New report offers framework to prevent well liabilities being transferred to taxpayers as oil well production declines and plugging costs mount

LONDON, 10 June – Policymakers across the U.S. increasingly acknowledge the scale and cost of orphaned and abandoned oil wells. But while the problem is well-known, the solutions remain highly contested.

The report, Solving the Oilfield Paradox explores why a profitable industry is still offloading millions, and is poised to offload billions in clean-up liabilities onto the public. It provides a framework for addressing the dual challenge of legacy wells and flawed incentives, offering systemic solutions that balance the need for new well plugging funds, with the risk of creating amoral hazard – where taxpayers cover the liabilities of oil companies that have profited for decades.

The “oilfield paradox” refers to the growing disconnect within industry, where some companies have created and profited from oil wells, walking away before the clean-up bill comes due, while others, who now own the wells, often lack the financial capacity – or the incentive – to clean up, transferring the risk to states, communities and ultimately taxpayers.

Since about 1970, well plugging in the U.S. has been universally established as a condition of receiving and operating a permit for a well.

However, this obligation has been undermined by three policy failures:

(1) insufficient financial assurance requirements, which should create a financial incentive to plug the wells,

(2) permission to freely transfer wells, including to operators that may prefer defaulting on plugging obligations to paying the cost, and

(3) lax enforcement by oil and gas regulators and the lack of a mechanism to ensure that the oil and gas industry, rather than taxpayers, is in position to settle these liabilities when operators default.

These issues resulted in the massive number (approx 2.3 million) of unplugged wells today. Addressing them could cost around $280 billion, requiring a systematic approach

Rob Schuwerk, report author with Redwater Insights, said:

“Good policy is about proper incentives, and currently, in most jurisdictions, the incentives are to defer and offload AROs rather than settle them as the law requires. The legacy of poor policy choices has allowed many wells to remain unplugged, long after their economic lives have come to an end. Policy makers will have to act to prevent these liabilities from being offloaded to the public. Our framework is designed to help policymakers fix the system and restore accountability in the sector”

‘Financial assurance’ – whether in the form of surety bonds, letters of credit, cash and cash equivalents, or sinking funds is intended to protect the public from paying to plug wells by incentivizing operators to do the work.

However, unlike commercial creditors, U.S. states and the federal government have not required financial assurance commensurate to the risk—‘Billion Dollar Orphans’ (2020) found that, on average by state, only approximately 1-2% of estimated plugging liabilities are covered by financial assurance.

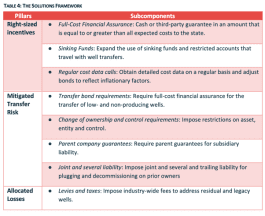

Our recommended Policy Solutions Framework has three policy pillars:

- Right-size financial incentives: Operators must be forced to internalize the costs of plugging wells; the primary mechanism for this is financial assurance which should be equal to or greater than the expected costs of plugging. Sinking funds should be considered.

- Mitigate transferred liability risk: Allowing well transfers without increases in financial assurance forces the state to absorb more counterparty credit risk, for free. Transfers need not be prohibited, but the state should not bear added risk.

- Allocate losses: Where subsidization is necessary to meet requirements, money should come from industry as the primary beneficiary of drilling activity, rather than the public.

Each pillar requires both the political will and infrastructure to support enforcement activity (refer Table 4 subcomponents below).

In a previous report: ‘There Will Be Blood’ (2023) we compared expected future cash flows from California’s oil production to AROs for all existing wells, in aggregate – finding even if the entirety of industry’s free cash flow were retained to pay for plugging it would fall short of the estimated $21.5 billion in liability by a whopping $15.2 billion dollars.

In ‘Rocky Mountain Highs and Lows’ (2024) we assessed the future cash flows from and the expected costs of plugging the roughly 48,000 unplugged wells in Colorado, where production peaked 5 years ago, concluding that approximately 27,000 wells sat in well-type groups that would be unable to pay for their plugging. By contrast, the cash flows from roughly 11,000 Denver-Julesberg horizontal wells would likely be more than sufficient to pay for the plugging of all wells in the state.

Once the embargo lifts the report can be downloaded here: https://carbontracker.org/reports/solving-the-oil-field-paradox/

For more information and to arrange interviews please contact:

Joel Benjamin jbenjamin@carbontracker.org +44 7429637423