The Network for Greening the Financial System (NGFS) is comprised of 144 central banks and supervisors, plus 21 observers (as of 11 March, 2025[1]) committed to knowledge sharing and development of climate and environment-related risk management in the financial sector – mobilising finance to support transition to a sustainable economy.

After five iterations of the NGFS long-term climate scenarios and following user feedback from the financial community, the NGFS published new short-term scenarios (through 2030) on 07 May 2025.[2] The intention is to provide ‘decision useful’ scenario outputs focussed on the current business, credit and electoral cycle which better reflect investment horizons.

Baseline Scenarios

The baseline scenario is calibrated using the October 2023 IMF World Economic Outlook projections:

• The macroeconomic variables used to align the models to the IMF projections are GDP, inflation, technical progress, sectoral growth, population levels, and consumption patterns.

- The impact of COVID-19 and the energy price shocks of 2022 are considered in the calibration of the monetary policy response.

Key innovations of the NGFS short-term scenarios include:

- modelling of compound extreme climate events (simultaneous occurrences of multiple bundled hazards such as floods & storms (wet); and heatwaves, droughts, and wildfires (dry));

- incorporating cross-regional transmission of shocks (short-term spillover effects of both transition and physical shocks through trade and financial linkages);

- providing a framework to study the interplay between climate risks and business cycles, by integrating climate policy, extreme weather events, economic trends and sectoral dynamics;

- zooming in on a policy-relevant timeframe for financial stability and monetary policy;

- providing granular economic and financial data across a wide range of sectors and countries, and capturing the inflationary impacts of climate damages.[3]

The NGFS suggest ‘these features make the short-term scenarios well-suited for climate stress-testing exercises and for analysing financial risks that may materialise within a business-planning, policy- relevant timeframe’.[4]

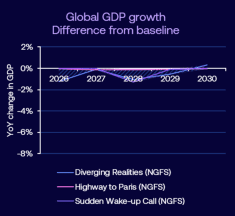

Four distinct narrative scenarios are presented – exploring diverging levels of climate policy action and physical climate risk to 2030.

Key Messages of the Short-Term Scenario Outputs Include

- The possible occurrence of a sequence of plausible but extreme weather events in one region causes substantial GDP losses, with effects on the global economy. The impacts of these extreme disasters vary across regions, with losses peaking at 12.5% of GDP in Africa. Effects of regional disasters affect the global economy through trade and financial linkages.

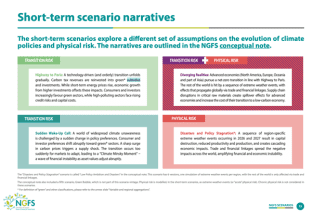

- Default probabilities rise significantly for high-capital and high-debt sectors, with increases of more than 10pp in the power supply sector (albeit from a low base).[5]

- Rapid and unexpected policy shifts increase the economic costs of transitioning and cause additional financial stress. A delayed and abrupt transition generates global output losses of 1.3% (each year) and increases the unemployment rate by 1.3pp. Default probabilities rise significantly in several sectors, with increases of more than 10pp in the power supply sector, due to its high capital intensity and high debt to capital ratio.[6]

What the short-term scenarios get right?

- The short-term scenario narratives include four plausible story lines with varying assumptions around the short-term evolution of climate policies and physical climate risk. This storyline approach to qualitative climate scenarios is broadly comparable to the approach TREX analysis take with narrative based scenarios – first developed with Exeter University and USS[7] to be more intuitive for pension fund trustees.

- The short-term scenarios focus on the period 2025 – 2030 – a window of time deemed “decision useful” for institutional investors, corporate financial planning and politics, with 2030 a key waypoint towards net-zero 2050 targets.

- The focus on hardest hit regions (Africa, Asia) and sectors (agriculture, fossil energy/ coal) provides investors with actionable information regarding how the differing pace of transition and manifestation of climate risk is likely to impact GDP output, default rates, and capital costs in regions and key sectors in which they invest, especially energy, where viable transition plans are lacking.

What the short-term scenarios could improve?

- Like the NGFS long-term scenarios, due to the inherent uncertainties, the short-term scenarios exclude the plausible possibility of triggering climate tipping points – potentially resulting in cascading physical climate damages[8] – thus ignoring potential for catastrophic risks.

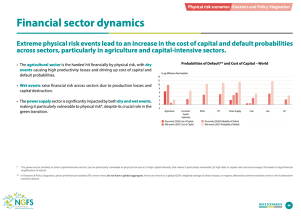

- Sovereign default risks, as in the long-term scenarios appear insufficiently captured. Page 66 of the Technical Documentation[9] states: sovereign default probability can be approximated by a linear combination of sectoral default probabilities (if the latter are calibrated on the same exogenous default probability as the former). Petrostates reliant on high fossil prices and demand with high fiscal breakeven prices are uniquely exposed to a moderately paced transition – refer CTI Vulnerability Chart – Petrostates of Decline (2023) report[10].

- The distorting impacts of subsidies – such as the estimated $7 trillion annual global subsidy to prop up fossil fuels (IMF 2022) – are not captured.[11]

- By design, there is no probability of occurrence attributed to each narrative scenario – the NGFS suggest “to address this – you can either hire experts to share expert opinions – or rely on the market to infer default expectations”[12]. The scenarios are primarily designed for stress-testing, not intended as forecasts.

- The accompanying technical documentation pg 5 states: “In terms of the interplay between transition and physical risks in the short-term time horizon, it is important to note that transition risk has little to no impact on physical risk over the short- term scenario forecast horizon of five years. Climate change impacts experienced now are the result of past GHG emissions and concentration in the atmosphere.” – While this is true for CO2 (10yrs + lag), other emissions, notably methane and aerosols are much faster acting – and should be considered separately[13] according to the Global Heat Reduction Initiative.[14] Around 30% of all post-industrial warming has been caused by methane[15], yet emissions are standardised for accounting purposes into tonnes CO2 equivalent.[16] Given the recent expansion of gas power and LNG in the global energy mix, faster acting methane emissions should be accounted for separately, to better reflect the short-term warming impacts of the dash for gas.

- The NGFS short-term scenarios are said to have ‘limited comparability’ with the long-term scenarios, due to different modelling approaches.

NGFS Comparisons With Investment Consultants Narrative Scenarios

TREX analysis have published their own assessment of NGFS scenarios against their own short-term scenarios which can be read in full here.[17]

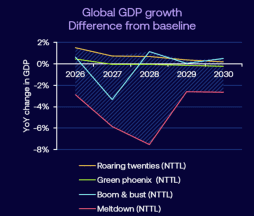

TREX representation of 3 of 4 NGFS Scenarios (no Disasters/Policy Stagnation)

Equivalent GDP damages in TREX NTTL Narrative Scenarios

In terms of both GDP damages, and the pace of adoption of new scientific research and modelling techniques – it should be noted that relative to individual investment consultants, the NGFS is constrained by its large and geographically dispersed international membership and governance model of consensus decision making.[18]

The objective of the NGFS is to support the widespread adoption of practices by financial sector actors and policy makers to include climate considerations in their assessments and analyses. Standardisation of approach and comparability across institutions is key, adopting well established climate assumptions and models for the production of scenarios.

As observable in other consensus-based forums such as the IPCC or COP – it is commonplace for outputs agreed by consensus to lag cutting edge science, particularly on knowledge frontier topics like climate tipping points, where uncertainty remains.

In areas of imperfect knowledge, but catastrophic potential risks, scientists advocate for the precautionary principle to reduce the likelihood of occurrence, until we know risks can be avoided.

Conclusion

Drawing attention to the heightened default risks for exposed sectors in the NGFS short-term scenarios may prove to be more effective at changing investor behaviour than the more typical % global GDP damage figures frequently cited in long-term scenario analysis. Investors own stocks and bonds, not GDP.

As a recently emerging practice, the relationship between higher future damages in climate scenario analysis, and resulting investor behaviours, such as revised net zero target setting, investment tilts and increased allocations to solutions remains both poorly studied and understood.

With 140+ global central banks now looking to deploy NGFS short-term scenarios for financial sector supervisory purposes – the outcomes of upcoming stress test exercises deploying the new scenarios will be closely watched.

With ‘decision useful’ scenarios – the NGFS is heading in the right direction, but there is more work to be done to ensure that financial sector expectations of future physical climate damages are aligned with climate science.

Ultimately, it is what happens to real-world financed emissions that counts.

—————————————–

[1]https://www.ngfs.net/en/publications-and-statistics/publications/ngfs-short-term-climate-scenarios-central-banks-and-supervisors

[2]https://www.ngfs.net/en/publications-and-statistics/publications/ngfs-short-term-climate-scenarios-central-banks-and-supervisors

[3] NGFS Short-Term Scenarios Technical Document pg 7: “for physical risks, EIRIN captures climate effects on endogenous growth mechanisms & the macro-financial response of the economy in terms of fiscal, monetary & adaptation policies. It thus derives dynamic trajectories of GDP, inflation, & policy rates that account for both direct macro-economic impacts & their potential macro-financial amplification”

[4] Refer to NGFS Short-Term Scenarios – Main Takeaways – p3 https://www.ngfs.net/en/publications-and-statistics/publications/ngfs-short-term-climate-scenarios-central-banks-and-supervisors

[5] Refer NGFS Short-Term Scenarios presentation pg 6 https://www.ngfs.net/en/publications-and-statistics/publications/ngfs-short-term-climate-scenarios-central-banks-and-supervisors

[6] Refer NGFS Short-Term Scenarios presentation pg 6 https://www.ngfs.net/en/publications-and-statistics/publications/ngfs-short-term-climate-scenarios-central-banks-and-supervisors

[7] https://www.uss.co.uk/news-and-views/views-from-uss/2023/09/09072023_improving-climate-analysis-with-the-university-of-exeter

[8] https://esd.copernicus.org/articles/15/41/2024/

[9]https://www.ngfs.net/en/publications-and-statistics/publications/ngfs-short-term-climate-scenarios-central-banks-and-supervisors

[10] https://carbontracker.org/reports/petrostates-of-decline/

[11] https://www.reuters.com/sustainability/trillion-dollar-question-fossil-fuel-subsidies-2024-11-15/

[12] NGFS guidance to users via the short-term scenarios launch event 12/05/25

[13] Refer to The CCC (2019) – Briefing Note on Time Lags in the Climate System: “When emissions are reduced the response of radiative active species in the atmosphere is more complex. For short lived greenhouse gases, the concentrations and radiative forcing can quickly decrease, for instance for methane significant concentration reductions over a decade would be expected following a large reduction in emissions” https://www.theccc.org.uk/wp-content/uploads/2019/07/Briefing-note-on-time-lags-in-the-climate-system-Met-Office.pdf

[14] https://trellis.net/article/global-heat-reduction-initiative-short-lived-pollutants/

[15] https://www.iea.org/reports/global-methane-tracker-2022/methane-and-climate-change

[16] https://trellis.net/article/global-heat-reduction-initiative-short-lived-pollutants/

[17] https://www.linkedin.com/pulse/climate-scenarios-compared-why-nttl-ngfs-paint-czuye/

[18] https://www.ngfs.net/en/about-us/governance