The UK will phase-out new ICE vehicle sales by 2035, but an incoherent battery strategy puts the relevance of the UK automotive sector at risk

Recent political events have highlighted the UK as a confusing place for investors interested in the country’s vehicle electrification story. While there are some reasons for optimism, this is marred by an insufficient automotive industrial/ battery strategy and underlines the lack of joined-up thinking between Government and industry bodies.

Unless the UK can reclaim its leadership position on electric vehicle policy, supported by an automotive industrial strategy proportionate to the scale of transformation that the industry is undergoing, investors will instead continue to deploy significant capital in the EU or US (global annual EV capex of ~$400bn and growing), putting the UK automotive industry’s long-term future at risk including:

- Risking losing the 300,000 jobs in the UK automotive sector (direct and indirect). It is estimated that 200,000 jobs alone in UK are related to ICE engine manufacture and are at risk if the industry mishandles the shift to BEVs (Battery Electric Vehicles).

- Missing out on creating equivalent skilled jobs in the battery supply chain.

- The UK becoming reliant on importing batteries for car manufacturing and other energy applications required as the economy decarbonises.

Too much of the discussion today in the UK is hyper-tactical, for e.g. the monthly market share of BEVs, which is important but missing the bigger point. The world of automotive manufacturing has been upended for the first time in a century by the introduction of engines that need no oil and are faster and cheaper to run. Resisting this change, and not building a strategy to exploit it is mass-scale industrial folly. The UK needs to rethink its battery strategy as a priority.

Policy Powers Progress

At the UK Pavilion during COP28, there was much fanfare as the long deliberated Zero Emissions Vehicle (ZEV) mandate was put into UK law. Similar to the California ZEV mandate, this law obligates vehicle manufacturers to sell a minimum percentage of BEVs (Battery Electric Vehicles) into the UK per year.

Starting this year, 22% of new UK cars sold by automakers must be zero emission, with the percentage rising to 80% by 2030, culminating in the complete ban on the sale of new internal combustion engine (ICE) vehicles by 2035.

The ZEV mandate is arguably a more effective mechanism to increase the sales of BEVs than the EU’s fleet average emissions targets. In the EU system the sale of new ICE vehicles is effectively banned by 2035, but until then there are various loopholes automakers use to lower fleet average emissions to meet compliance, including the sale of PHEVs (Plug-in Hybrid Electric Vehicles), which emit many times more CO2 than stated in test conditions.

The UK Government and policymakers should be applauded for handing the challenge to automakers to bring pure BEVs to market, however it should be noted that policy to end the sale of new ICE vehicles was watered down, with the ICE ban moved from 2030 to 2035. The UK thus moved from a leading player in the transition to zero emission vehicles, to one where targets are subject to uncertainty and change.

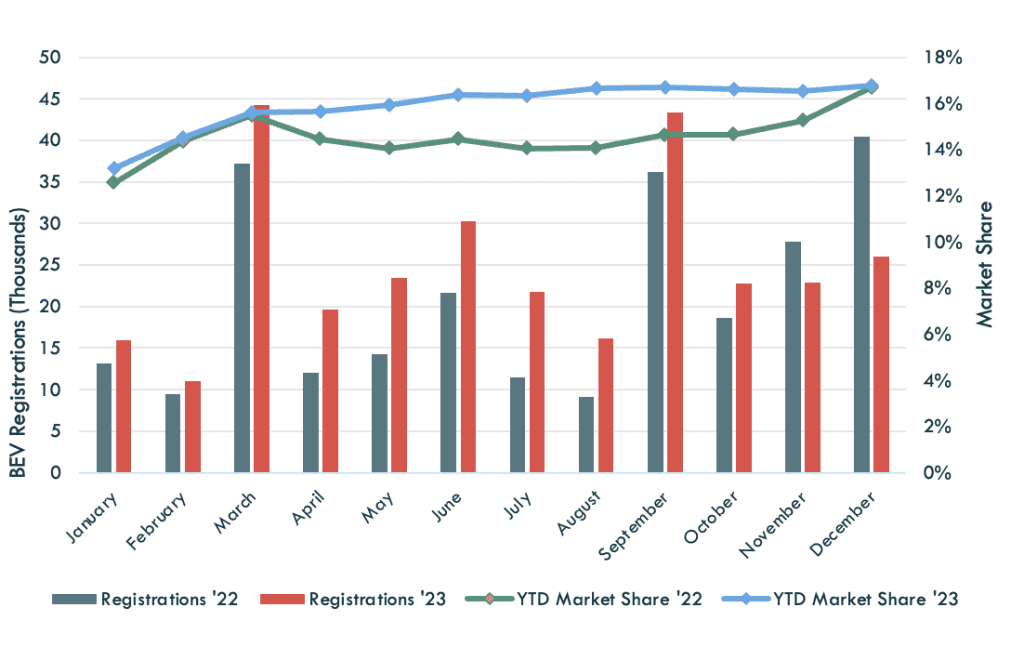

This confusion has certainly influenced industry and consumer confidence, with electric vehicle sales declining 18% and 36% in November and December ‘23 respectively compared with a year earlier, according to data from New Automotive. However, 2023 electric car market share remains steady with 1 in every 6 cars sold being a BEV. It could be argued that automakers deliberately held back the sale of BEVs at the end of 2023 to then register the BEV sale in 2024 as the UK ZEV mandate begins, but the fact remains that the UK has ceded its electric vehicle leadership due to the ICE ban shift from 2030 to 2035, adding uncertainty to the market.

Figure 1: Monthly UK Battery Electric Vehicle Registrations 2022-2023

Source: New Automotive

UK battery strategy – A strategy out of time?

The ZEV mandate has set the course for the UK automotive industry to a complete transition to BEV by 2035, however the absence of a supportive industrial/ battery strategy has slowed investment relative to other competing countries/ regions.

High-cost energy, lengthy planning and less financial support have reduced the attraction of making the massive scale capital investment in UK battery supply chain, putting the industry in an increasingly weak competitive position.

As the US and EU respectively unveiled the IRA (Inflation Reduction Act) and the European Green Deal, in addition to China’s long-term plans to dominate BEV manufacturing, the UK was worryingly quiet about its plans to attract automotive investment, a historically strategic industry for the country.

In a late reactionary move, the Government has unveiled electric vehicle sector investments from a handful of automakers.

Table 1: UK Electric Vehicle Industry Investment Announcements – 2023

| OEM | Investment | Plant Location | Details |

| Tata/ Jaguar Land Rover | £4bn | Somerset | New battery gigafactory, JLR to be main offtaker of batteries |

| Nissan | £2bn | Sunderland | Vehicle production of 3 BEVs |

| BMW (Mini) | £600m | Oxford & Swindon | Vehicle production of 2 BEVs starting in 2026 |

| Stellantis | £100m | Ellesmere Port | Announcement in 2021. Production of electric vans and cars from 2023. |

Source: Public information

The UK Government published its battery strategy in November 2023, but its attitude to the industry is akin to a venture capital (VC) approach. The problem with this approach is that the UK needs gigafactory mass-scale manufacturing now – not with small-scale funding spread thinly. That VC R&D phase has gone – we are in mass manufacturing mode now, and a very different approach needed.

The current UK Government’s battery/ automotive strategy, or lack thereof, has led to the demise of two domestic battery manufacturers, namely AMTE Power and Britishvolt.

The failure of Britishvolt in early 2023 illustrates the limitations of the UK’s VC approach to developing a domestic battery supply chain. The project was reported to have made good progress towards developing a high-performance battery cell, however the absence of any significant customer orders meant the project was not able to secure the necessary multi-billion-pound investment to allow the final cell development and construction of a gigafactory to manufacture at scale.

It is well known that automotive original equipment manufacturers (OEMs) take a very conservative approach to working with new suppliers, and for a component as critical as the battery the supplier approval process would take many years. There is almost no likelihood that an established OEM would place significant orders from a start-up with no proven ability to manufacture a safe and reliable cell at scale. A project of this magnitude needed to have the participation of an established battery technology partner to de-risk the proposition for OEMs and allow the project to accumulate firm commitments in the scale necessary to green-light the final large investment.

The UK battery strategy for local supply chain is now out of time and the end-to-end supply chain approach at limited VC scale is misinterpreting the current state of the market. Huge global players such as CATL and BYD are already dominating lithium-ion battery manufacturing and BEVs with vast industrial scale investment. Both Chinese companies will also construct sodium-ion battery gigafactories this year – this technology replaces lithium with a sodium cathode, reducing costs. This leads these companies into an adjacent high-growth industry: grid storage. As electricity becomes the dominant energy system, the UK risks losing twice in a row (EVs and grid storage) if it doesn’t have a coherent battery strategy.

Move to the Fast Lane: From Battery R&D to Battery Manufacturing

Towards the end of 2023, the UK Government announced it will support the development and manufacturing of batteries and will make available an additional £2bn of support between 2025 and 2030, but this level of investment is tiny compared to an estimated $0.5-1 trillion investment required by 2030 to meet global EV demand. And these UK funds will be spread across the value chain, from upstream mining projects, to midstream processing of minerals, and gigafactories.

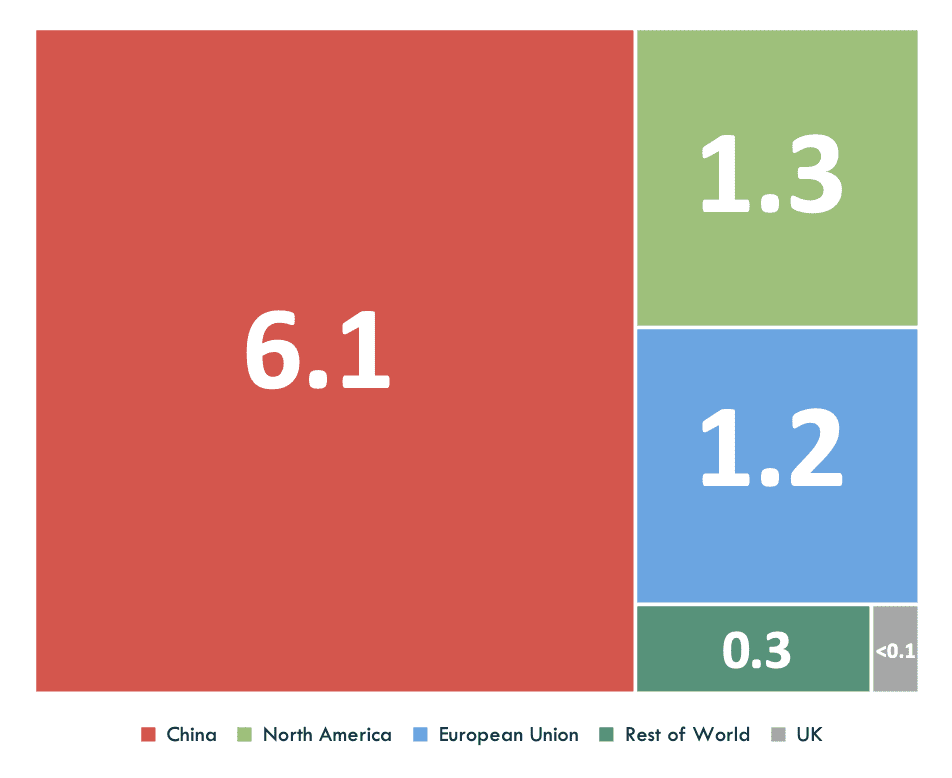

The UK is estimated to need 100 GWh of battery manufacturing capacity by 2030, doubling to 200 GWh by 2040, to support the growth in UK EV production and domestic job creation. But the UK has only 2GW of capacity today with a pipeline of 65GW of announced capacity. Each gigafactory is a large, multi £bn capital project with a minimum 3-year lead time.

Given the higher level of incentives available elsewhere, it will be challenging for the UK to close the battery gap, increasing risk for the UK automotive industry that electrification is easier elsewhere; before the UK has shown it can provide an environment that supports a next-gen battery ecosystem and exposed to the vulnerability of a long supply chain for critical imported battery technologies.

Figure 2: Global Battery Manufacturing Capacity by 2030 (TWh)

Source: Benchmark Minerals

Insufficient UK domestic battery manufacturing capacity will mean importing batteries from the EU and beyond, lengthening supply chains and making the UK an increasingly unattractive location for just in time (JIT) manufacturing.

Putting the UK’s Electric Vehicle sector back on track

The shift to electric vehicles will be fast and non-linear – mixed electric vehicle sector messaging from the UK Government will not help investor confidence. A lack of automotive/battery strategy is limiting the UK’s attractiveness for domestic mass-scale battery manufacturing, while large global players deploy capital to take advantage of this growing market.

For the UK to regain electric vehicle leadership and provide assurances which will facilitate investment, Carbon Tracker suggests the following strategic moves:

- Policy: The UK Government should re-instate the 2030 phase out of new ICE vehicle sales. Prioritise supporting a growing electric vehicle market, to enable growth, job creation and to meet climate goals, and accelerate local future skills development. It should also set out its vision of why this is such a core industry focus for mid-21st century growth in the UK.

- Industry: The UK Government, OEMs and UK automotive businesses should look to leverage and collaborate with strategic battery/EV manufacturers, and to stop focussing on direct competition with small-scale investments. Offering financial incentives from government to established, large-scale battery manufacturers will encourage these companies to set up battery manufacturing in the UK, leveraging currently available battery technology. Partnering with these companies will allow UK businesses to be a core part of the global EV supply chain. Long-term this will support the creation of expertise in battery technology, installation, and assembly – a core skill for the UK transportation sectors, and allowing an option to access the growing grid storage battery expansion that also lies ahead.

End Section