2024 is the Chinese year of the Dragon, the only mythical beast in the Chinese zodiac: and a year typically associated with fresh starts.

Carbon Tracker’s late December 2023 and January 2024 research output reflects this turning arc of time, and the looming impact of the world energy transition in 2024.

This could be accommodated efficiently, if total energy demand growth is steady, and the two energy systems of renewables and fossil fuels collaborate.

But they almost do the opposite – renewables grow quickly as technology learning curves improve, meanwhile, the oil and gas incumbent attempts to grow too, even as its technology becomes outdated, and its product demand is dwindling.

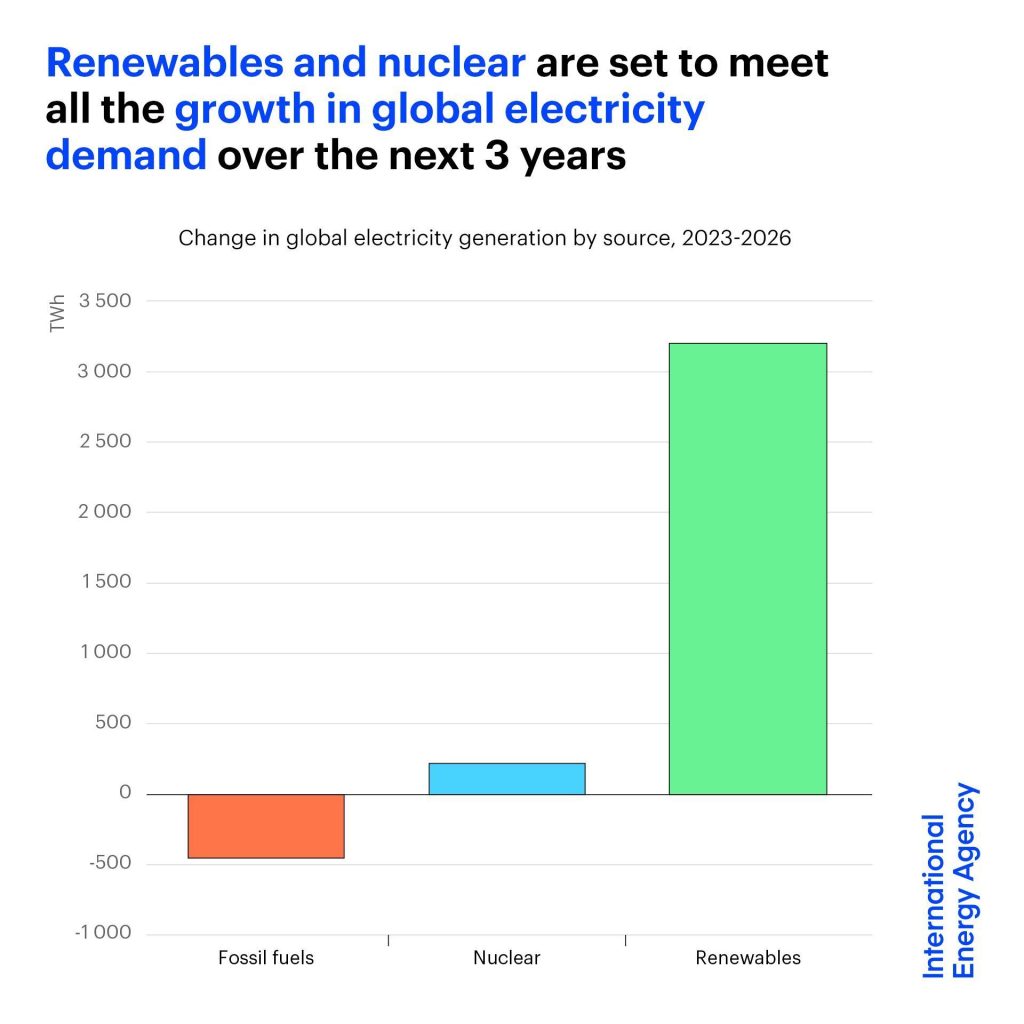

The result will soon be an energy glut, with too much polluting carbon in the energy system forcing fossil fuel production declines – a key example noted here in the global electricity sector by the IEA in a 2023-26 outlook released In January 2024.

Figure 1: Change in Global Electricity Generation by Source, 2023-26

Source: IEA. Licence: CC BY 4.0

The good news is that this will make 2024 the first year of emissions decline in the global power sector.

The less good news is that as renewables eat into demand in other sectors, such as transport, where oil and gas firms stubbornly refuse to react in a disciplined manner regarding supply, the financial risks to those firms and their many stakeholders will start to multiply in 2024.

At some point, this has to show through in the global energy environment at major scale – and in 2024 it probably will. And so, in 2024 we will likely see the transition debate shift from scenario wars to how to optimise and quickly scale the new system.

So, in this month’s Monitor we cover three key areas:

- A high-level analysis of the key questions ahead for climate and energy this year

- A deeper dive into the transport sector – now the largest emitter on the planet

- And a review of how the incumbent oil and gas sector appears to still be misreading this transition, with worsening consequences for its asset investments, and its weight of liabilities, including the high risks to mature phase investors via private equity

Key Climate and Energy questions for 2024

We started the year with a blog covering over 20 key issues we believe will be confronting the climate and energy markets in 2024 – they ranged from the EU and US elections, to the outcome of the COP28 negotiations and to the sudden rise of new energy technologies.

- Will the growth of China’s renewables market finally outstrip the expansion of domestic coal power generation? This would be a big deal: for emissions, clean energy, and for Chinese climate leadership.

This marks one of the most serious changes in the energy transition. As soon as China can bend the emissions curve, generating more clean energy than it emits via fossil fuels, the world emissions curve goes into reverse.

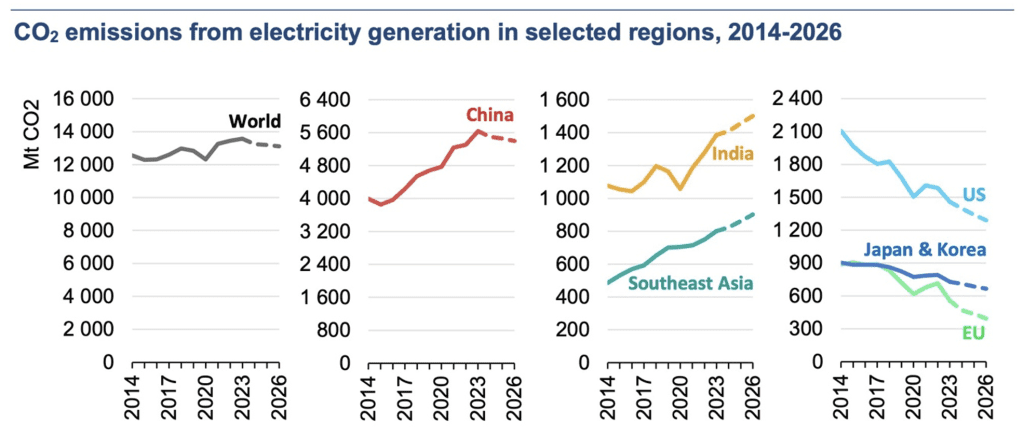

Our analysis aligns with the latest IEA global electricity sector report – which indicates peak emissions in 2023, and a fall of over 2.4% in 2024.

Figure 2: CO2 emissions from electricity generation in selected regions 2014-2026

Source: IEA. Licence: CC BY 4.0

Good news for the global power sector – but it leaves transport as the world’s highest emitting sector – which we also noted as a key question and covered in a transport

- The IEA nailed their colours to the clean energy mast more than ever in 2024. Watch out for what they have to say on EVs and oil demand for road transport.

Our blog UK Electric Vehicle Industry – Battery half full, half empty or running out of charge? delved deep into this by using the UK as an example.

Transport is a major pivot of the energy transition – and the blog sums it up in a key issue:

“The world of automotive manufacturing has been upended for the first time in a century by the introduction of engines that need no oil and are faster and cheaper to run. Resisting this change, and not building a strategy to exploit it is mass-scale industrial folly. The UK needs to rethink its battery strategy as a priority.“

The UK, a major G20 economy, needs to re-appraise its industrial transport policy to retain jobs and offer future growth, as the blog explains.

In a multi-trillion transport market the ability to be part of the global battery supply chain will be fundamental. The chart below shows how this will likely play out between now and 2030.

Figure 3: Global Battery Manufacturing Capacity by 2030 (TWh)

Source: Benchmark Minerals

As we note in the blog, the UK suffered two home-grown battery manufacturing bankruptcies in 2023 (Britishvolt and AMTE) – largely due to pursuing a Venture Capital (VC) driven strategy and novel battery tech route in a world rapidly moving to the mass manufacture of EVs with proven lithium-ion designs.

In 2024, best estimates are there will be another 17 million EVs sold, a market worth over $500bn per year growing at over 20% pa. It is a world now requiring large industrial and manufacturing capacity, at mass scale.

We therefore predict the continued rise of two Chinese manufacturing behemoths: BYD to become the largest manufacturer and exporter of EVs in the world in 2024, and CATL to continue its dominance of EV battery manufacture for global brands.

And now that battery packs power over 50 million EVs on the road, electrification of transport threatens the oil monopoly of road transport – most estimates have the impact on oil demand by 2030 of a net reduction between 4-6 mb/day.

Which leads to our final key question – how does this all impact oil demand?

- What happens with the Rosebank oil field in the North Sea? Will parliamentary and NGO legal pressure stymie the necessary finance needed to take the project forward?

Rosebank is an exemplar of the current style of oil firms’ corporate approach: that is to dig in and continue with the expansion of hydrocarbon fields, despite warnings of demand decline and future emissions increases – even at the high end of the cost curve.

A precise instance of a wasted and upcoming stranded asset – which will add further to the global carbon bubble as we explain below in our blog – How many new emissions did oil and gas exploration add last year? Nobody knows

Here is the problem, that Rosebank and other oil-field developments around the world continue to create.

The remaining carbon budget to have a 50% chance of limiting global heating to 1.5 degrees has dropped beneath 300 billion tons (gigatons) of CO2 equivalent (CO2eq). But we produce from oil and gas alone 25 billion tonnes of CO2e per year. The arithmetic is simple – our remaining carbon budget due to oil and gas emissions alone is 12 years – or 8 years if you include all emissions.

This is why we are calling for a simple global metric, New Reserves and Resources which it aims to work on with the Global Registry of Fossil Fuels, and calls on a global target of Zero New Reserves in the exploration sector – Global Zero New.

The blog reviews the issue in more detail and how it can align with IEA demands for no new developments.

But the reserves problem is a far wider one as we highlight in From Net Zero to New Zero – Reserves Estimates in a Decarbonizing World.

As the report notes, as energy transition advances, a large part of total oil and gas company reserves, not just the recently added ones will become worthless.

In short, we have a system of measuring reserves that was fit for a world focused on discovering and developing new fossil fuels; that system is not fit for a world that must cease adding new reserves and manage a decline in the rate of production of existing reserves.

The report explores the extent of this, its implications for industry governance and company finances, and potential solutions.

Relatedly, in our report: Overlooked: Why oil and gas decommissioning liabilities pose overlooked financial stability risk, we highlight a growing liability bubble with oil and gas firms decommission requirements being far short of full liabilities.

The scale of this problem is massive in financial terms – as the report analyses in detail:

- Oil and gas decommissioning obligations are large. Our first-order estimate to decommission existing oil and gas infrastructure in the U.S. alone exceeds $1.2 trillion. Total costs globally could be four times as large – a total exposure twice the size of the 2008 financial crash.

More study of this topic is urgently required, and the report goes into deep detail on the options for change and the implications for all key stakeholders.

And yet, even higher risks are still being taken.

At the late stage of oil and gas investment, misreading the energy transition paradoxically attracts private equity (PE), who are drawn to contrarian bets, such as assuming there are high returns to be made on betting on a long slow and well-ordered energy transition.

In Private Eyes Wide Shut: Private Equity Investments in Oil and Gas at Risk from Energy Transition we analyse how taking late bets on oil and gas development by private equity firms puts GPs and LPs at increasing risk, as they delve into high cost oil and gas developments for example in the North Sea.

The report:

- Quantifies the impacts of a slow and moderate-paced transition to private equity backed companies’ future cash flows, investments, and production.

- Identifies the key considerations for policymakers and financial regulators.

- Throws a spotlight on private equity backed companies’ role in new licensing.

A webinar on this report in February will provide further details.

To conclude – Carbon in 2024: from valuable commodity to stranded element

An obvious point of the energy transition is that it aims for decarbonisation: meaning carbon will be used less and less in the energy system. As a commodity element, carbon will command less value as demand declines, yet its high-risk supply continues.

Many parties such as investors, fund managers and regulatory bodies should take very careful note of stranding risk across the old fossil system in the new year of the Dragon.