Political pressure may be forcing the IEA to revive an old forecast of endless fossil fuel growth, but oil and gas investment reality tells a clearer story of an industry embracing decline.

The recent threat by US Energy Secretary Chris Wright to defund the International Energy Agency (IEA) has achieved its goal: the return of the pro fossil-fuel “Current Policies Scenario” (CPS) to the agency’s flagship reports. (WEO, Nov 12)

For critics of peak demand and the energy transition, this is seen as a victory for data over ideology. In reality, it is the reverse – it is a triumph of political gesture over foresight.

The CPS – which assumes no new climate policies at least until 2050 – is a backward-looking relic that ignores the seismic shifts already reconfiguring the global energy system.

This marks a fundamental shift in the landscape of energy governance: the IEA has reintroduced a scenario it admits is more pessimistic than real-world trends.

The CPS is therefore a warning, not a forecast: it implies energy innovation stops in 2030, as if hitting some sort of intellectual brick wall.

The ensuing headlines declaring the “collapse of the peak oil demand myth” are a profound misreading of the situation. They confuse a political concession with empirical reality.

A clear-eyed analysis reveals an oil and gas industry already conducting a quiet, rational, strategic retreat from long-term growth, despite public bravado from its supporters in the stands.

The cold data shows a sector preparing for plateau and decline, rewarding investors who push for harvesting with dividends and buy-backs, and leaving investors who believe the growth rhetoric dangerously exposed.

The “say vs. do” chasm

The most telling indicator isn’t found in any resurrected scenario model, but in real-time company boardrooms and capital allocation plans.

That political rhetoric of robust future fossil demand is contradicted by four industry actions:

- Capex rationalisation for a plateauing world. Since the investment super-cycle peak of 2014-2015, global upstream oil and gas capital discipline has been the dominant theme. While 2024 investment is up from the lows of the pandemic, it has stabilised at a level roughly 40% below the peak – falling from nearly US$900bn a year to a steady US$550-600bn per annum (Figure 1 bars).

This new equilibrium is the key signal. The industry has rationally concluded that this leaner, more efficient level of investment is sufficient to meet slowing demand and maintain a production plateau. It is not a signal of growth, but of sufficiency.

This disciplined capex frees up a massive cash flow stream, which is being used not to expand the resource base, but to appease shareholders through dividends and buy-backs – the classic behaviour of a mature, cash-cow industry, not a growth one.

To achieve the aggressive production growth assumed in the exhumed CPS, annual capex would need to surge by US$200-300bn each year, or 30-40% over today’s figures.

The industry’s steadfast refusal to do so is a powerful vote of no confidence in that endless-growth CPS forecast.

Figure 1: Global upstream liquids production by breakeven and capex, compared with IEA’s CPS demand outlook.

Source: Rystad Energy, IEA, Carbon Tracker analysis

Notes: Lines (left-hand axis, million barrels/day) indicate production split by producing and non-producing assets, with non-producing assets ordered by increasing breakeven price. Approximate CPS demand in red (based on linear trend to 114Mb/d in 2050); Bars (right-hand axis, billions of dollars) indicate actual and forecast capex (black tips denote exploration).

- Exploration’s end.Global exploration spending has fallen by around 60% over the past decade, with most majors allocating less than 10% of upstream budgets to new exploration. Exploration, production and construction teams are therefore being cut significantly.[1] BP’s large find in Brazil may seem an exception – but it proves the rule: these step-out projects will take 10-15 years to reach first oil and are more ornamental than truly productive and profitable options, given a 2040-and beyond world unlikely to need them.

- The downgrade signal.Credit rating agencies are listening to the numbers, not the speeches. S&P and Fitch have downgraded the sector outlook, with specific corporate downgrades following new project sanctions. Woodside’s recent negative outlook revision, triggered by a single long-term, high-cost, LNG investment, is a canonical example. The market increasingly treats major new greenfield fossil fuel projects as potentially stranded from the day they are announced.

- The rise of consolidation. the fast uptick in industry merger and acquisition activity (Exxon-Pioneer, Chevron-Hess etc.) also indicates a sector where many under-performing assets are not stranded directly but indirectly via absorption by more powerful corporate operators. This is not production growth; it is financial engineering – shuffling existing assets to cut costs and maintain dividends, and certainly not to expand a resource base, which the industry instinctively knows is not needed.

This rational harvest strategy, however, is not being executed perfectly. A seeming contradiction emerges: while the sector-wide trend is disciplined capex and consolidation, some companies continue to sanction individual, high-cost, long-cycle projects (see Paris Maligned 3, for recent examples).

These are the exceptions that prove the rationalisation rule – and they are increasingly punished by the market. Credit agencies downgrade them,[2] and many investors treat them as instantly stranded assets.

This highlights a critical divergence: the industry’s instinct is to harvest, but legacy structures and political pressure still lead to capital misallocation at the margins – a key risk for investors to resist.

Why is the oil and gas industry behaving this way? The demand foundation is cracking

The freshly-unearthed IEA CPS scenario assumes infinite demand elasticity – i.e. that oil demand will continue forever if the price is right.

But on the ground, the pillars of oil demand growth are crumbling in real-time, and irrespective of price – something frontline oil industry instinctively knows and can see.

- The end of transport growth. Global gasoline demand is set to peak in 2025. The reason is electrification. China, now a dominant “electrostate” is exporting cheap EVs and renewable tech globally, irrevocably altering the oil-intensity of transport. This isn’t a future prediction; it’s a present-day reality as EVs are on track to displace 4-5 million barrels per day of demand by 2030. Perhaps ironically, the IEA’s own detailed chart from earlier this year indicates peak gasoline in 2025, confirming oil-to-electricity substitution.[3]

- China’s dual peak. China’s own oil demand growth is declining. Simultaneously, its power sector emissions are widely expected to have peaked as renewables push coal’s share of generation to below 50% – a stunningly fast transition that undermines the core assumption of endless Asian fossil-demand growth.

- Limited growth levers. The industry clings to petrochemicals and aviation and, most recently, LNG as future growth drivers. Yet, as our analyses – The Future is Not in Plastics, Petrochemical Imbalance, Awaiting Take-Off – have detailed, these sectors cannot possibly offset the sweeping declines in road transport and power generation. They are a fleeting respite, not a revolution. As for LNG, the industry has already committed excessive capital in its dash to go global on gas. Further expansion not only risks new capital but will sacrifice the cashflows of sanctioned projects that depend on sustained prices to meet hurdle rate returns.[4]

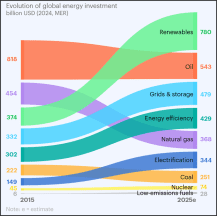

- Capital flight to the new system. The most damning indictment of the CPS is capital flow. While oil and gas capex stagnates, annual investment in renewables, grids, and electrification, at over US$2.2 trillion per annum, is more than double fossil-fuel supply investment. The market is already building the post-oil energy system, recognising that fossil fuels, while important, are a diminishing part of a very new and different, larger energy mix.

The investor imperative: recognise the quiet exit – the “myth of peak oil” is itself a myth

For investors, this creates a critical disconnect.

This “quiet exit” by the industry implicitly recognises the very transition that industry supporters attempt to dismiss.

A focus on peak oil as a “fever dream”, or “an analytical error” may seem satisfying to the incumbent supporters, but it misses the nuts-and-bolts cash numbers deployed by the oil and gas corporations themselves – numbers that acknowledge a far wider energy transition underway.

As Figure 1 shows, the oil industry is investing a steady, rational US$500 -600bn capex annually to maintain a production plateau – and preparing for further reductions as demand falls. The groundwork for increased dividends and buy-backs has already been set, as physical-engineering capex decline creates a financial payout opportunity.

And as fossil-fuel supporters ask for “drill, baby, drill” and try to limit oil decline by clinging to low-probability scenarios, they miss the revolution of the new infrastructure of energy being built around them.

The debate over ‘peak oil’ is a distraction, akin to fighting a last war. The real energy story is one of capital re-allocation, as illustrated in Figure 2.

The new energy ecosystem – encompassing renewables, grids, storage, solar and wind technologies, and EVs – is seeing financial investment double that of fossil fuels, but in energy-produced terms the ratio is closer to 3:1. Much of this is now increasingly developed in China and South-East Asia for deployment in the global South.

This leads to low-cost energy deployment in the global West and North – hence the tariff wars of the past year to try and slow the new energy distribution.

Figure 2: Evolution of changing energy investment from the old to the new system.

Source: IEA Energy Snapshot[5]

The energy transition is therefore not one of adding renewables atop today’s fossil fuels: it is building a whole new energy system that substitutes them with a better, cheaper and more resilient global energy technology.

As the renewable investments grow, the fossil-fuel funding recedes, opening up a new energy chapter globally.

Immediate implications

- For debt markets: fixed-income investors face asymmetric risk – limited upside with full exposure to a structural demand and price downturn. A bond yielding 2-3% over US Treasuries for example, typical of long-dated bonds issued by oil majors is a very poor investment if demand erosion triggers cash-flow collapse and downgrades.

- For equity markets: the question is one of opportunity cost. Why fund the managed decline of legacy incumbents when capital could be deployed into the explosive growth of the electro-tech ecosystem – from grid infrastructure to storage and renewables manufacturing of solar panels, wind turbines and EVs, a sector outspending fossils 3-to-1. The ‘fear of missing out (FOMO) should be moving equity capital to the energy transition, not to the last gasp of the old system.

- For late investors in fossil fuel infrastructure: there are hold-outs in the fossil fuel industry, most notably US LNG – yet these are high-risk and high-cost gambles. Many of the newly minted projects are likely to be stranded from the moment of conception, as a supply glut meets demand destruction in the late 2020s just when they are due on-stream.

Conclusion: look beyond political theatre – the real industry is leaving the battlefield

The reinstatement of the CPS is a political footnote, not an analytical breakthrough. It models a world that is already ceasing to exist – one of static technology hoping for permanent fossil-fuel dominance, with no viable analytical foundation.

The real story is found in the convergence of data: stagnating capex, wary credit agencies, peak gasoline, and peak Chinese emissions. These are not aspirational data points; they are empirical facts around us today, documenting a large energy system in transition, – constructed around the CPS’s static forecasts.

The oil industry’s quiet retreat is perhaps its most rational act in a decade. And the great irrationality now lies with investors who mistake this harvest for a rebirth, and with policymakers who resuscitate outdated forecasts. The industry is no longer led by multi-billion, high-risk engineering mega-projects, but by sober capex reduction, and cash-flow diverted into investors’ pockets: in Q2 2025, Exxon had a free cash flow of US$5.4 billion and shareholder distributions of US$9.2billion, a US$-3.8bn deficit in just 3 months, clearly showing their priorities, even amid a pro-fossil fuel vibe across the political landscape.[6]

Investors and fossil fuel supporters who believe the resurrection of the CPS is a pivot toward energy reality, should see it as the very opposite: a shift into magical thinking, a very dangerous move in a hard, engineered, unblinking realm of fossil fuel production where the capex retreat shows the oil industry knows when to quietly exit the battlefield.

—————————————————–

[1] Cost cutting is rife in upstream oil and gas, including job cuts in exploration: https://www.reuters.com/business/energy/global-oil-gas-company-layoffs-2024-2025-2025-09-30/

[2] https://energynews.oedigital.com/lng/2025/05/01/sp-downgrades-woodsides-credit-rating-to-negative-after-lng-investment-decision

[3] https://www.iea.org/reports/global-ev-outlook-2025/outlook-for-energy-demand?utm

[4] https://www.ft.com/content/5ba8caec-61d3-4aa9-a877-9b200ef4b5b0

[5] https://www.iea.org/newsletters/energy-snapshot/23-06-2025/how-has-energy-investment-changed-over-the-past-decade

[6] https://corporate.exxonmobil.com/news/news-releases/2025/0801_exxonmobil-announces-second-quarter-2025-resultsn