Suggested reforms offer best chance to deliver GB net zero power market by 2035

LONDON, February 01 – British customers overpaid on their power bills to the tune of £7bn in 2021-22 finds a study published on Tuesday in response to a consultation on reforming the power market. The analysis suggests policy measures such as utility hedging obligations for future fuel needs to reduce exposure to high gas prices, and reform to contracts for difference (CfD) agreements to lower bills.

Marginal Call estimates what Great Britain’s wholesale market electricity costs would have been if prices were calculated via a “split market” that separates the pricing of power produced by variable supply of renewables, from other sources, as opposed to the marginal pricing design the market currently operates under.

This allows for a measure of prices that are more reflective of the operating costs of technologies supplying electricity and an estimate as to the extent to which global gas market influence can skew UK electricity prices under current market design.

When calculated this way, total net power procurement expenditure over 2021-22 turns out around £7.2 billion lower, representing what could have been saved if measures had been in place to protect against gas market price spike influence on the power market. This is netted against past and projected payments made between renewable generators and the CfD support scheme for low-carbon generators over the period.

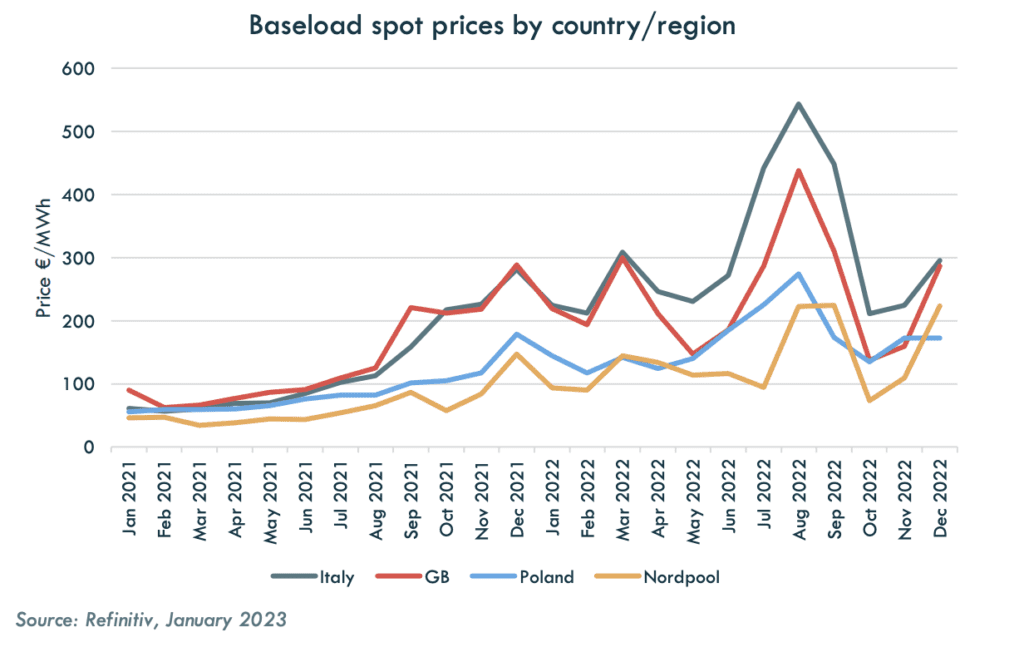

The report finds Europe’s most gas power dependent countries, the UK and Italy consistently paid the highest spot prices during the recent period of high gas price volatility (fig 1). With gas-fired power stations the marginal source of UK power generation for several years, power prices effectively mirror movement seen at the UK’s NBP gas hub, leaving consumers exposed to paying the highest prices ever for electricity during a gas-led energy supply crisis.

Figure 1: Power prices in gas-dependent nations have detached from those less exposed

Senior Analyst and report author Jonathan Sims said:

“Our findings show the extent to which the global gas market has over the past two years skewed British power prices to levels unreflective of the technological makeup of today’s generation mix.

“While continuing with marginal pricing for wholesale power market design is preferable to ensure significant changes do not dent investor confidence in the renewables sector at this crucial juncture, government must protect against any future gas price spikes pulling power market prices up with them.”

The study stops short of calling for a market split to be rolled out as Great Britain’s long-term power market design option, as a significant shift in design now could threaten power market net zero by 2035 goals, by introducing uncertainty over revenues of new renewable power generating technologies required to wean the market from gas power, which continued to account for close to 40% of the country’s electricity generation in 2022.[1]

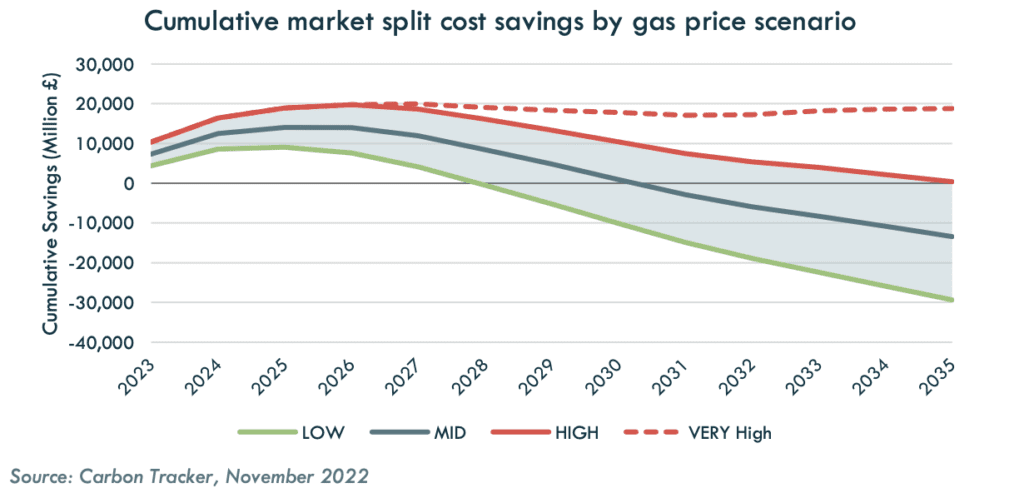

Market split design would also only result in cheaper bills for consumers if gas prices remain at existing high levels for the rest of the decade (fig 2), while pricing signals for flexible power sources such as battery storage would be weakened.

Figure 2: Gas prices would need to remain high for market split design to achieve long-term cumulative cost savings

Instead, Carbon Tracker recommends retaining the marginal price system but introducing measures, such as utility hedging obligations, which could protect against future gas market price spikes skewing power market prices under this design. The National Audit Office (NAO) cites “insufficient hedging” as a significant factor in 71% of UK energy supplier insolvencies reviewed between July 2021 and May 2022[2].

Reforming CfD agreements for clean technologies, by removing existing loopholes that allow producers to delay the onset agreements, driving up power costs for consumers, is also recommended. The suggested market reform approach would deliver benefits in terms of reduced consumer vulnerability to volatile gas prices as the GB power market decarbonises, without the major disruption and high upfront policy reform costs associated with migrating to an alternative design.

Power Analyst and report author Lorenzo Sani said:

“A split market, by effectively putting a floor on wholesale prices, removes the price signals needed to deploy the flexible technologies that can ensure the stability of a renewable-based power system. A net-zero power market must provide incentives for the clean technologies that are currently struggling to be profitable: flexibility providers (e.g. battery storage and demand response) will support system stability while electrolysers would take advantage of the low-price periods to produce green hydrogen to be used during cold winter days.”

Carbon Tracker’s longer-term view is for gas demand to peak and prices to decline as lower-cost renewables gain market share – suggesting that a move to a split price market today may not recover sunk market reform costs, or reduce bills for consumers tomorrow.

Alternative market redesign structures considered by the analysis include locational pricing (both zonal and nodal pricing) – but limitations are highlighted for such approaches including concerns that these could result in a more fragmented market, reducing trading liquidity and the ability to hedge against forward price movements.

Therefore, retention of the current marginal price structure, together with reform of CfD agreements represents the lowest cost/ lowest risk policy option – providing cost relief for UK consumers, and policy certainty for investors financing the transition from gas to renewables.

Background:

In July 2022, the UK Government opened a consultation[3] Review of Electricity Market Arrangements (REMA) seeking expert views on reforming the power market to lower costs and maximise the potential for energy security offered by domestic, low-carbon energy sources. This analysis furthers that consultative by modelling the consumer price feedthrough implications of wholesale energy prices on the various market redesign options.

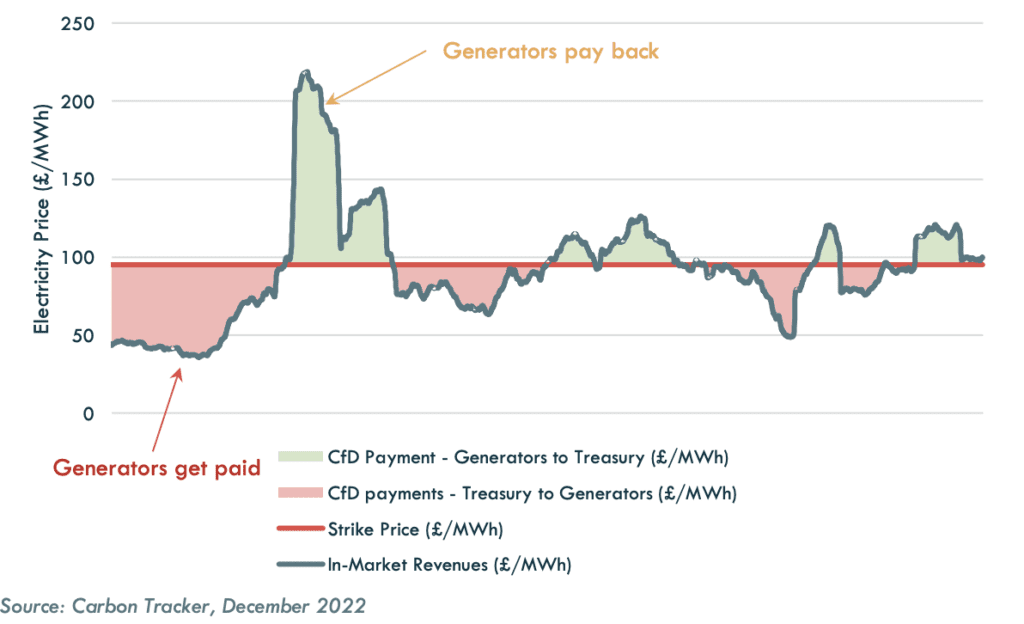

About Contracts for Difference[4]

CfDs are currently the main support mechanism for renewable energy in the UK; they are a price discovery system which determines a strike price through reverse auctions. Generators who win a CfD are compensated the difference per MWh to the market price, but if the market price goes higher than the strike price, generators must pay back the difference. The contract provides long term certainty in revenue streams for investors, while the subsidy cost to consumers is kept within strict limits. The auction mechanism works as follows: the government sets a technology-specific target of capacity and budget. Renewable generators that meet the eligibility requirements can apply for a CfD by submitting a ‘sealed bid’. The strike price is then determined by the maximum price that exhausts the set budget or the capacity limit. Projects that are competitive with the strike price win the CfD.

Figure 3: Cfd mechanism explained

Once embargo lifts report can be downloaded here: https://carbontracker.org/reports/marginal-call/

To arrange interviews please contact:

Joel Benjamin jbenjamin@carbontracker.org +44 7429 637423

David Mason david.mason@greenhouse.agency +44 7799 072320

About Carbon Tracker

The Carbon Tracker Initiative is a not-for-profit financial think tank that seeks to promote a climate-secure global energy market by aligning capital markets with climate reality. Our research to date on the carbon bubble, unburnable carbon and stranded assets has begun a new debate on how to align the financial system with the energy transition to a low carbon future. www.carbontracker.org