At the end of February, Italian oil major Eni announced new carbon emissions reduction plans. While not aiming for net zero across all emissions, and hence attracting less attention than BP’s and Repsol’s net zero plans, they are significant in their own way – in particular, because they appear to confront the prospect of a managed decline in oil and gas production more directly than peers.

Maximising value/minimising transition risks and aligning with the Paris goals will require companies to sanction a smaller subset of low-cost projects going forward, maximising margins while shrinking production in absolute terms. However, they seem reticent to (publicly) acknowledge this for their own portfolios. For the most progressive producers there are signs of a tentative shift in messaging, but conviction and detail are still sorely lacking. Perhaps a more whole-hearted commitment would be rewarded by the market.

Oil and gas industry targets often allow increased CO2 emissions in absolute terms

We have been critical of the way that many oil and gas industry emissions “ambitions” (never framed as formal binding targets) are formulated – often in relative intensity terms as tonnes of CO2 per unit of energy produced. This thereby allows companies to produce a level of emissions in absolute tonnes of CO2 that remains flat, or even increases, as long as they also add low carbon power to their portfolios at a greater rate. Indeed, Shell is explicit that its strategy for hitting its intensity ambition is to “keep increasing the share of such low-carbon energy products in our portfolio, while also developing carbon sinks” rather than contemplate lower oil and gas production (as we have previously discussed). Highlighting this, 25% of its CEO’s bonus is tied to increasing fossil fuel production volumes.

Unfortunately, this approach does not square with the physics of our planet, which requires emissions to fall overall on an absolute basis and reach net zero globally in order to stabilise temperatures at any given level – the concept of a finite “carbon budget”. A world that has lower emissions and hence less fossil fuel use will have smaller fossil fuel producers, hence companies will need to be prepared to cut output or risk wading into overinvestment and stranded assets. We explored these issues in our 2019 report “Balancing the Budget”.

In recent months there has been progress on this from some of the industry leaders. BP, under new leadership, framed its own net zero emissions ambition in terms of absolute reductions. Repsol’s aim, while framed in intensity terms in the interim, reaches net zero in 2050 which at least sets an absolute end point. At net zero, intensity and absolute approaches give the same result – emissions intensity of 0 tonnes of CO2 per unit of energy results in 0 tonnes of CO2 no matter how much energy is produced.

Eni’s emissions targets would seem to imply absolute reductions in oil and gas production

Alongside net zero targets relating to its own operations, Eni sets a mixture of relative and absolute targets for the full emissions (including from use) related to its production:

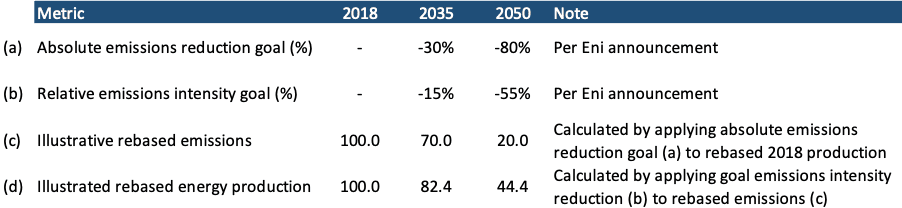

- Absolute – reduce net lifecycle emissions (Scope 1, 2 and 3): -30% in 2035; -80% in 2050 (vs 2018)

- Relative – reduce net carbon intensity of energy production (Scope 1, 2 and 3): -15% in 2035; -55% in 2050 (vs 2018)

These numbers therefore do not reach net zero, unlike BP and Repsol. However, they do appear to imply lower oil and gas production more explicitly. As the absolute goal requires emissions to fall at a rate faster than emissions intensity improves under the relative goal, energy production must be falling overall.

Let’s wheel out the back of the envelope and put some quick numbers together to illustrate this. Imagine that 2018 production (oil and gas combined on equivalent basis) and emissions are both rebased to 100. For Eni to meet its 2035 goal would require absolute emissions being 30% lower, making 2035 emissions 70. If it also meets its ambition to lower intensity of production by 15%, that implies production in 2035 of 82.4 (70/0.85) i.e. a drop of nearly 18%.

Source: Eni, CTI analysis

This appears to challenge the prospect of producing more while lowering intensity. Indeed, if absolute emissions are lowered by -30%, in order to maintain flat production Eni would have to also cut intensity by a commensurate -30%, far more than the -15% aim. Accordingly, Eni must either be planning to absolutely smash its goals, in which case they should arguably be made more stretching, or be contemplating absolute reductions in production.

Going further, Eni’s production grew by 1% from 2018 to 2019 and its plan earlier this year outlined 3.5% annual growth from 2019 to 2025, which would put it at rebased production of 124.3 in 2025. Getting from production of 124.3 in 2025 to 82.4 in 2035 is quite a step – equivalent to a -4.0% p.a. compound rate of decline, which is suggestive of very little new project sanction post-2025. This near-term production forecast is now likely to be reduced by project deferrals resulting from subsequently-announced capex cuts, but the wider point remains.

Perhaps the precise definition of the emissions covered by targets allows increased production in some way that we have not appreciated. So, is Eni projecting reduced production over time, or not?

Imply or explain?

Eni doesn’t put it quite so bluntly; indeed it gives messages that seem somewhat mixed. It notes both a “flexible production profile from 2025” and a “production plateau” from this point. In its annual report, it states that it is planning 14 projects to give “flexibility and growth options” subsequent to its 2023 action plan.

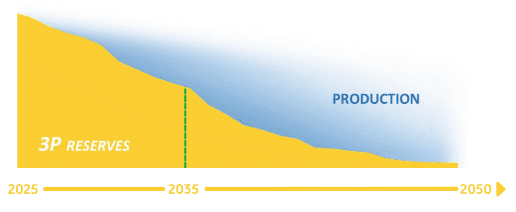

A chart in its strategy deck (see below) shows falling production from “existing” 3P reserves from 2025 onwards. However, this doesn’t necessarily confirm overall production decline in itself – there are plenty of examples of companies pointing to lower risks for current reserves, for example citing relatively short proved reserve lives, while apparently ignoring that they continue to reinvest cash flows into new projects. We are also unsure as to the significance of this illustration using 3P reserves, which are statistically unlikely to be achieved in the first place.

Source: Eni

A couple of other companies have alluded vaguely to lower production. Equinor refers to the “scale and composition” of its oil and gas portfolio playing a “key role” in achieving its -50% intensity reduction. BP CEO Bernard Looney expects to “invest more in low carbon businesses – and less in oil and gas – over time”. On our reading Eni appears to be the first to put numbers on this concept, even if it can’t quite bring itself to say it out loud.

Companies need to invest in the right assets, not just fewer

Companies’ actions on climate can be viewed through two lenses: firstly alignment, i.e. lowering emissions, and secondly risk, i.e. minimising financial downside. From a financial perspective, the issue isn’t just about getting smaller for the sake of it – a company can attempt to align with the Paris goals by reducing production and hence associated emissions, but if it holds high-cost fossil fuel assets then it may still generate poor returns for investors in a decarbonising world.

At Carbon Tracker, we prefer an approach that marries both of these aspects – heightened capital discipline and cost control resulting in lower production as fewer, but on average better, projects satisfy the hurdles for approval.

Here again, Eni talks the right language, highlighting the average breakeven of its development projects. We don’t think that an average is sufficient in itself as it may obscure weaker projects, but the logic is sound.

Small but perfectly formed

Despite the “value over volume” mantra of 2014+, CEOs seem to believe that they need to maintain a volume story. This position is hard to explain, given the outperformance of ConocoPhillips during its “shrink to grow” period.

With growing investor concern around transition risks and the de-rating that the oil and gas industry has experienced in recent years, we wonder whether being clearer about a strategy of managed decline for fossil fuel operations would actually unlock value over time by giving the market greater certainty about future resilience in the energy transition. If linked clearly enough to alignment with the Paris goals, it may even open up a new group of buyers in the rapidly growing quantum of funds managed to an ESG mandate.

Ørsted, formerly Danish Oil and Natural Gas, announced in 2017 that it would sell its entire oil and gas business and dedicate itself fully to renewables. Since then its share price has strongly outperformed its old oil and gas peers, with a total return of 155% while the S&P Oil & Gas Exploration and Production Index has delivered -60%. However, we have yet to see a company truly commit to and detail a near term plan of Paris-aligned managed decline, rather than immediate exit. If and when the first company puts such an approach front and centre in its strategy and communications, a positive market reaction may give other management teams the confidence to do similar. Some industry leaders appear to be edging towards this position.