Key Resources

Summary Report

Press release

The great coal cap: China’s energy policies and the financial implications for thermal coal press release

Read MoreKey Quotes

Since the turn of the century, China has almost single-handedly been driving global thermal coal consumption growth. Changes in the regulatory landscape and the competitiveness of different power sources suggest that future demand may not follow the same path. This could have significant financial implications for investors, regulators and civil society that do not foresee such changes.

- What are the drivers leading many to predict the near-team peaking of China’s thermal coal demand?

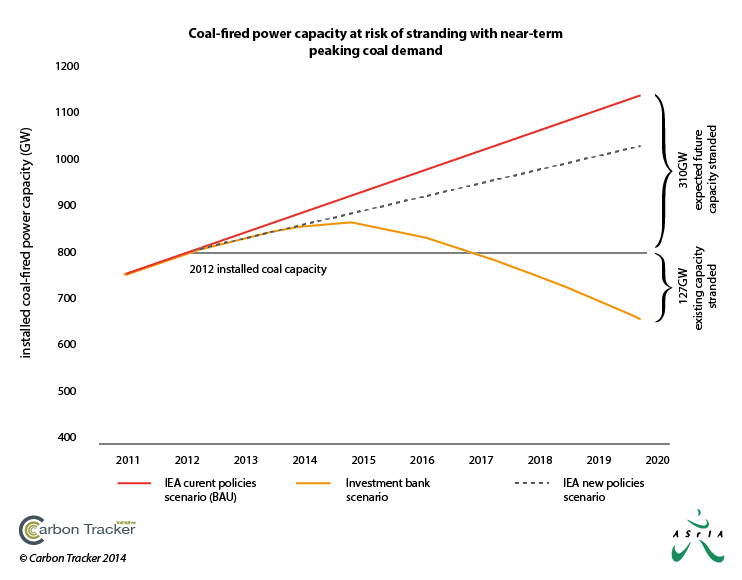

- What is the scale of thermal coal reserves, potential reserves and power generation infrastructure at risk of becoming stranded in this scenario?

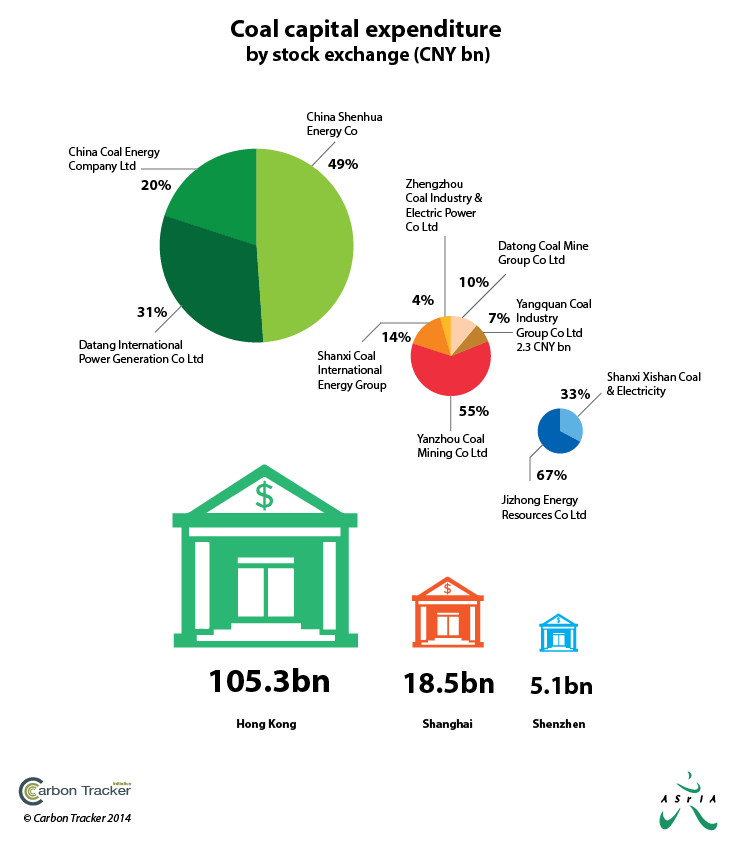

- How much capital expenditure is being committed by China’s coal sector to add to potentially strandable coal assets?

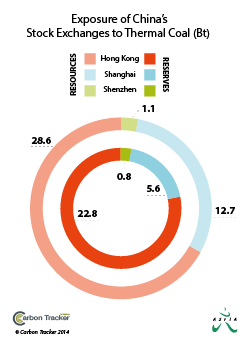

- How does this translate to investor exposure to this risk through China’s stock exchanges?

- Who is most exposed to this risk?

- What implications does this have for the international thermal coal market?

- What actions can be taken by investors and other stakeholders to minimise their exposure to potential stranded assets and, instead, take advantage of China’s transition to a more diverse power generation sector?

Key Findings

This report from Carbon Tracker and ASrIA (the Association for Sustainable and Responsible Investment in Asia) evaluates the environmental and economic regulatory drivers serving to slow China’s coal demand growth to a potential peak.

The research goes on to reveal that this lower-than-expected Chinese coal demand could create significant stranded assets and wasted capital both for those within China’s coal sector and international coal exporters.

The report was launched in Hong Kong on June 5th. To download the Chinese version of the report click here.

Partnering with us on the report are Simon Zadek, Co-Director, Inquiry into the Design of a Sustainable Financial System, and ASrIA.

Click images for larger version