Key Resources

Press Release

US oil majors unprepared for existential challenge of energy transition

Read MoreKey Quotes

In a series of reports since 2011, Carbon Tracker has shown the financial and stranded asset risks to fossil fuel producers related to the shift to a lower carbon economy, in a world where stabilising global temperatures to any level puts a finite limit on the amount of CO2 that we can emit (“the carbon budget”).

Carbon Tracker has looked at the risk of investing in “stranded assets” – projects that fail to deliver adequate returns as conditions change.

In this report, we look at potential capital expenditure (“capex”) that might be spent on such stranded assets in the oil and gas industry using an economic framework, and focus on company and project level results. This report updates previous work on this theme, Carbon Tracker’s 2 Degrees of Separation series, including 2019’s Breaking the Habit.

The energy transition to a net zero carbon world is an existential challenge for oil and gas majors but US companies are lagging way behind their European rivals in adapting their businesses and minimising their stranded asset risk.

Key Findings

Far from simply an “ESG” issue (environmental, social and governance), for fossil fuel producers the energy transition represents an existential concern that goes right to the heart of strategy. It therefore requires an integrated approach that touches on different aspects of the business.

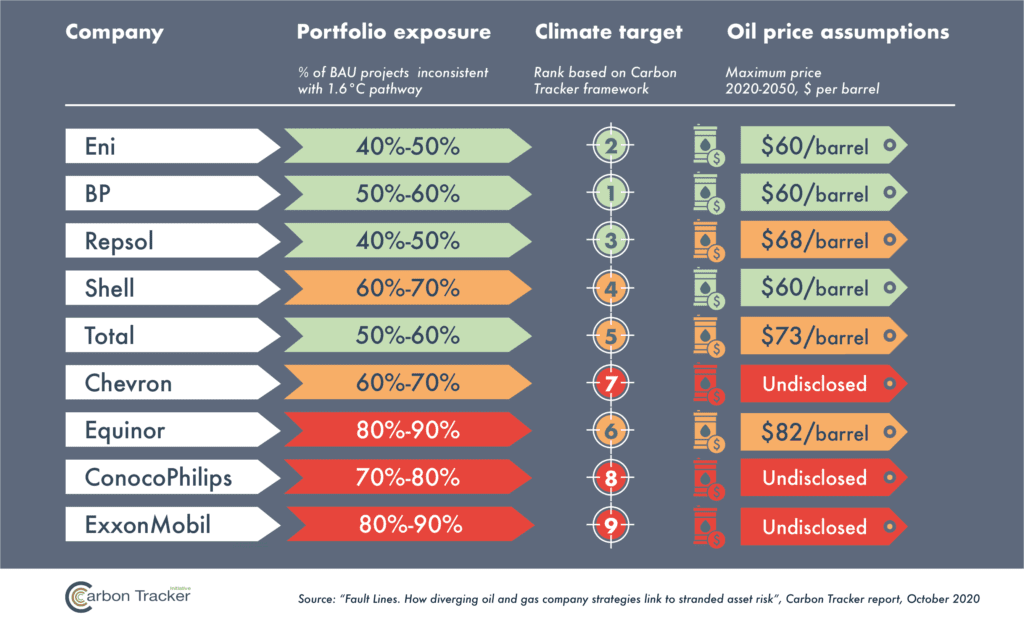

Oil and gas companies’ emissions ambitions, scale of capex at risk and internal oil price assumptions for impairment tests are all highly correlated. Companies are increasingly either approaching climate issues holistically or getting left behind on all three. These aspects may be seen as proxies for each other – setting conservative price assumptions or stronger emissions targets appears to link to portfolio management that is more resilient in the transition.

European producers clearly outperform their US counterparts on all three factors in the report. Equinor is a notable laggard.

US companies don’t disclose their impairment price assumptions. However, these strong relationships and poor performance on the other factors suggest that their assumptions of long term oil and gas prices are high, raising the risk of asset write-downs in future and possible continued investment in stranded assets.

Companies are taking diverging views of the future – this further exaggerates the gap between leaders and laggards. We explore using each company’s internal accounting price assumptions as an indicator of how conservative they will be in their future project sanction activity.

We highlight $60bn capex associated with the 15 largest projects sanctioned in 2019 that aren’t competitive on economics under the International Energy Agency’s 1.65-1.8˚C Sustainable Development Scenario (SDS). Most of the majors sanctioned assets that fell into this category. ConocoPhillips is the exception, only sanctioning assets that fall outside the lower-fossil fuel/higher-ambition 1.6˚C Beyond 2 Degrees Scenario.

All of the majors have assets available for sanction in 2020- 22 that fall outside the SDS. Timing of approval of these assets is extremely uncertain in the context of Covid-19. However, they may prove a key indicator of company commitment (or lack of) to resilience in the energy transition, or perhaps whether oil company long term demand expectations have been fundamentally shifted down by the crisis.