Key Resources

Press Release

Switching to battery powered electric vehicles will save the Global South over $100 billion annually

Read MorePolicy Brief

Résumé Analytique

Résumé Politique

Key Quotes

Unlocking the economic potential from vehicle electrification

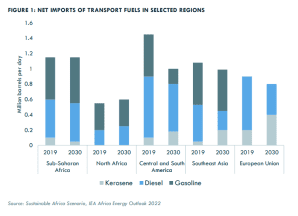

The global deployment of Battery Electric Vehicles (BEVs) is geographically split; the passenger vehicle fleet in the Global North is rapidly decarbonising through deployments of zero tailpipe emission vehicles. Conversely, new and used BEV sales volumes in the Global South remain at present insignificant. This is largely to be expected in the short-term, as most new vehicle sales are in developed countries; while the Global South continues to be predominantly an export destination for used internal combustion engine (ICE) vehicles from the Global North.

This state of affairs has reduced the Global South – where new vehicle sales are limited to companies operating in the region and wealthy private individuals – to a passive role in the overall automotive market, with limited accessibility to affordable vehicles.

It’s therefore a key question, which Carbon Tracker examines in this report, about whether – as the tipping point for BEVs approaches and the associated electric vehicle technology moves down the cost curve – the Global South will have the opportunity to leapfrog the incumbent ICE regime to BEVs and play an active role in the automotive market.

There are significant barriers standing in the way of this opportunity, in part because car manufacturers who have been grounded in a fossil fuel-based transport system (and as they see new ICE sales decline in the North) may transfer their target markets for new ICE products to the South.

Key Findings

- The Global South’s reliance on ICE vehicles, and the dependency on fossil fuels, is not benefitting the region economically. The Global South fleet is dominated by ICE (Internal Combustion Engine) vehicles, most of which are used car imports from the Global North and China. Despite having net zero ambitions, most automakers aim to continue ICE vehicle sales in regions with no/limited vehicle emissions policy i.e. the Global South. This will exacerbate the Global South’s dependency on fossil-fuels for transportation.

- Unless positive policy action is taken, there is a risk the Global South will become indefinitely locked into this fossil fuel path dependency. In the short- to mid-term, the Global South will import even more ICE vehicles as the Global North substitutes its fleet with BEVs (Battery Electric Vehicles). In the longer term, used BEVs will stay within the Global North region and recycled for critical battery materials circularity. This means the Global South will not have access to used BEVs, rather instead a dwindling pool of used ICE vehicles.

- The Global South can leapfrog to BEVs: BEVs lower barriers to entry for domestic manufacturing, for market and country participants, and opens other opportunities across the value chain. Electric vehicle technology has already progressed to a stage where the Global South can remove its dependency on fossil fuels and effectively leapfrog to BEVs.

- Taking advantage of BEV technology improvements now means Global South countries can reap financial/ economic rewards, as well as lower costs for consumers (vehicle purchase price and operating costs). Delaying the switch to BEVs would be detrimental to Global South countries and a missed opportunity that could be lost indefinitely if swift action is not taken.

- For the leapfrog to BEVs to occur (point 3) and for the Global South to benefit from the transition to zero emission mobility, first there needs to be a policy environment conducive to enable widespread adoption of BEVs. Policy actions include an emissions policy to phase out ICE vehicle sales, both new and used, alongside a comprehensive industrial strategy to facilitate involvement in the BEV value chain and infrastructure, including incentivisation of domestic BEV manufacturing and sales.