Key Resources

Recent extreme price spikes for the GB power market have triggered key discussions over whether the time has come for a shift in the way that electricity generation is traded and priced in the country.

Marginal Call estimates what Great Britain’s wholesale market electricity costs would have been if prices were calculated via a “split market” that separates the pricing of power produced by variable supply of renewables, from other sources, as opposed to the marginal pricing design the market currently operates under.

When calculated this way, total net power procurement expenditure over 2021-22 turns out around £7.2 billion lower, representing what could have been saved if measures had been in place to protect against gas market price spike influence on the power market.

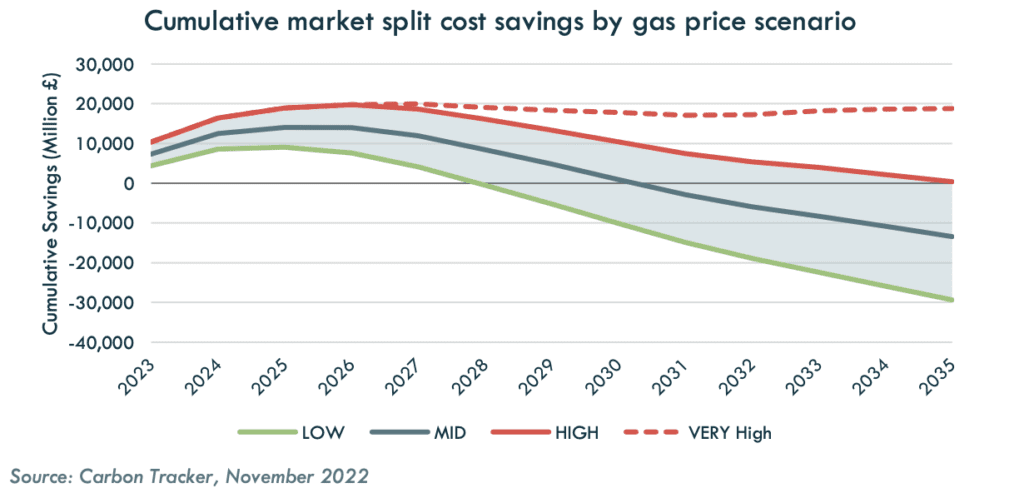

Market split design would however only result in cheaper bills for consumers over the longer-term if gas prices remain at high levels for the rest of the decade (fig 1), while pricing signals for flexible power sources such as battery storage would be weakened.

Figure 1: Gas prices would need to remain high for market split design to achieve long-term cumulative cost savings

Instead, the analysis suggests policy measures such as utility hedging obligations for future fuel needs to reduce exposure to high gas prices, and reform to contracts for difference (CfD) agreements to lower bills.

Watch a summary video here:

https://www.youtube.com/watch?v=mILcJ5JGUwM

Key Findings

- GB’s wholesale power market grid procurement expenditure over 2021-22 was not reflective of the makeup of technologies supplying electricity. Estimated grid costs turn out more than £7 billion lower on a net basis when calculated instead using a generation-weighted average of technology output over that period.

- Policy makers should consequently introduce measures to protect against future gas market price spikes which skew power market prices under marginal pricing design. These could include imposing hedging obligations on utilities for their future fuel requirements.

- The continuation of marginal pricing is still preferable to a significant shift in market design. A complete change in the market design used for the pricing of GB electricity generation may risk denting investor confidence in renewables and low-carbon forms of flexible generation by creating renewed uncertainty over project revenues. This could consequently threaten the UK’s 2035 deadline for completing power sector decarbonisation.

- Alongside measures to counter any future gas market price spikes, the UK Government should also restructure its Contracts for Difference (CfD) support scheme for low-carbon generators. Basing future CfD top-up payments on eligible firms’ overall combined revenue streams would ensure investor confidence is not impacted by the risk of not receiving payment during periods of zero or negative prices in the wholesale market, while the adoption of contracts from the point of first operation of a project should be made mandatory.