Major oil and gas companies still have choices about how to minimise the risk of having stranded assets, for now.

Early in March 2023 Janet Yellen, the US Treasury Secretary, said that climate change is already having a major economic and financial impact on the United States in a speech we covered here.

Yellen said there has been a 500% increase in the annual number of billion-dollar disasters over the past five years due to climate change, compared with the 1980s, even after taking into account inflation, which increases systemic risk significantly.

This echoes key themes that Carbon Tracker has explored over the last few years.

For example in Decline and Fall: The Size & Vulnerability of the Fossil Fuel System published in 2020, we noted the switch away from fossil fuels to renewables, if not actioned in an orderly and planned way, risks stranding at least $100 trillion of assets across financial markets.

The US Treasury is clearly waking up to this fact.

Some may liken this to a Gray Rhino event – the opposite of the Black Swan risk which is highly improbable and so unforeseen: a Gray Rhino is a clear and obvious risk or danger that individuals or corporations tend to or even choose to ignore.

And as if to underline how systemic risk can stem from a single bank’s exposure to risky assets, a week later came the collapse of Silicon Valley Bank SVB, a result of high interest rates and bond losses in the banking sector, and crucially poor risk management. For some looking for the impact of higher rates this was an accident waiting to happen – and for us all perhaps a lesson on taking exposure to climate risk investments more seriously.

The fall of Credit Suisse later in the month increased the risk profile in the banking sector.

The parallels with climate risk on financial well-being in banks and oil and gas firms are not exact, but there are some comparisons worthy of exploration.

There are some precise analogues: banks with high exposure to fossil fuel investments or climate-related events may have a large exposure now to currently unpriced climate risks that may cause sudden impairment when loanee corporate assets become stranded.

Another commonality is the extent of exposure — for both it is in the high trillions of dollars, as we note in our paper.

However, differences are likely in timing. The systemic risk that Janet Yellen highlights in bond and equity markets can happen in a sudden, almost overnight shock as we saw in 2008 and now this month – exposing some corporations, and many individual investors.

The stranded asset risk in energy is likely a more extended threat, focussing on mostly corporate failure (the market already having down-rated oil and gas stocks for years).

So, one is an acute infection, financial exposure, and now being treated by the US Treasury via investor insurance relief and Federal bank loan innovations.

The other is a more chronic and global one, fossil fuel asset decay in value, which is still being mostly unmitigated by corporations and regulators world-wide. Whilst oil and gas prices remain elevated writedown risks may be limited – but that could change quickly.

As the SVB incident shows, a concentration risk in even a moderate-sized bank in a corner of an industrial sector can lead to rapid contagion of the wider network. Less “too big to fail” and more “too quick to spread”.

The danger for energy stock investors and incumbent corporations is the belief that this lingering condition of decline will be slow and prolonged, and largely controllable. The industry has even invented its own language for this – a plateau beyond the peak.

Plateau or not, this condition might still be treatable if fossil fuel firms start to recognise the future possibility of disorder and act on it now by, for example, reducing exposure to new oil and gas developments, writing down asset values, or closing down assets entirely.

There are some examples of this – for example BP’s write-down of its refinery in Germany by $1.4 billion

But the general industry preparation for the coming decline in fossil fuel demand — as new energy options start to emerge at large scale – appears to be going in the other direction. Continued high investment in long-term oil and gas assets, sometimes prompted by governments over-reacting to security concerns, and superficial risk management of potential downturns.

Add to this increasing level of climate jeopardy.

The IPCC released in March their AR6 Synthesis Report, – its first since 2014 (before Paris) – highlighting the increasing risks of warming beyond 1.5 deg C, and the solutions required. The report, which was more explicit than anything else the IPCC has said about the risks of BAU fossil fuel investment and stranded assets, was notably accompanied by a message from the UN Secretary General – who was at pains to emphasise the IEA message that oil and gas expansion is incompatible with 1.5C.

We’ll discuss the IPCC report and its fall-out next month in more detail – but for now it is clear the financial corporate and climate risks of continued dependence on fossil fuels is rising quickly, and may start to resemble financial market shifts in its speed of transmission. Indeed, the IPCC report may increase that risk by suggesting we plan for overshoot of the 1.5 deg C target – allowing a longer window for fossil fuel development as it is an open-ended concept.

Actions are required to manage these hazards now (as spelled out by the IPCC), reduce transition confusion and maximise asset values (or at least minimise the risks of terminal values of assets tending to zero).

So how are key industry players in oil and gas reacting to these increasingly short-term threats ?

This month we published two significant Transition Plan Analyses (TPA) papers on global oil and gas majors, ExxonMobil and Shell.

There are overlaps and similarities between how the two firms are managing the energy transition, but they do diverge.

Perhaps by nodding to the Anna Karenina principle, transition success may not come necessarily from positive traits, but by avoiding negative ones.

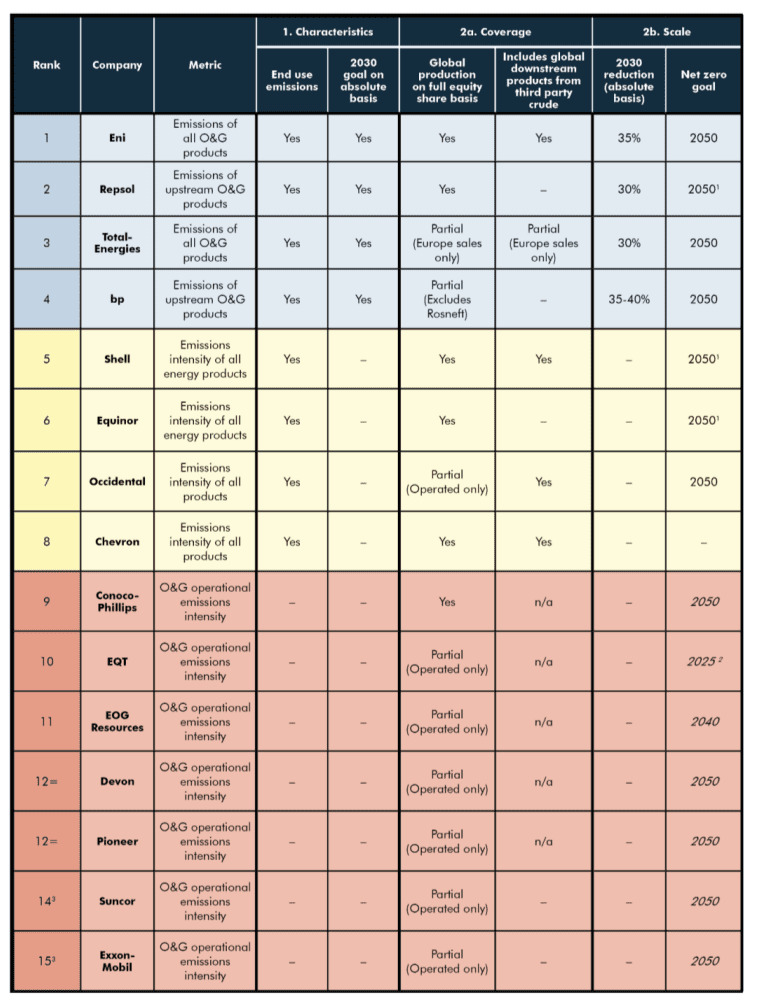

For major oil and gas companies we have created a comparison ranking system for investors to review in terms of readiness planning for the energy transition.

This performs a dual function – noting their progress toward emissions reduction, but also their risk of exposure to the energy transition

The companies were ranked on various criteria, including stretch of their goal across divisions, their breadth across Scope 1, Scope 2 and Scope 3 emissions (Scope 1and 2 cover company direct and indirect activities in their own facilities, Scope 3 cover indirect emissions from the use of their products, burning of fossil fuels in cars), and the use of interim target for emissions reduction prior to 2050.

The league table is shown here, with ranking from most advanced to least:

Table 1: Ranked comparison of company climate goals selected per CTI Methodology

Source: Company Disclosures, Carbon Tracker Analysis

Let’s start with ExxonMobil.

In this report the summary of its transition planning is summarised as

- ExxonMobil is not Paris-aligned due to continued greenfield development and its greenhouse gas targets fail to address Scope 3 emissions.

- The pursuit of growth in its traditional oil & gas business will heighten Exxon’s stranded asset risk profile.

- ExxonMobil’s Low Carbon Solutions business – biofuels, CCS, and blue hydrogen – will NOT become a meaningful part of its business for now.

- Exxon will have to relentlessly pursue a low cost strategy so it can remain a survivor in the energy transition (ET). The competition for that position could be intense. Also we think shale over conventional is a lower risk investment strategy in the ET, as it lessens stranded asset risk.

In the CarbonTracker comparison of oil and gas company goals ExxonMobil ranks 15 out of 15, bottom of the league for efforts in climate reform.

We have already broadly assessed many of these players in a recent work in Paris Maligned which showed the deficiency of their transition planning.

More specifically, in the current report we explain how ExxonMobil shows a number of negative transition traits that other oil and gas firms exhibit too.

- Continued investment in greenfield projects, “planting a multi-billion dollar flag in the next wild frontier” as Bloomberg warned – in 2016

- Production increase targets of 3% pa over the next five years

- Limited investment in meaningful zero emissions technology

- their Low Carbon Solutions business comprises CCS, blue hydrogen and biofuels at a rate of about $1 billion per year through 2027 or about 4% of total capex – and into businesses that require subsidies or tax breaks to stay afloat

- A focus on share buy-backs and dividend increase rather investment in alternative energies

All this even after the activist engagement of Engine no 1, which placed three directors on ExxonMobil’s board to specifically steer the company toward a less fossil fuel driven strategy.

In a way then, ExxonMobil shows that for many major oil and gas producers, it is almost as if there has been no energy transition, and that they discount that there will be one. Business as usual by default.

They seem to be locked in a prison of their own massive asset base and business model, each new long-term project another brick in their self-built penitentiary wall.

A reality perhaps for many major oil and gas companies.

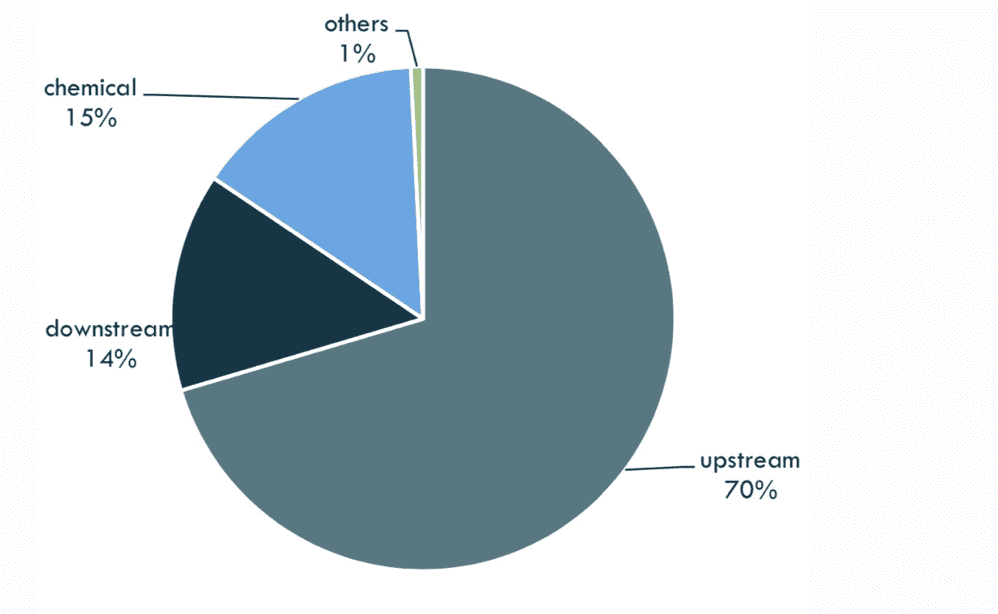

Looking at the company profile by the numbers invested, it’s the 1980s all over again – a pie chart in.

Figure 1: ExxonMobil’s capital employed by division

Source: Company reports and Carbon Tracker

So, despite record profits, their main focus is to recycle finances into shares and dividends – but still take the risk of longer-term project investments.

Their production increase targets, even if achieved, would not bring them back to 2010 production levels. Like many other majors, their reserves base is shrinking, their production is smaller than decades ago, and their capital options are mainly financial restructuring, not expansion.

Their strategy is not Paris Aligned from an environmental perspective, and from an investment perspective, it bets on a slow and long-term transition.

Investors may enjoy the cashflow benefits today – but they should be clear on what ExxonMobil’s strategy means, and the risks it locks itself into.

And so to Shell.

Echoes of the Exxon analysis will be seen here – although Shell ranks far higher in the transition planning assessment table:

- Shell has made a significant effort to improve the amount, depth and frequency of information in its approach to the Energy Transition as well as in introducing an Energy Transition strategy.

- The company believes it is Paris-aligned. However, the lack of interim Scope 3 absolute targets, the long time needed for low carbon activities to become substantial in the group, and the continuing activity in hydrocarbon exploration and new project sanctioning appear to be in contrast with full Paris-alignment.

- Shell’s Energy Transition Strategy contain, as one of its key pillars, the objective to diversify and grow in low and zero carbon activities. It is a laudable but complex objective to achieve, since currently only a minority of its activities matches such a description. Overall, the capex strategy that Shell is implementing for diversifying into low carbon activities makes strategic and financial sense, but there will be significant challenges in its implementation. We also observe that given the huge size of Shell’s hydrocarbon assets on the balance sheet, to convert Shell into a business able to cope well with the tectonic shift of the energy transition, will require a herculean effort for many, many years, and capital redeployment will need to be accelerated significantly.

- Shell’s current Energy Transition Strategy was decided under the previous CEO Ben van Beurden, who retired at the end of past year, after almost a decade at the helm. The new CEO, Wael Sawan, will need to decide if to maintain such a strategy or modify it.

Shell ranks higher in the table because of more detailed targets across the emissions Scopes, and in actually having a codified Energy Transition Plan.

Shell also has targeted some limited production decline over the next decade at 1-2% per year, rather than expansive production targets.

However – as Tolstoy noted in the novel Anna Karenina, each unhappy family is unhappy in its own way.

Shell is still spending the vast bulk of its capital on hydrocarbon activities, and although setting up a “Renewables and Energy Solutions” division, this contains a lot of hydrocarbon assets and operations, and is still a tiny portion of Shell’s profits.

In fact its investment in long-term exploration actually increased in 2022, a harbinger of exposure to decades of future production commitment.

This led the previous CEO Ben van Beurden to note that there was no real prospect on moving into renewables (proper zero carbon ones) in a significant way because he felt you could not make commodity-like returns on them, which is what investors actually wanted: equity exposure to oil prices by proxy, and lots of cash via dividends throughout the cycles.

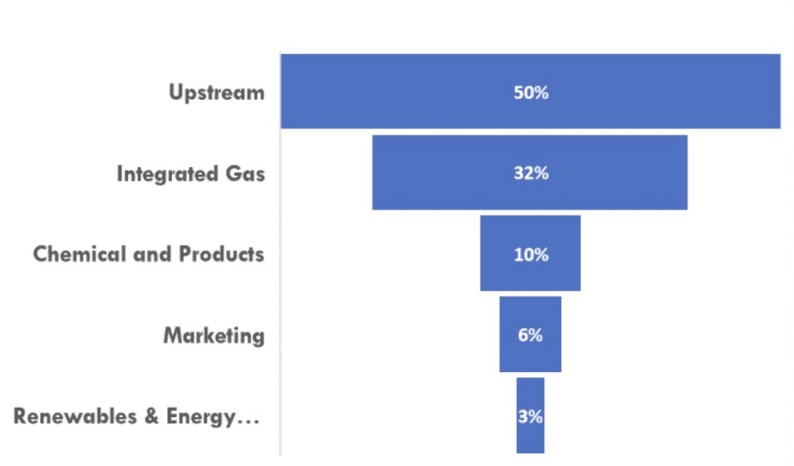

So, if ExxonMobil and Shell are prisoners of their assets, they are also captives of their profits, as our Shell TPA report clearly shows looking at their EBITDA by segment:

Figure 2: Adjusted EBITDA by segment (2022)

Source: Shell Unaudited Resutls 2022, compiled by Carbon Tracker

The new CEO Wael Sawan may take a different course, as we urge in the paper.

But many externally-hired executives in Shell’s new Renewables and Energy Solutions division have come and gone in recent years, suggesting a thick layer of resistance in the main hydrocarbon businesses, in what was recognised decades ago as the “creosote bush” problem in the IT industry, with profitable divisions in a company causing competing divisions to suffer from lack of capital and resources.

The upshot is that these two IOCs, and many like them in the table, have varying approaches to the energy transition, but as Janet Yellen noted, they are at increasing risk of looking solid and financially secure, but then succumbing to systemic risk as the transition takes hold, and demand declines.

In the reports on ExxonMobil and Shell, we suggest many questions corporate and individual investors should ask, and actions the companies should take – the main ones being pare back traditional capex and lower production targets, clearly outline the risks the current strategy runs assuming demand decline, and reinvest in zero-carbon renewables if viable.

However, it seems most IOCs are incapable of structural change at least in the medium term, and are still putting down cement, steel and other resources that will produce hydrocarbons for decades to come, and with hundreds of billions of dollars of company finance every year.

Just more bricks in the wall.

This of course leads also to the increasing risk and costs of decommissioning as demand declines, and those physical assets transform quickly into balance sheet liabilities.

We highlight a recent example in the US state of Colorado here

In early 2022, Colorado overhauled its financial assurance rules for oil and gas companies – this law requires the state’s regulations to ensure that ‘every operator is financially capable of fulfilling every obligation’ imposed under state law, including permanently plugging wells and fully restoring the surface.

We reviewed the potential financial assurance improvements of these rules in Feet to the Fire. The report determined that while there may have been some marginal improvements and would likely lead to increases in financial assurance benefiting the state, it was highly unlikely these rules would approach anything close to full protection for Colorado taxpayers.

What we find is that while some total financial assurance is increasing, the rules fall short of the legislative mandate to ensure that operators can fulfill every obligation imposed by law, and the proposals fall even shorter still.

In our assessments so far, many companies are requesting a steep discount from what the new rules presumptively suggest. Operators are methodically exploiting several the loopholes built into the rules to reduce financial assurance requirements.

A more detailed assessment on various companies can be found here

The upshot is that the fossil fuel industry, whilst still expanding and growing as we noted in the ExxonMobil and Shell reviews, in the less conscientiousness parts of the industry is also attempting to game the asset retirement obligations it is piling up.

Investors – and also taxpayers – beware.

One can view all of this analysis of bull-headed investment into more oil and gas production through a prism of emissions and climate change prevention.

But as we stated at the start of the piece, perhaps the larger picture is that of a Gray Rhino event that the industry may be ignoring as outlined in all the reports and analysis this month.

The Gray Rhino analysis notes there is evidence that groups or sectors, confronting even existential risk, revert to the mechanisms of groupthink such as denial and muddling through, and so often might rather fail as a collective, than take a risk of moving in a different direction alone. The very definition of a looming systemic risk.

Indeed, for all the new language of ESG and Low Carbon or Energy Solutions – the underlying numbers of the oil majors look almost no different to what an analyst in the 1990s or 2000s would observe.

And it is also clear to see how captive to their asset and business model that large oil firms are.

There are some signs of retreat and exit and minimising asset risk in recognition of the new energy era – these should be encouraged as we have outlined. But they look marginal in comparison to forward investment programs, and profit re-cycling to shareholders.

If we are optimistic, perhaps 2023 marks the beginning of a quiet harvesting of assets, a peak in investment in long-cycle projects, recognising that demand does not support such multi-decade risks any more.

But a far faster restructuring is required.

We discuss Stranded Assets as a framing idea constantly.

Like BP’s north-west Geman refinery write-down, stranded assets is an ongoing phenomenon, not a one-off event, and it is now likely to quicken and spread.

To avoid systemic infection as Yellen notes, pre-emptive actions should be planned and implemented.

Phasing out assets can be proactive and orderly – or reactive and imposed by markets or governments and disorderly.

To date, we suggest that the proactive industry actions are still too limited: so the risks of disorderly outcomes pf declining market demand are increasing by the day.

Assets can be stranded in a contained and efficient way: or suddenly closed, or devalued in a reaction to market flight.

Major oil and gas companies still have choices – for now.

But the longer they continue with long-term business-as-usual mindsets and investments into fossil fuels, the higher the walls they are building when they eventually need to exit.