The HDV sector is failing to electrify at anything close to the pace required

LONDON/NEW YORK, May 2 – The world’s leading Heavy Duty Vehicle (HDV) manufacturers are failing to transition towards EV production at a pace in line with climate goals and upcoming regulations, finds a report from think-tank Carbon Tracker on Thursday.

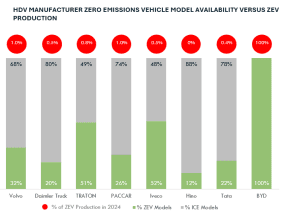

To be aligned with the IEA NZE [Net Zero Emissions] scenario, more than 13 million zero emission HDVs need to be deployed globally by 2035. But in 2023 with little more than 10 years to go less than 100,000 new zero emission HDVs were produced – less than 2% of global HDV production.

Carbon Tracker assessed 8 HDV manufacturers, which cover 50% of global HDV production/sales, on the quality of their emissions targets and transition to electrification:

- European (4): Volvo Group, Daimler Truck, Traton Group, Iveco

- US (1): Paccar

- Asia (3): Hino, Tata Motors, BYD

Heavy Lifting Required: Truck Makers’ Electric Transition found that there are no standout performers, with most HDV manufacturers scoring below three out of five on both ‘quality of emissions targets’ and ‘transition to electrification’ metrics.

Tata and Hino are by far the worst performers, due to uncredible, weak net zero goals, limited vehicle offerings and limited investment in zero emission powertrains. Volvo and Daimler score better, but none of the eight companies has short term emissions targets.

Ben Scott, head of automotive and report author, said: “The lack of short-term targets reduces the likelihood of long-term goals being met and increases the risk of a disorderly transition to electrification.”

Bringing vehicles to market is another key metric against which most manufacturers are failing. A wide range of types of electric HDVs will legitimise the market and instil customer confidence in the technology. But manufacturers are producing relatively few models and in very limited volumes, with most using less than 1% of production capacity on EVs.

The poor performance of leading HDV manufacturers risk putting wider climate goals at risk: Despite only making up 3% of vehicles on the road, HDVs contribute 30% of emissions from road transport and that percentage is expected to grow as electrification spreads across smaller vehicles.

The contrast in transition speed between HDV and passenger vehicles partly reflects structural differences between the two markets. The passenger car market is relatively fragmented, with new entrants like Tesla and BYD pushing electrification. The HGV market, by contrast, is highly consolidated, with 10 producers controlling over 70% of market share and fewer new entrants pushing electrification.

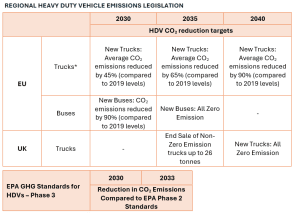

The market’s failure to transition at pace means that these companies are heavily exposed to commercial risks. Regulation in the UK, EU and US will impose increasingly tough targets beginning in 2030. On current trends, most HDV manufacturers will struggle to be compliant with these regulations and risk facing penalties.

Meanwhile, these companies are missing out on an enormous commercial opportunity presented by ‘re-fleeting’ – the replacement of the existing HDV fleet with battery electric alternatives – and risking stranded assets as their ICE production assets become obsolete.

Report author Ben Scott, said: “The transition to electric trucks offers manufacturers a ‘re-fleeting’ opportunity and a huge potential upside in revenues. In the near-term, short and medium-haul logistics represents the easiest prospect for electrification and for HDV manufacturers to capitalise on, as fleet-operator cost benefits are realised.

“However, for long haul logistics more work is needed to help deploy the necessary high-power electric vehicle charging infrastructure. To unlock the full financial potential from the re-fleeting of the existing ICE (Internal Combustion Engine) HDV fleet, manufacturers need to do more to facilitate the rollout of EV charging stations through investments, joint ventures, and partnerships.”

Once the embargo lifts the report can be downloaded here: https://carbontracker.org/reports/heavy-lifting-required-truckmakers-electric-transition/

For more information and to arrange interviews please contact:

Conor Quinn conor.quinn@greenhouse.agency

+44 7444 696 214

Joel Benjamin jbenjamin@carbontracker.org

+44 7429637423

NOTES TO EDITORS

The ‘Quality of Emissions Targets’ score is determined by an analysis of:

- A) Company Emissions Goals and Targets

B) GHG Reduction Strategy Implementation

C) Financial Disclosure and Decarbonising of Capex

The ‘Transition to Electrification’ score is determined by an analysis of how companies are pivoting towards electric powertrains including ZE vehicle model availability, ZE vehicle market share, and investment in enabling technologies (e.g. batteries) and electric HDV charging infrastructure.