Financial assurance requirements are universally considered to be too low to pay for plugging and abandoning wells. An inventory of inactive wells across the country shows that regulators have failed to require uneconomic wells to be plugged and abandoned.

We therefore ask: why do operators ever plug wells? The data suggests one key driver: drilling. That is to say, operators only “fill when they drill.” It’s a startling conclusion but not necessarily a surprising one—plugging wells is a cost and economic actors avoid costs, if they can. However, that cost is unavoidable when the objective is to frack a mature field. In that case, older wells may need to be plugged to maintain pressure or avoid “frac hits,” when pressure and/or fluids from a newly fractured well communicate with an existing well.

Looking at the data for the thirteen largest oil and gas producing states, we find significant correlation between new horizontal and directional drilling and the plugging of older wells, explaining two-thirds of the recent plugging activity in the 13 top states by well count. This makes sense since communication between wells is a key side-effect of the fracking. But if companies primarily plug wells when they are drill: Will the filling stop when the drilling stops?

If it does, operators will need other economic incentives to plug wells. Those needs will only grow stronger with less demand for oil and gas, due to the energy transition, and the potential for less revenues from oil produced, due to diminishing demand. This is not a far away problem since, as we noted in Fault Lines, there is little to no need for new wells in most low-carbon scenarios.

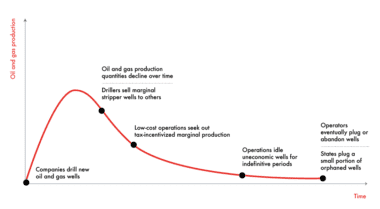

Lifecycle of a typical oil and gas well:

This has implications for regulators:

First, some regulators look at current plugging practice as a sign that operators will meet these obligations. Basing policy on such false assurance would tend to justify complacency with the status quo when regulatory reform is needed. If plugging is no longer driven by drilling, regulators will need to revisit the financial carrots and sticks that can incentivize timely plugging activity.

Second, regulators may assume that higher plugging counts by large drillers is evidence that blanket bond regimes are working. But if drilling stops, so will plugging. By then it may be too late to eliminate blanket bonds and impose higher individual bond amounts.

Finally, policy makers may fail to appreciate the full environmental risks associated with frac hits, including uninsured damage to previously plugged wells. Large drillers may be creating more problems than they are solving with “drill-filling”.