Navigating Peak Demand: the oil and gas industry enters its post-imperial age

Most things may never happen: this one will

Despite a decade of noting the risks of over-extending investment in oil and gas production, and risking trillions of dollars in stranded assets, Carbon Tracker finds itself as 2023 ends picking through the final options available to the industry as oil demand closes in on its peak, before entering decline.

Ahead of COP 28 (the 28th UN Climate Change Conference) in Dubai we released two major reports Navigating Peak Demand – a follow up to our previous assessment in early 2022, Managing Peak Oil, and PetroStates of Decline

We will focus on these reports below, and also review a related blog which highlights the cautionary tale of business as usual oil investment in the UK: Are more UK oil and gas licences really the answer?

In Navigating Peak Demand we consider two scenarios of future oil demand representing a moderate and a fast pace of transition – and what it means for the industry and investors if they stay with today’s business as usual (BAU) strategy.

Global oil and gas demand has been a low-growth story for many years: even without new energy sources the competing forces of expansion and decline have pushed the industry into an equilibrium, a flat-line pattern.

Yet now with the addition of fast-paced renewables, that flat pattern is turning into a peak followed by decay.

Over the past 10 years renewable energies – mainly wind, solar, batteries and heat pumps – have dropped in cost by 50-90%. Their exponential deployment now means for example that in Europe wind and solar alone provide more power (22%) than fossil gas (20%) for the first time, and global investment in wind and solar alone now outpaces that of oil and gas for the first time too in absolute value at over $500bn pa.

Industrial scale new renewables, allied with mainstays of nuclear and hydropower, are now forcing an energy industry tipping point, and at a fast pace of change. Together these forms of energy already supply 18% of primary energy and are on course to produce 30% of primary energy by 2030.

A key example: to meet the Net Zero requirements in IEA scenarios the deployment of wind and solar will need to treble in capacity by 2030 from 3.6TW to 11TW. And that is exactly what many analysts and governments now expect to happen.

Renewables allow mass electrification in various sectors beyond power, such as transport and heating to force fossil fuels on to a plateau of demand, and in many regions and sectors already into a full-scale decline.

An unbiased observer looking at the energy landscape will now see fossil fuel peaks emerging like a mountain range coming into view: peak combustion engine car sales in 2017, peak gasoline sales 2023, peak emissions in the power sector likely 2023, peak emissions across the energy sector also possible in 2023, probable by 2025.

Peak emissions to be clear are a lagging indicator of change: if emissions have peaked it is very likely that fossil fuel consumption has peaked in advance.

Commentators such as the IEA, typically cautious in this space, announced in their latest World Energy Outlook (again) that no new oil and gas exploration is required to meet the declining future demand.

Even in their most guarded scenario (STEPS), the IEA have brought peak oil demand further forward to occur in the next couple of years.

And in a mid-range scenario demand for oil, which pushed 100 million barrels a day in 2019, is set to fall to about 93 mb/d in 2030 and then further down to 55m b/d in 2050 if current government policy pledges are met. Their Net Zero scenario is even more bleak.

Whistling past the graveyard: Peak Demand as a reality, not a scenario

The scenarios we consider in detail below from PRI (moderate and faster) also point to two fundamental issues regarding global oil and gas demand:

First, peak demand is projected to occur in all main scenarios this decade, and in some perhaps this year.

Second, this new age of oil demand growth coming to a halt closes many options that the industry sector has chosen to assume it still has.

This is because the industry works in long investment and production cycles typically spanning horizons of 10-20 years.

With a demand peak now imminent, measured more in months than years, any significant structural actions to avoid over-supply or diversify the business model would have had to be implemented in detail many years ago.

As the Navigating Peak Demand report outlines in detail– this leaves the industry with very few if any pro-active opportunities, and at best a limited range of reactive decisions.

Companies that continue business-as-usual investment to replace or even expand supply will be pursuing “a dangerous strategy” as the report notes, one that could leave them highly exposed. New conventional oil and gas projects developed today and then entering production may never be profitable, except at the lowest breakeven prices.

Many oil and gas companies claim that they are well equipped to lead society through the energy transition, but the report notes that leading oil and gas firms contributed just 1% of global renewables investment for 2022, and just 2.5% from their own capex budgets.

Despite the rhetoric, little investment is therefore happening and those looking to diversify may well have missed that boat.

And as demand growth grinds to a halt OPEC has taken the most reactive route possible: it has restrained supply for almost a decade, turning down the taps to put a floor under prices.

In this world of deteriorating demand, international and national oil firms could become motivated to maximise receipts while they can.

So, these companies and their stakeholders should consider the risk of OPEC deciding to suddenly produce at levels which drive prices down to a level which is unsustainable for listed companies.

Navigating Peak Demand becomes a major strategic judgment – if diversification is no route out, and continued expansion increasingly high risk and with OPEC’s actions unpredictable and open to rapid change, what should be the path to take in the post-peak environment?

What future of oil demand to plan for?

Navigating Peak Demand looks deep into this issue, and the options and pathways ahead for oil and gas firms – now the risk has leapt from probabilities on a page into a real-world problem.

This report builds on Managing Peak Oil, and arms investors with the information needed to assess oil and gas companies, by:

- Demonstrating the demand substitution impact of an accelerating energy transition on project viability.

- Outlining the strategies open to Upstream businesses, and a clear framework to assess these

- Reviewing the potential diversification options (if any) for these companies, including into CCS and renewable energy.

- Providing key questions for portfolio managers to ask of their investee companies to assess risk exposure and incentivise change.

- Identifying the key considerations for policymakers and financial regulators.

First – let’s look at the tight corner oil and gas companies have got themselves into regarding demand and supply.

Then second, let’s look at their options, both good and bad.

Demand and supply:

For demand the paper takes the moderate UN IPR Forecast Policies Scenario (FPS), and a faster one the Required Policies Scenario (RPS).

For supply it uses two scenarios: a Business as Usual (BAU) case aligned with the IEA’s Stated Policies Scenario, the likeliest supply profile to 2030 we have today, and a special Managed Investment case that Carbon Tracker have derived using lower break-even prices.

There are three big take-aways from this analysis

- Demand even in the moderate case is still below current and soon-to-be added supply: in the faster demand decline case even current supply, with no more investment, is close to meeting demand – which is why the IEA is saying “STOP”

- We can put this another way – supply is now chronically higher than demand: so as peak demand is reached (expected now), oil and gas companies have to navigate enduring over-supply that is set to get deeper and deeper.

- The impact on prices is forecasted to be far less smooth or level as physical demand / supply volumes: long-term prices will likely fall sharply as supply continuously outpaces demand. And even the first indications of long-term over-supply could cause prices to collapse. Both profit and loss and capital NPV impacts could be substantial even in the very short term.

Oil and gas firms are now near the time where medium-term decisions or options are starting to run out of roadway.

So, what options do oil and gas firms have to navigate this new demand decline terrain?

The paper summarises two broad alternatives, and it also considers what to do with capital historically re-invested if companies favour a lower investment route in hydrocarbons.

What paths to take?

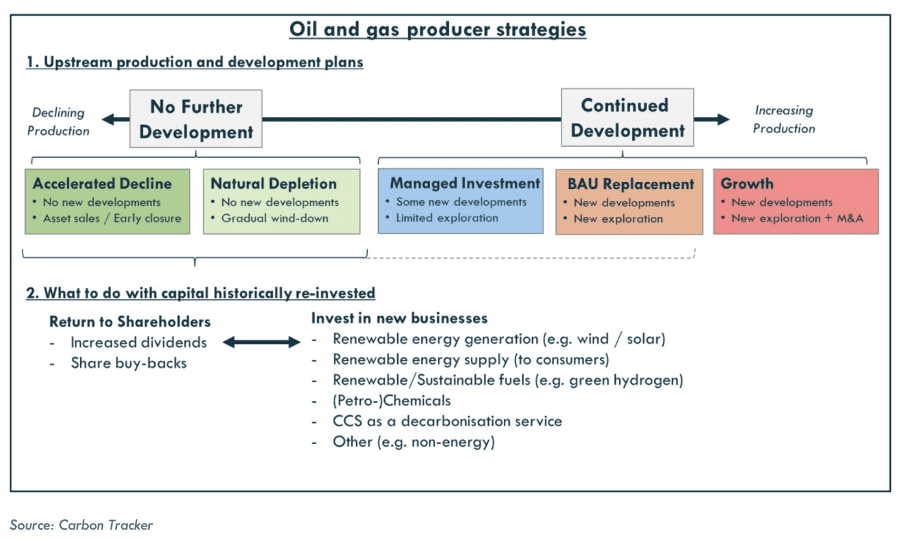

Figure 1: Strategies for companies with upstream oil and gas production business

Step 1 – Upstream Production Planning

No Further Development – Accelerated decline or natural depletion

A strong form of this would be to stop new project new exploration and development options as corporate strategy and to focus on sales/closure of marginal assets.

A more restrained version would be to stop development and focus on a more gradual natural depletion: conserving capital, and reducing future exposure.

Continued Development – Managed Investment, BAU and Growth

The paper argues against this strategy for the many reasons outlined: peak demand, stranded assets, misaligned with global policy responses and misreading rapid alternative technology developments in renewables.

However, the statements from IOCs and the actions of NOCs suggest many major players have decided to follow this route in the belief peak demand is either a long way off – or even if it occurs, the impact will smooth and measured.

Step 2 – What to do next with capital historically re-invested?

In either case conserved capital can be recycled into financial management such as increased dividends or buy-backs or put into new oil and gas developments and also speculative investments into new businesses such as renewables.

In spirit the IOCs still propose a growth bias, but the NOCs in practice are looking to follow as they have many extra-corporate considerations –e.g. national state strategies of energy security and fiscal wealth.

But yet again the numbers contradict the narrative: OPEC, especially Aramco, continue to restrain production, and diversification includes some renewables, but the vast majority of its capital still goes into oil and gas supply projects, whilst it aims to produce less oil and gas near-term.

In sum – as the author Mike Coffin pointed out in the report release:

“There is no one-size fits all approach for what to do to with cash that would historically be reinvested. With the right combination of technical and commercial advantage then some new areas may be attractive, but becoming a growth business in a new sector is not a simple transition… It may well be in the interests of shareholders for companies to pursue a cash out strategy as production declines, and incentives, both for companies and their leadership must reflect this option.”

Key findings to study include:

- The energy transition poses a huge demand substitution challenge to the fossil fuel industry – it cannot simply be dismissed as some ancillary ESG concern

- A strategy aimed at maintaining, or even growing, production via significant new development and exploration is increasingly risky

- We identify at least $200billion of capex associated with planned and proposed oil and gas projects that are unlikely to be financially viable under even a moderate transition scenario– and over $450billion at risk in a more rapid one.

- To support shareholders, companies must make clear the demand and price forecasts that underpin business planning and strategic intentions.

A number of key questions for investors and policymakers to ask companies are also covered including:

- What demand scenario is the company using in its central planning case?

- Are the company’s commodity price forecasts consistent with that scenario?

- Why is a diversification strategy value generative vs cash-out?

And for National Oil Companies, who are even more compelled to invest further in fossil fuels as it underpins their entire economies, the implications of peak demand are even more stark.

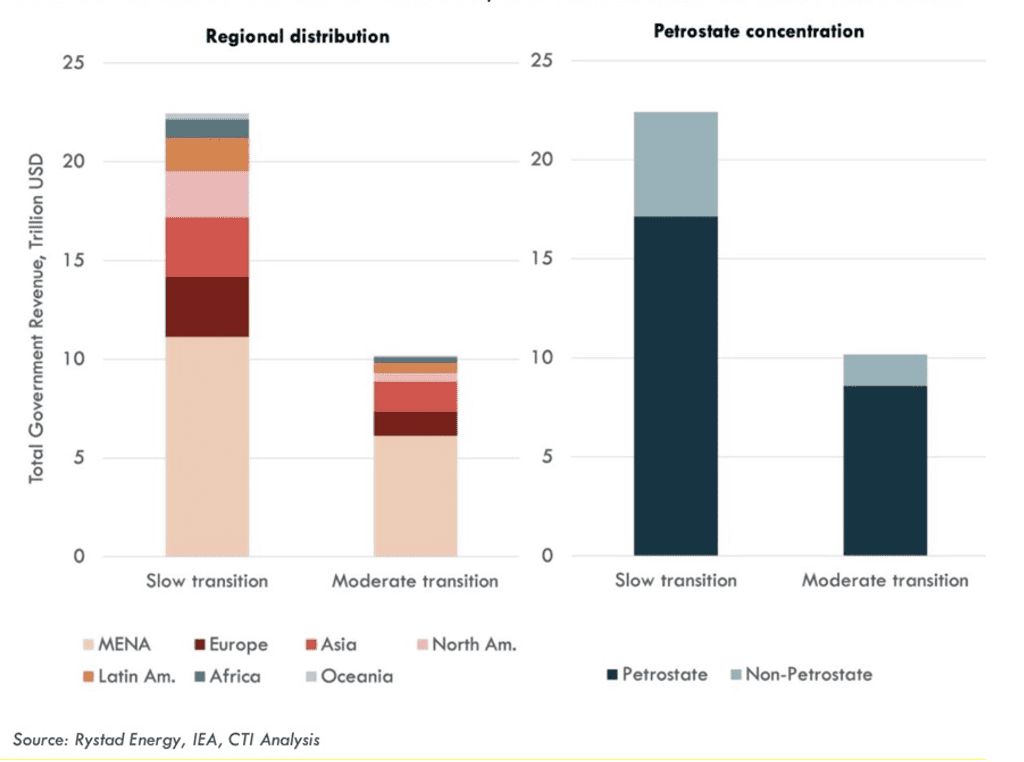

Our latest report, Petrostates of Decline analyses 40 countries with a high economic dependence on oil and gas revenue.

It calculates how much their governments rely on revenues and how far these are likely to fall over the period 2023-2040 in a moderately paced transition consistent with limiting global heating to 1.8°C.

The report aims to highlight petrostates’ vulnerability to the energy transition rather than predict the future, but its warning is clear – Petrostates could lose up to half their expected revenues by 2040.

That is a shortfall of $8 trillion dollars.

It finds that 28 petrostates in total would lose this expected revenue – even in a moderate transition, which in fact could go far faster as we outlined above.

That is a massive collapse in fiscal receipts that are expected to support these state economies, and at a time when many of them in, especially in Africa, are going through a population boom.

For example, the UAE (of which COP28 host Dubai is a member) relies on oil and gas for 40% of government income – – but production revenue could be 60% lower than expected.

Figure 2: Future Global Government revenues (2023-2040) for all countries under slow and moderate transition scenarios, split by region and by petrostates status

All countries dependent on oil and gas for national income are massively exposed to oil’s variable demand and consumer reactions – but at a time of a structural peak in demand, the risks are now much larger.

This includes mature incumbents such as Saudi Arabia, but also new entrants to oil and gas development such as Guyana.As the report notes:

“There are countries now which are looking to the oil and gas industry as a future for growth for that country, and we really have to question is that the right path forward?”

Navigating Peak Demand noted the financial stress that will likely occur for international companies doggedly pursuing expansion: for incumbent and emerging Petrostates the risks will go further to impact sovereign debt, credit ratings and cost of debt-financing of any new projects.

All of this should be a clear warning signal to investors of the credit risks of allowing international and national oil companies to pick their preferred demand scenarios, plunge on into new production, and ignore the discipline of evidence-based financial planning.

For sure the oil and gas industry, especially national champions, have ridden cycles of high and low prices.

But for the past decade oil demand has increasingly coasted toward zero growth, renewables have become established rapidly at global scale, and the industry now clings to the hope of demand somehow resurfacing after a decade of production cuts lead by NOCs.

Petrostates of Decline outlines those oil-concentrated countries most at risk, options to limit the risk of over-investment, and the impact on national governments and international investors – as another example of navigating the reality, not the scenario, of peak oil demand.

And so finally we turn to the North for a short story on how this all may play out.

A Cautionary Tale: the mature basin of the UK North Sea

This month we also published a short review which takes the peak demand analysis and turns it towards the example of the UK North Sea.

Are more UK oil and gas licences really the answer?

Despite all the analysis and scenarios and the UN and IEA pleas for no more new production and expansion, the UK government over the past decade has continued to issue new licensing permits for hundreds of fields – most recently in the cause of “energy security”.

Yet literally only a handful of licences have seen (limited) investment as the UK basin is in a very late life phase.

UK oil and gas production has fallen 70% from its peak in 2000 and will fall further to 90% lower by 2030 – even with new licences.

Also consider the UK midstream – this month also saw the announcement that the last refinery in Scotland, Grangemouth, is to be closed down. Built in 1924, from 2025 it becomes just a storage site for foreign fuel imports.

And finally in end-use in UK transport, despite a relaxation on bans on sales of oil-fired cars, sales of EVs have accelerated to 20% market share from zero in the last few years, just as sales of diesel cars have dropped from 50% market share to 5%. (Note – We will cover this transition issue in more detail in next month’s monitor where we discuss the impact of the ICE to EV rapid switch in the Global South – the report is here).

A microcosm of global change

Peak oil and gas demand speaks to all these underlying rapid changes – it is not an isolated event, but the culmination of several key transformations in the energy sector: a long-cycle global phenomenon now causing short-cycle reactions in various sub-sectors e.g. in the UK, and as noted potentially in the investment decisions IOCS and NOCs and Petrostates.

One can argue change is obvious and will happen anyway – but the vibe being given by industry leaders matters too. It signals comfort and confidence in the status quo when the exact opposite may be true – putting investor capital at much higher risk than is being publicly expressed.

Major players such as states and corporations now find themselves at a crossroads – because the routes to efficient capital management are diverging quickly in outcomes.

One leads to managed decline in the existing oil and gas sector and recognising the pace of change.

The other, the business-as-usual path, leads to an over-confident belief that demand will always persist, and that supporting it is the safe thing to do. We worry about that path.

Coda

We began with Larkin’s poem on how things reliant on earth-bound finite resources – a human body, an oil field – will always have an end.

To paraphrase: Most things may never happen: but Peak Oil Demand will.

——————

References

Carbon Tracker

Navigating Peak Demand

Peak Demand Press Coverage

Petrostates of Decline

Managing Peak Oil

Are more UK oil and gas licences really the answer?

Driving Change

Other References