Key Resources

Oil and gas companies are still failing to commit to the absolute emissions reductions necessary to link their businesses to the finite limits of the carbon budget.

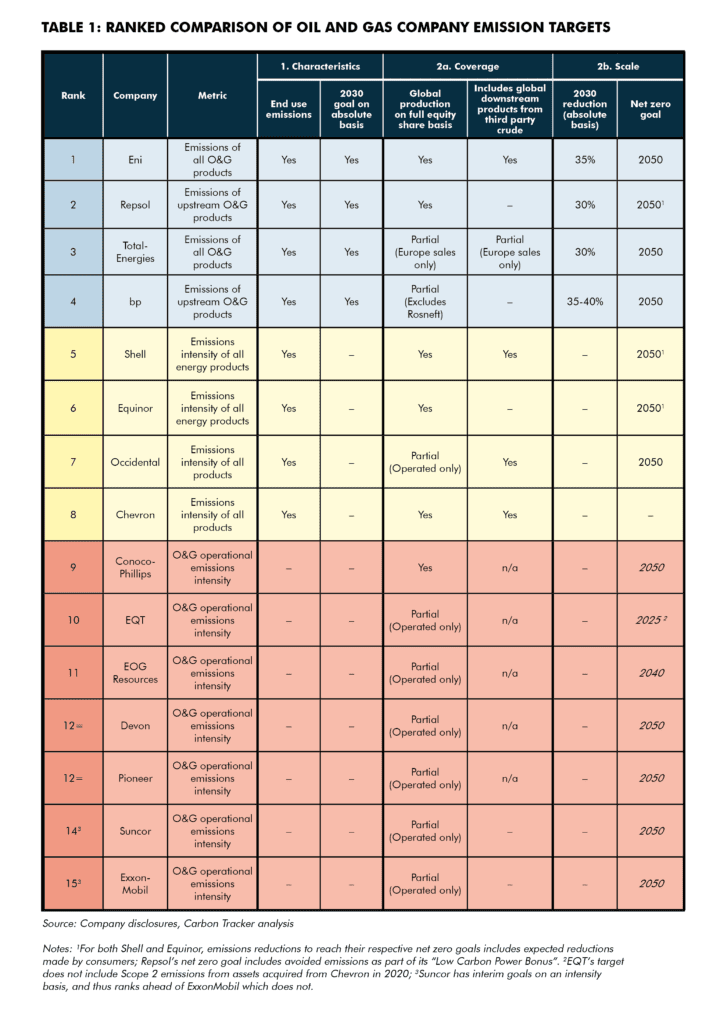

For the third year running Carbon Tracker’s Absolute Impact report assesses and ranks climate policies, expanding its analysis to cover the 15 largest publicly traded oil and gas companies. It warns that net zero targets are not enough for companies to be aligned with Paris – they need absolute limits on future emissions and significant interim targets.

A key element of this year’s analysis is a greater focus on the credibility of companies’ approaches to emissions reductions and the degree to which their efforts contribute to a genuine fall in global emissions levels.

Since the first publication of this report in 2020, there are now many more “net zero” goals. However, not all company targets, or ambitions, are created equal in the degree to which they reduce the impact of company activities on global temperature rise.

Key Findings

- Net zero goals alone are insufficient to reduce carbon emissions in line with Paris goals and curb corporate transition risk.

- We provide a relative ranking of the emission reduction targets of 15 of the largest listed oil and gas companies based on our “Hallmarks of Paris Compliance” (majors plus Equinor, Occidental, Repsol, Devon, EOG Resources, EQT, Suncor, and Pioneer).

- Tier one includes those with absolute reduction targets including Scope 3 emissions

- Tier 2 companies are those with scope 3 emissions reductions on an intensity-only basis.

- Tier 3 includes companies with only operational intensity (Scope 1 & 2) emissions reduction goals.

- Setting appropriate targets is just the first step; the approach to achieving emissions reductions must be credible to ensure that both stated reductions occur and that shareholders’ exposure to transition risks are not increased.

- Asset divestments must not be used to justify continued investment in new fossil assets.

- The ability of emissions mitigation technologies such as CCUS and “nature-based solutions” to deliver stated reductions must be scrutinised.

- 3rd Party offsets may not actually lead to emissions reductions.

- Winding-down existing assets is the best way to reduce both the climate impact of company activities and transition risk for investors.

- To support investors’ engagement with companies we define a set of “Credibility Criteria” to assess company plans to reduce emissions