The Covid-19 crisis is showing up the oil and gas industry’s exposure to the threat of falling demand, a forewarning of what will happen through the energy transition. Traditional business models are rapidly falling apart. While companies are waking up to this, with a succession of newly-announced strategies and associated climate “ambitions”, pay policy remains inadequate.

Our recent report, Fanning the Flames[1], reviewed the policies of 30 of the largest listed oil and gas companies, finding that for the vast majority, senior executives are still directly incentivised to grow oil and gas production volumes. This is both at odds with successfully navigating the energy transition, and against shareholders’ interests.

Fanning the Flames (March 2020) – Summary of Key Findings

- Nearly 90% of companies have direct growth metrics such as production or reserves replacement metrics in their 2019 incentive structures, at odds with the value-focused strategies needed through the energy transition.

- Globally, 15% of variable pay is driven by direct volume growth metrics, with a third of variable pay linked to growth including more subtle indirect growth incentives.

- Just four companies have no direct growth metrics: Diamondback Energy, Equinor, OMV and Origin Energy.

- For European majors, nearly half of variable pay incentivises volume growth (direct and indirect metrics).

Overall, we find that most remuneration practices are bad for the climate and bad for investors. With AGM season approaching, we encourage investors to really consider whether current remuneration policies are appropriate, and highlight five questions to ask.

Remuneration and the role of incentives

“It is not from the benevolence of the butcher, the brewer, or the baker, that we expect our dinner, but from their regard to their own interest. We address ourselves not to their humanity but their self love”

Adam Smith, Wealth of Nations.

To understand how individuals might act within a world of limited resources, Economists often appeal to Homo Economicus, a rational human who is able to allocate their time appropriately to maximise the value they receive. That reward can be financial, either in the short or over the long term, or in less directly quantifiable forms such as the feeling of satisfaction in helping others.

For organisations – be they commercial or otherwise – to be successful then they must ensure that individual actions are aligned with their goals. Corporations fundamentally exist to deliver a return (either income now, capital growth, or both) to their shareholders, and variable pay is often used to incentivise employees towards these company objectives. While this can take the form of shares awarded with no strings attached, awards can also be directly linked to performance against key metrics associated with business “success”. It is these specific incentives that are our focus.

To give the market confidence of continued dividends and associated share price appreciation, the oil and gas industry wants to demonstrate a strong pipeline of future commercial[2] projects; the metric of reserves replacement ratio has historically been used to show this. This metric is then used to assess leadership performance and determine variable pay, and directly incentivise growing production. Alongside this, a range of other metrics which also incentivise growth, both directly (e.g. production growth) and indirectly (e.g. absolute levels of free cash flow), feature in remuneration policies.

“You always get more of whatever you measure”

Louis Gerstner, former CEO and Chairman of IBM Corporation.

Perhaps in contrast to those in a charity or volunteering organisation, the subspecies H.E. Corporatorum is likely to display some of the most direct responses to these financial incentives. Those who have made it to the helm of oil and gas companies have had long careers marked by delivering against these personal incentives; they will undoubtedly continue to strive to meet the targets they are set.

Given this rationalism, if incentives are used to influence individual behaviour, then they must be aligned to a corporate strategy fit for the current business environment.

The energy transition: focus on rewarding value creation

While being the CEO that pumps the most crude may give bragging rights in the country club, that’s of little interest to shareholders whose currency is dividends now, or the potential for strong future distributions. Even under stable business conditions, management should be incentivised to create value, rather than growing production simply to get bigger. Against the backdrop of falling demand for fossil fuels through the energy transition – and peak oil may even have been reached in 2019 as a result of the Covid-19 crisis[3] – this need for a value focus is magnified.

For oil and gas companies, we see two broad strategies to maximise value in response to the energy transition: optimise production from existing assets (“harvest”) or seek future cash-flows from non-hydrocarbon businesses (“transition”). Either strategy must then be backed up by appropriate metrics in remuneration policies. Of course, non-fossil investments still need to create value – the rationale of not growing for growth’s sake still applies – albeit counter-arguments around capturing market share are far more relevant in a growth sector such as renewables.

As a value metric example, consider total shareholder return (TSR)[4], in comparison to share price. While variable pay awards linked to share price performance do reward actions valued by the market, they implicitly disincentivise returning capital to shareholders, whereas TSR links directly to the creation of shareholder value via either route, and is strategy-agnostic.

Current remuneration practices hold back change

In Fanning the Flames, we reviewed the remuneration policies of the 30 largest companies listed in Europe, North America and Asia-Pacific. We find that for 2019, just 4 companies (Diamondback Energy, Equinor, OMV, Origin Energy) did not include any metrics which directly incentivised fossil fuel growth. For the remaining 87% of companies, either:

- The company strategy was to continue to grow fossil fuel production and they encouraged management to deliver this, or;

- The company had a stated long-term ambition to transition away from fossil fuels, but their executives were incentivised to do anything but.

Either way, most remuneration practices are bad for the climate and bad for investors.

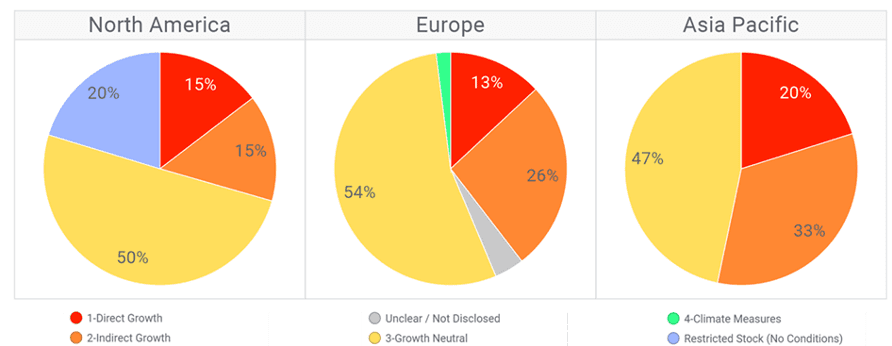

We also quantify the relative impact of different metric types on variable pay (Figure 1), showing that around a third is linked to volume growth incentives (direct and indirect). While European companies are generally positioned ahead of their North American peers in terms of climate ambitions, for them we see just 1% impacted by climate measures (e.g. decarbonisation or renewables investment).

Figure 1. Variable target CEO remuneration by incentive – average by company within region

Source: Company reports, CTI analysis

Note: Where incentives include an unweighted basket of metrics, the entire basket is assumed to be subject to any included growth metrics. Pie-charts are equally-weighted by company to avoid skewing results to companies with higher total remuneration. 2018 performance year.

While Figure 1 may indicate the average North America-based company as having a lower proportion of variable pay incentivising volume growth, a fifth is paid as restricted stock without any performance conditions (therefore delivering a reward to executives even if TSR is worse than peers or significantly negative). Furthermore, many US companies still include options, inherently encouraging risk taking through limited downside exposure.

Over the last few years, we have generally only seen incremental progress in remuneration practices, and these continue to lag corporate positioning. For example, despite their ambitions to be a “Net Zero Emissions Energy Company”, Shell’s 2020 remuneration policy retains measures which directly reward growing oil and gas production, contributing to 25% of annual bonuses[5].

More positively, for 2020 BP appears to have removed its remaining direct growth metrics to accompany its “Net Zero 2050” announcement, although the indirect growth metric of free cash flow remains within its annual bonus. Repsol, which despite having one of the most progressive climate ambitions[6] still had a reserves replacement metric in its long-term remuneration plan in 2019, has now shaken up its remuneration policy for 2020. A significant proportion is now linked to decarbonisation and sustainability (25% of annual bonus and 40% of long-term award), however both awards are linked to a new strategic plan, for which individual metrics are not yet disclosed.

Use your vote accordingly

Even for those companies that have no plans to change course in response to the energy transition, remuneration should incentivise “value over volume”. For those looking to transition, companies’ stated strategies may paint a bold picture 30 years hence, however if senior leaders are rewarded for continuing to grow hydrocarbon production, then that’s what will be pursued. As individuals it would be irrational for them to act differently, particularly given their relatively short tenure. This will make responding to the energy transition their successors’ problem, with shareholders the ones to lose out in the interim.

With AGM season approaching, we encourage investors to really consider whether company strategies are all they seem, and particularly whether current remuneration policies are appropriate – we highlight five questions to ask.

Five key questions for investors to ask on executive remuneration:

- To what extent does remuneration policy really align with stated corporate strategy, particularly on risks related to stranding assets in the energy transition?

- Are there any metrics which directly incentivise growth in oil and gas production without a value element? In particular:

- Reserves replacement

- Production volumes

- Exploration resources

- Are there other metrics which indirectly create an incentive to increase oil and gas volume growth, for example absolute levels of earnings or cash flow?

- Are climate-related measures really meaningful in the context of the absolute emissions reductions required to meet the goals of the Paris Agreement?

- Are the relative weightings for individual metrics disclosed and if not, why not?

[1] Available at https://carbontracker.org/reports/fanning-the-flames/

[2] Reserves are by definition supposed to be commercial, however the commodity price assumptions used are not necessarily consistent with under different international development scenarios, or worse, inconsistent with companies’ own price forecasts.

[3] Carbon Tracker report “Covid-19 and the energy transition: crisis as midwife to the new” available at https://carbontracker.org/covid-19-and-the-energy-transition/

[4] Used by some companies as both an absolute metric and relative to peers.

[5] Share Action report “Shell’s and BP’s 2020 remuneration policies”: https://shareaction.org/wp-content/uploads/2020/04/BP-Shell-Rem-Final.pdf

[6] “Repsol’s net zero ambition: joining the dots” available at https://carbontracker.org/repsols-net-zero-ambition-joining-the-dots/