We welcome the recent announcement that South Africa has struck a deal to access concessional financing of $8.5bn over the next five years from US, UK, France, Germany and the EU.

Nevertheless, we see this as only the first step, given South Africa will need significantly more financing to fully close its coal plants and transition to clean energy. In fact, Eskom’s CEO has publicly stated recently that closing coal plants and switching to renewables would cost $30-35bn over 15 years .

South Africa is the world’s 12th biggest emitter of carbon dioxide and is the sixth largest in terms of installed coal capacity. It has 42 GW of coal capacity and around 85% of electricity is derived from coal power. Eskom, the heavily indebted state monopoly power utility, announced in August the planned retirement of up to 30% of its coal fleet (12 GW) by 2031.

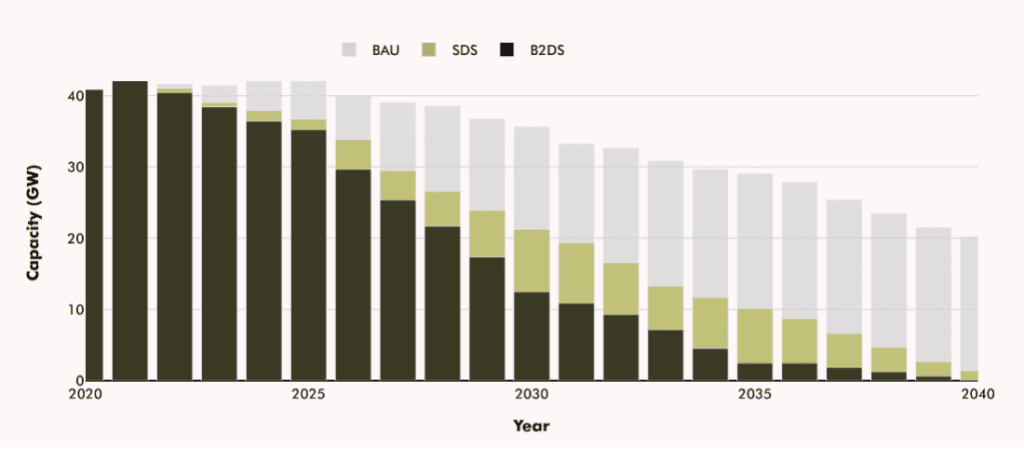

We leverage the data from our proprietary global coal power economics model (GCPEM), which contains detailed country coal modelling at the boiler-level, to determine a coal phase out pathway for South Africa. Our analysis shows that under a Beyond Two Degrees Scenario (B2DS)[1] South Africa will need to shutter 30 GW of coal capacity by 2030, with much of the remaining capacity (10 GW) needing to be decommissioned by 2035. By 2040, all coal plants in South Africa would need to be closed according to our research.

Figure 1 Coal phase out pathway for South Africa under B2DS

Source: Carbon Tracker Analysis

As our analysis highlights, Eskom’s current medium-term plan falls well short of the capacity needed to be closed under B2DS, which would limit temperature rises to close to 1.5°C. This is compounded by the fact that Eskom continues to build new coal plants. According to Global Energy Monitor, South Africa has over 3 GW of new coal plants under construction and a further 1.8 GW in the pre-permit phase. As the IEA has highlighted, no new coal plants are needed if we are to keep temperatures to within 1.5°C warming. Moreover, our analysis shows that Eskom is at risk of $5.3bn of stranding[2] of its existing coal power assets.

Many of Eskom’s coal plants are old – we estimate the average age to be 41 years – and unreliable, meaning consumers are regularly confronted with rolling blackouts. Furthermore, we estimate almost 90% of the power plants in operation use sub-critical boiler technology, which renders them less efficient and more polluting than newer plants which utilise supercritical or ultra-supercritical technology. Indeed, connected to this issue, the CEO of Eskom stated in March that it would cost more than R300bn (almost $20bn) to retrofit its coal fleet to comply with current emissions standards. The rejection by South Africa’s environment department to delay compliance with emission limits could see 16 GW of Eskom’s coal capacity close immediately.

It makes no financial sense to spend vast sums of money retrofitting a polluting technology, when South Africa has abundant and cheap renewables potential. The economics of building new solar farms is overwhelming, with solar already cheaper than operating existing coal plants.

We calculate the cost of building new solar farms in South Africa in 2022 to be $41/MWh (levelised cost of energy) which is below the cost of operating existing coal plants at $46/MWh (long run marginal cost).

We forecast solar costs to continue to decline reaching $36/MWh by 2025 and to be well below the $55/MWh cost of running existing coal plants at that date. Including battery storage with solar will see renewables outcompete operating coal by 2026 with a cost of $52/MWh.

South Africa and Eskom should be more ambitious in decommissioning the coal fleet and transitioning to solar power The initial financial commitment of $8.5bn is not in itself sufficient to fund all of South Africa’s renewable transition, but it is a major step forward and may lead to additional financing in the future.

Using the new financing to kick start the retirement of old coal plants, in-line with our phase-out analysis, and replacing them with new renewables will enable South Africa to get on track to meet its climate goals, ensure a better financial and environmental outcome for energy consumers and lay the foundations for sustainable job creation. Progress should be closely monitored as success may provide a template to phase out coal and transition to renewables for other coal-dependent countries, such as those in South East Asia.

[1] For an explanation of what our B2DS modelling involves, please refer to p.18 and the coal methodology in the appendix of our recent Do Not Revive Coal report

[2] We calculate stranding risk for operating coal units as the difference in the net present value of operating profits (annual revenues less long run marginal costs) between a scenario of Business as Usual (BAU) and a Beyond 2 Degree Scenario (B2DS). For a more detailed explanation, please refer to p.31 and the coal methodology in the appendix of our recent Do Not Revive Coal report