Key Resources

Press Release

Oil industry betting future on shaky plastics as world battles waste

Read MoreInfographic

The Future’s Not in Plastics

Download ResourceRelated Webinar

Climate Week NYC 2020 Webinar | The Future’s Not in Plastics, Benjamin

Read MoreKey Quotes

The oil and petrochemical industries are betting their future growth prospects on demand for plastics.

But plastics demand is likely to peak as the world starts to transition from a linear plastic system to a more circular economy and governments act to hit climate targets. The implication is peak oil demand and hundreds of billions of dollars of stranded petrochemical capital expenditure.

Forecasts from BP and the IEA both see petrochemicals as the largest driver of expected oil demand, making up 95% and 45% respectively.

Plastics are uniquely vulnerable

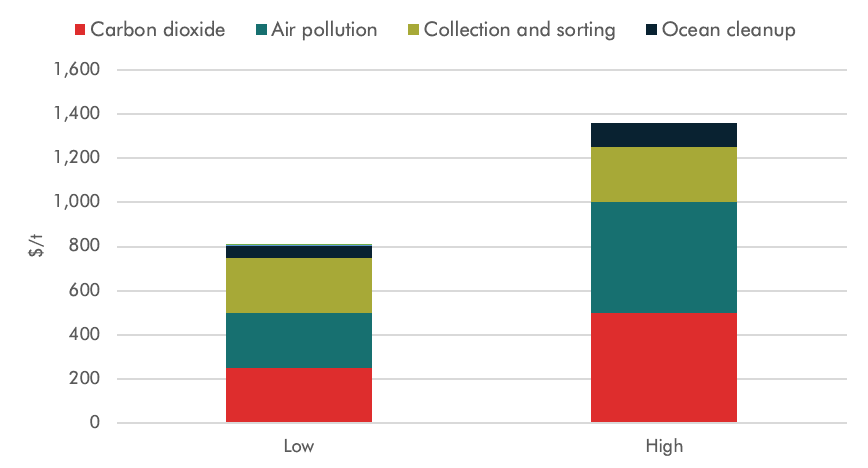

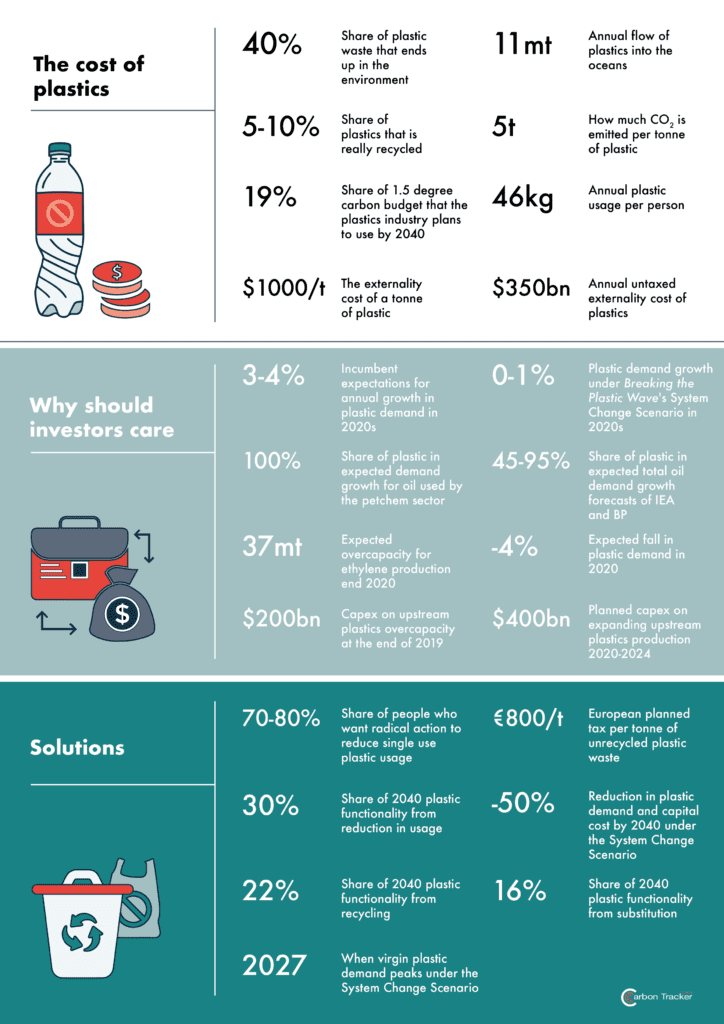

Plastics impose a massive untaxed externality upon society which this report estimates is about $1,000 per tonne ($350bn a year) from carbon dioxide, health costs, collection costs, and ocean pollution.

Range of plastic externalities per tonne ($)

Source: EPA, CREA, WHO, UNEP, CT estimates, Breaking the Plastic Wave

There are technology solutions

There are three main solutions – reduce demand through better design and regulation; substitute with other products such as paper; and massively increase recycling.

Why now?

Policymakers in Europe and China are implementing much more stringent regulatory regimes using the five key tools of taxation, design rules, bans, targets, and infrastructure.

Moreover, the COVID shock is likely to reduce plastic demand by around 4% this year and give policymakers more room to act.

Stranded petrochemical assets

There is a stark contrast between the plans of the petrochemical industry and the threat of much lower growth.

The petrochemical industry already faces huge overcapacity but is planning to spend a further $400bn on 80 mt of new capacity. Unless stopped, this will result in continued low prices and stranded assets.

Plastics: Key Statistics

Watch our webinar at Climate Week NYC 2020 to hear from the report author and the expert discussion.