-2040)

Oil supply from already-sanctioned (post-FID) projects and new projects sanctioned in period 1 (2022-2026) in the high investment (left chart) and managed (right chart) cases, with FPS oil demand

Source: Carbon Tracker analysis

Figure 2 – Managed case could eliminate value destruction

Capex (2022-2030) on projects approved in 2022-2026 split by commerciality at two supply cases and three long-run oil prices

Source: Carbon Tracker analysis

This analysis updates our previous IPR research, Handbrake Turn.

Key Findings

- Oil demand and pricing are currently rebounding, triggering calls for significantly increased investment into new oil – a narrative at odds with the immediate global production reductions required within most “well below 2°C” scenarios.

- Short-term demand growth would see even greater reductions required subsequently to keep the goals of the Paris Agreement alive. Policy action is likely to strengthen post-COP26, while the rapid adoption of EVs will potentially further weaken demand.

- Companies basing sanctioning decisions on bullish short-term signals thus risk significant over-investment, seriously impacting shareholder value. It wouldn’t be the first time that the industry has fallen into this trap.

- This analysis therefore explores the financial implications of such a non-linear scenario, where oil demand grows in the short-term before falling rapidly. We use the Inevitable Policy Response Forecast Policies Scenario (FPS, 1.8°C) where oil demand peaks in the mid-2020s.

- Under a ‘high-investment case’, companies could waste some $530bn of capex this decade as demand starts to decline and the oil price falls back to c.$40. This amount would double at $30/bbl.

- As an alternative, we explore a ‘managed’ case where companies sanction more conservatively for long-cycle projects, only up to $30/bbl breakeven. The managed case then assumes companies sanction more liberally for short-cycle projects (which ramp up production quickly), up to $50/bbl breakeven, to meet elevated short-term demand.

- The key is to avoid locking in high-cost, long-cycle projects. Our managed case significantly cuts oversupply over the long term and eliminates wasted capex at a $50/bbl long-run oil price. The managed case wastes less capital than the high investment case irrespective of oil price.

- Managing oil prices in the next few years would be a challenge under a scenario such as the FPS, even allowing for increased shale production. There is, however, enough oil to meet the short term bump.

- OPEC needs to deploy its spare capacity much more aggressively to avoid even higher prices than today – up to an extra 2mbd in the managed case. This is what can stop the oil price spiking beyond $80; without this, higher prices could last for several years. We believe this is in the group’s long-term interests.

- For investors who subscribe to an FPS-like pathway, it’s imperative to challenge management on higher cost projects, particularly those with sanction some years hence.