Despite rising acceptance of peak oil demand, most plan on increasing production

LONDON/NEW YORK, June 24 – Most oil majors have set climate ambitions that leave them free to increase production or ignore the full impact of burning their future oil and gas, finds a report by Carbon Tracker on Wednesday that uniquely ranks the strength of their corporate climate policies.

It shows that companies such as Shell and Total are setting out ‘net zero’ ambitions without committing to the absolute reductions needed to link to finite climate limits, while targets set by their US counterparts ExxonMobil, Chevron and ConocoPhillips ignore carbon released when their oil and gas is burned.

It also notes that companies’ emissions targets can give investors an insight not only into how closely aligned they are with the Paris climate targets but also how well they recognise the impact the energy transition will have on their traditional business models.

Companies that recognise there are climate limits to the oil and gas that can be burned are likely to take more cautious investment decisions while those whose policies allow for continued growth may invest in higher cost projects that rely on continued growth in demand.

Through a unique approach[1], Absolute Impact analyses and ranks emissions targets following a flurry of new industry announcements at the end of 2019 and finds big differences in their effectiveness at contributing to climate change mitigation and reducing the risk of stranded assets.

Mike Coffin, Oil & Gas Analyst and author of the report, said: “Companies cannot be aligned with Paris unless they commit to only sanctioning Paris-aligned projects – this will have the knock-on effect of absolute cuts to their oil and gas production and resulting emissions.

“On their own, net zero targets are insufficient to link to Paris goals. To do that, climate targets need to recognise the absolute limits of a global carbon budget and incorporate interim emissions reductions. Policies which fall short will fail to satisfy both environmental and financial concerns from investors, and risk being perceived as greenwashing.”

Carbon Tracker found that corporate policies fell broadly into three levels of ambition with a major gulf between US and European companies:

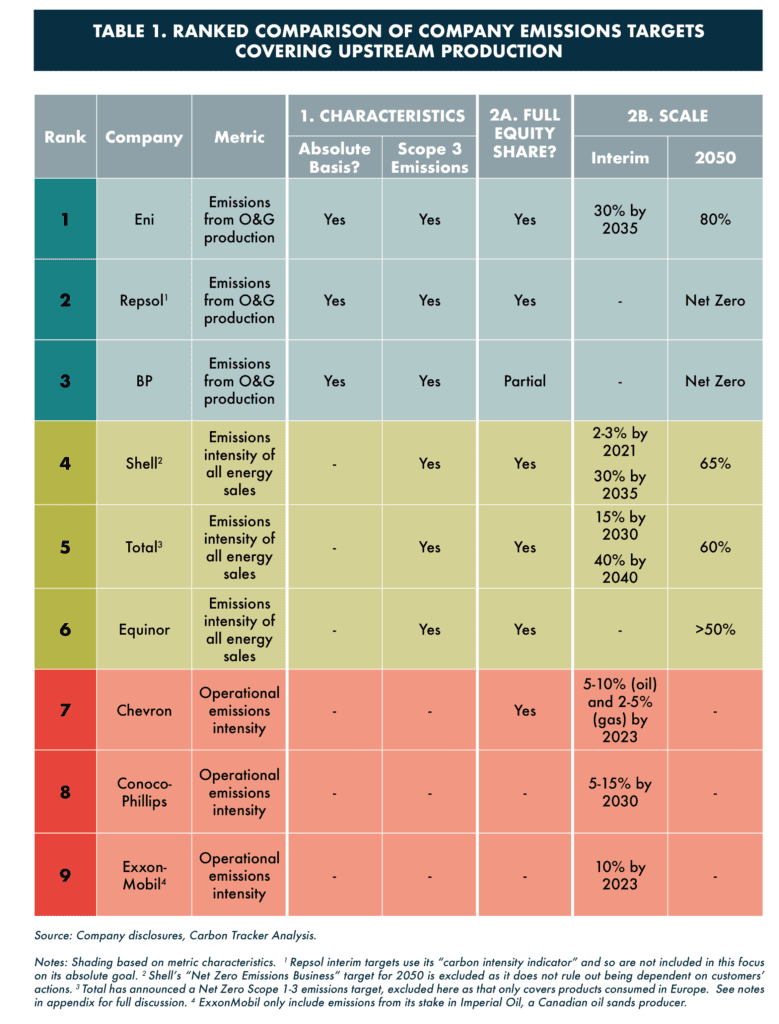

- Eni, Repsol and BP have the most impactful policies, which all set absolute targets for cutting emissions by 80% to 100% across their oil and gas production by 2050. Eni leads the field with a strong interim target of cutting emissions by 30% on an absolute basis by 2035.

- Shell, Total and Equinor come next. They have set targets of reducing the carbon intensity of the oil and gas they sell by 50% to 65% by 2050, but this is not a commitment to an absolute cut in their emissions.

- While European companies targets cover Scope 3 emissions from the use of their products Chevron and ConocoPhillips only commit to small cuts in operational carbon intensity of operations (Scope 1 & 2) by 2050, equivalent to a maximum 3% cut in overall emissions.

- ExxonMobil ranks bottom because its targets only cover operational emissions related to its investment in the oil sands producer Imperial Oil.

Carbon Tracker has previously found that in order to meet the Paris target oil majors would need to cut combined production by 35% from 2019 to 2040.

“In a world of decreasing demand for oil and gas, only the most cost-competitive projects will generate value, and even they will potentially deliver lower than expected returns,” it states.

“Capital invested into projects that exceed climate limits risks becoming stranded and destroying shareholder value.”

However, the report warns that, despite growing acceptance that demand for oil and gas will peak in the next decade, most companies plan to increase oil and gas production and therefore risk creating considerable stranded assets.

The report notes that each company frames its emissions targets differently and defines pre-requisites for metrics to be considered as linking to Paris goals that the think tank terms “Hallmarks of Paris Compliance” . These are:

-

- Absolute targets – Companies cannot be aligned with the Paris Agreement unless they recognise that there is a finite carbon budget and plan absolute cuts in emissions from their oil and gas production. Companies that pledge to reduce only the intensity of their emissions, leave the door open to potentially expanding oil and gas production.

- Full lifecycle emissions (Scope 1, 2 and 3) – US companies which only set targets covering their own operational emissions (Scopes 1 & 2) ignore the 85% of emissions that come from burning the oil and gas they produce (Scope 3).

- Full equity share – Comprehensive emissions targets should cover the vast majority of production owned by companies. BP is marked down because its targets do not cover its stake in Rosneft, which accounts for 29% of its production.

- Net zero – Many companies have announced “net zero” policies which do not fully meet these criteria: Shell’s aim to be a “net zero emissions energy business” potentially relies on customers taking action to reduce emissions, while Total’s net zero target only applies to Europe.

- Interim targets – It is not enough to set an ambitious 2050 target. Companies must also set out a pathway to get there with significant targets to ensure timely action.

- The report says without a concrete plan “this may lead to questions of commitment and at worst accusations of “greenwashing”.

ENDS

To arrange interviews please contact:

Stefano Ambrogi sambrogi@carbontracker.org +44 7557 916940

Joel Benjamin jbenjamin@carbontracker.org +447429637423

David Mason david.mason@greenhousepr.co.uk +44 7799 072320

[1] : It compares the structural fit of carbon emissions targets relative to the concept of the global carbon budget, using the three hallmarks laid out in CTI’s “Balancing the Budget” report, and then analyses the magnitude of both 2050 and interim targets.