In early 2022, Colorado overhauled its financial assurance rules for oil and gas companies in a rulemaking mandated by SB 19-181.

This law requires the state’s regulations to ensure that ‘every operator is financially capable of fulfilling every obligation’ imposed under state law, including permanently plugging wells and fully restoring the surface.

We reviewed the potential financial assurance improvements of these rules in Feet to the Fire. The report determined that while there may have been some marginal improvements and would likely lead to increases in financial assurance benefiting the state, it was highly unlikely these rules would approach anything close to full protection for Colorado taxpayers. This would happen because of the discretion given to the Commission to allow for downward departures from the requirements.

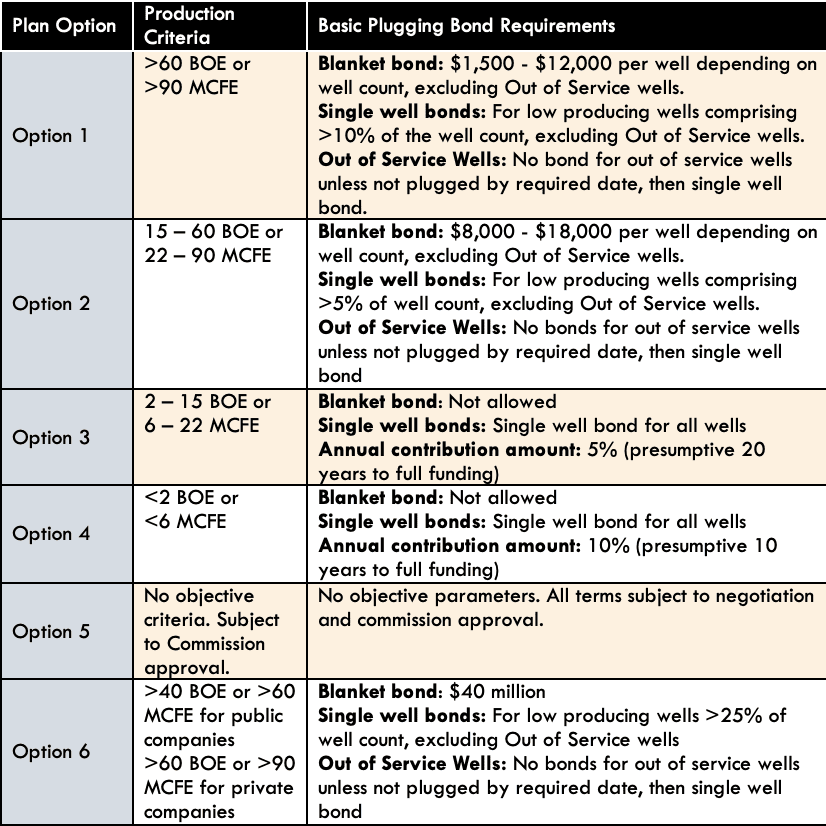

The rules provide for a two-step process for determining financial assurance amounts. First, the Colorado Oil and Gas Conservation Commission (COGCC) calculates the “presumptive” financial assurance amounts for each operator, putting the operators in one of four tiers based upon the average production from their wells. These are based on presumptive plugging costs of $10,000, $30,000, or $40,000 per well, depending on well depth[1], plus $100,000 per site for remediation and reclamation activities.

Second, the operators propose alternative bonding arrangements, including whether wells are designated as “out of service” and thereby excluded from financial assurance requirements.

Now that most operators have submitted their financial assurance plans, we have a chance to test our predictions. We will be juxtaposing these proposed plans with the presumptive financial assurance amounts set out in Colorado’s new rules to determine how steep of a discount oil and gas operators are requesting over the amount of financial assurance strictly required by the new regulations. Our assessments of individual companies’ proposed plans can be found in the Engagement Tools.

To make our assessments, we are analyzing data published on COGCC’s database and corporate attestations in the financial assurance plans and are comparing our base case (financial assurance amounts indicated by the presumptive plan guidelines and regulatory cost calculations) with the plans proposed by Colorado operators.

What we find is that while some total financial assurance is increasing, the rules fall short of the legislative mandate to ensure that operators can fulfill every obligation imposed by law, and the proposals fall even shorter still.

In our assessments so far, many companies are requesting a steep discount from what the new rules presumptively suggest. Operators are methodically exploiting several the loopholes built into the rules to reduce financial assurance requirements. In some instances, proposed financial assurance amounts barely exceed what companies hold under the old rules, and in others, the proposals may be less than what was previously required.

Importantly though, these plans are not yet approved. The purpose of this exercise is to shine a light on the proposals emerging under the new rules. Ultimately, it’s up to the COGCC to decide if these plans fulfil the intent behind SB-181 of protecting Colorado taxpayers from taking on the cost to retire the oil and gas industry.

The data from the proposed rules demonstrate several tactics used by operators to avoid providing the presumptive financial assurance required. These include:

- The hail Mary: This is the primary reason for the significantly lower financial assurance amounts proposed. These operators forego the options 1-4 for option 5, which essentially allows the company to select its desired bonding amount, regardless of the risk posed to the state. These plans typically result in the operator not proposing any single well financial assurance as otherwise required for low producing wells.

- The bargain basement plug: The COGCC itself has determined that it may cost around $110,00 to $140,000 to plug a well and reclaim a site. Even though these numbers will vary in practice, including with respect to gas wells, shallow wells, and easily accessible wells, and well bore integrity, many operators have proposed unreasonably low amounts. Some proposals are as low as $3,168 per well—an amount unlikely to cover the day rate for a workover rig or mobilizing equipment to the site. In some cases, operators have asserted that the resale of topside infrastructure will make the plugging costs minimal. The COGCC has invited this by eschewing the relevant financial assurance amount, i.e., the amount it will cost the state and its taxpayers to plug the wells, and allowed operators to provide “demonstrated” costs, i.e., the amount the operator argues it will cost them to plug the wells. It will now be up to the COGCC to assess whether these low amounts are reasonable, particularly in light of their own experience plugging wells.

- The deep discount: Some operators are seeking to maintain or even lower their financial assurance requirements under the rules. In some cases, the total amounts companies propose end up being lower than the annual payments they would be required to make under ten or twenty-year funding plans under the presumptive bonding requirements. These results are at odds with the intent of the rules.