“It’s now cheaper to save the world than destroy it.”

Akshat Rathi, Climate Capitalism

“It ought to be remembered that there is nothing more difficult to take in hand, more perilous to conduct, or more uncertain in its success, than to take the lead in the introduction of a new order of things.

Because the innovator has for enemies all those who have done well under the old conditions, and lukewarm defenders in those who may do well under the new.

This coolness arises partly from fear of the opponents, who have the laws on their side, and partly from the incredulity of men, who do not readily believe in new things until they have had a long experience of them.”

Niccolò Machiavelli, The Prince

We are at a time where the ambition to re-create the global energy system in a vastly different way is underway at scale, and with a hard deadline ahead of us to achieve it.

The two quotes above are from this year, well into the energy transition, and from 1532 almost 500 years ago.

Rathi points out the failure to change will cost us far more than making that change happen quickly – the climate impact in many cases may be irreversible in human timeframes, and cause much damage to human habitation and the wider environment in the very near-term.

Machiavelli points out from half a millennia ago that humans however do not embrace change easily, and until the consequences are obvious and personal.

But, we may be at that juncture of “long experience” that humans need to act.

Not only are climate temperatures now long into an upward march toward 1.5°C, new technologies of wind, solar, battery storage and nuclear have been with us now for over 50 years, and are emerging at scale and at costs that are cheaper than existing fossil fuel alternatives.

That meets Rathi’s plea that clean technologies and capitalism work together to accelerate a better energy system that is long-term sustainable for the planet.

Yet we need to be aware that incumbents “who have done well under the old conditions” will often resist this change in overt and subtle ways such as “investing” in false solutions, or slowing legislation or policy changes.

This month’s Monitor covers several new reports and blogs from Carbon Tracker’s latest research which cover a range of energy change issues and initiatives, from the state of transition in the nation of Kazakhstan, to the more rapid progress of a major global utilities provider and a review of latest policy and corporate disclosure programs to accelerate energy change.

Power & Utilities – Analyst Note

In a detailed analyst report from our power and utilities team (in collaboration with the European Bank for Reconstruction and Development – EBRD) the Kazakhstan Energy Transition , we see a microcosm of the global energy transition – its promise and the resistance to it.

Kazakhstan – A Lack of Political Leadership and Green Ambition: although Kazakhstan has committed to net zero by 2060, there is no underlying political support to achieve this goal.

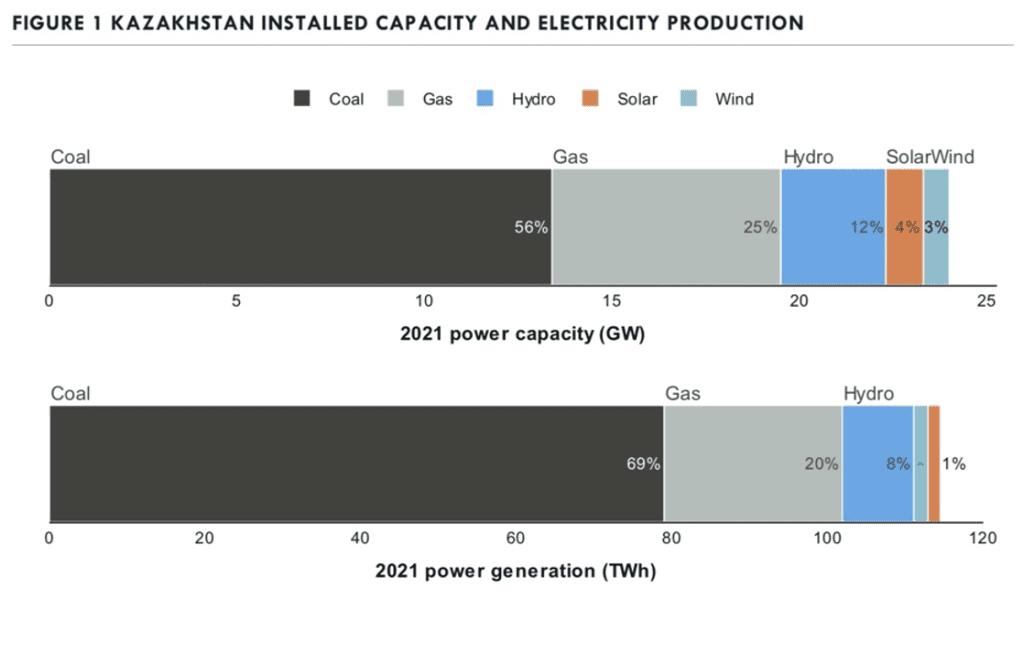

Kazakhstan produces about 0.7% global emissions, and 1.4% global coal.

So this analysis is not about the global impact of Kazakhstan’s emissions targets: rather it is a story that highlights how opportunities to improve and cleanse national output is being missed, and putting further economic and environmental strain on the country – in a sense a microcosm of the global issues facing the energy transition.

Current political and technology commitments will lock-in legacy fossil fuel infrastructure and crowd out renewables. Continued support for coal will create long-term economic risks and deter investment from economic activity that could diversify Kazakhstan’s economy and facilitate a just transition.

The main barriers to the transition are:

- coal is the cheapest source of existing power in Kazakhstan (though this will change);

- grid infrastructure has suffered from multiple years of underinvestment and is not ready for large-scale integration of renewables;

- reliance on the energy system of neighbouring Russia for expensive balancing services impedes large scale renewable development;

- there is limited awareness of climate change and its impacts within the Kazakh population, yet climate change impact on Central Asia expresses itself in increasing drinking water scarcity loss of biodiversity and degradation of the ecosystems – making many thousands of Kazakhs vulnerable to flooding;

- having cheap power and heating, however unreliable, is the main priority; and policy support favours fossil fuels over clean technologies with no support for large scale coal phaseouts.

Nevertheless, Kazakhstan has significant potential for utility-scale renewables deployment and could become a major clean energy exporter provided there is a commitment to stick to the sectoral decarbonisation strategy.

Key Findings

- The upcoming 10-15 years will be critical for laying the foundation of the new economy. Failure to do so will result in economic stranding as legacy revenue streams and old economy jobs dry up without the offset from new (clean) revenue streams and labour opportunities.

- Kazakhstan’s low carbon price does not incentivise energy transformation and is an ineffective tool given the ready availability of free quotas.

- Storage at scale will be required by 2030 to account for growing renewables integration and will be essential to provide flexibility to the system.

- Without financial aid Kazakhstan cannot accelerate its transition to clean energy

- Current political and technology commitments will lock-in legacy fossil fuel infrastructure and crowd out renewables.All else equal, power prices will significantly rise with the addition of new coal plants or retrofitting of existing ones.

- Inclusion of renewables which have demonstrated declining price trends will lower power prices to end users.

Without these new plans, policies and investments the following future plays out for Kazakhstan: more coal, more risk of economic and environmental degradation at home and abroad, and more costly heat and power as the opportunity for clean energy implementation is missed.

Three charts outline the gloom.

1 – Kazakhstan’s current energy supply profile by energy source – heavy reliance on coal

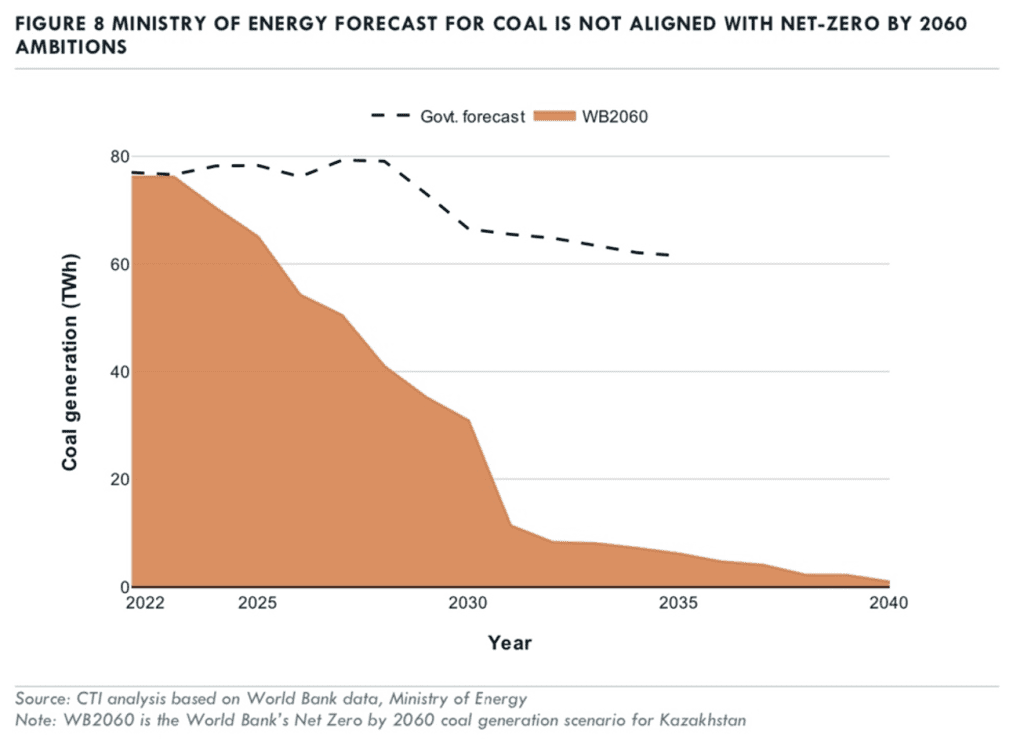

2 – Kazakhstan’s long-term addiction to coal: an unambitious energy transition plan nowhere near 2060 targets – coal plant generation barely changed

2 – Kazakhstan’s long-term addiction to coal: an unambitious energy transition plan nowhere near 2060 targets – coal plant generation barely changed

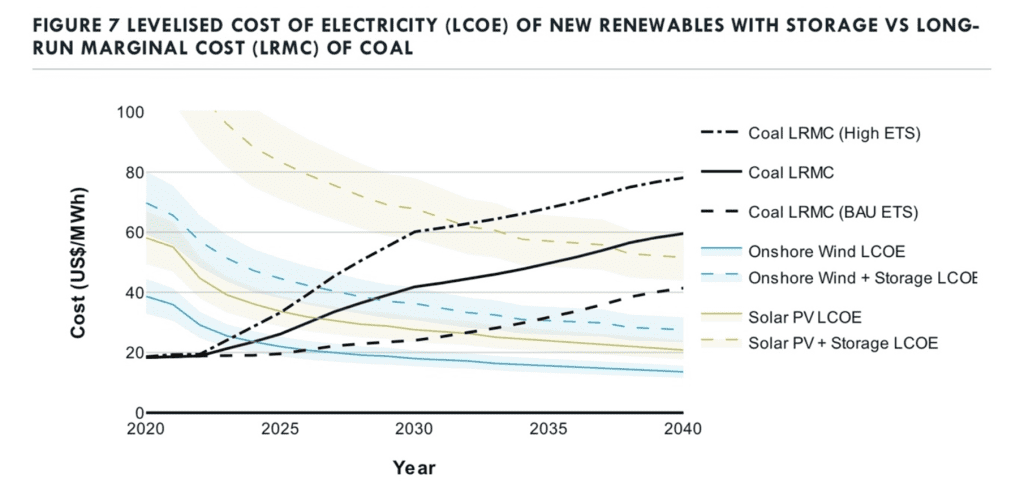

3 – Kazakhstan misses opportunities to change to cheaper, cleaner energy

The rising costs and missed opportunities of lower cost renewables by pursuing business-as-usual (BAU). Even in the mid-case scenario wind with storage is cheaper than coal now, and solar with storage cheaper by the early 2030s.

Given the continued reliance on costly coal, and the lack of planning for a real transition to 2060, Carbon Tracker has laid out the framework for change.

Priorities

- Create a holistic system of carbon regulation which covers the whole economy:

- Produce a unified and cohesive electricity plan overseen by one Government ministry:

- The Government should apply to the international community for transition financing

- Transmission and distribution tariffs should adequately reflect investment costs required for updating the grid system;

- Identify renewable energy regions for development;

- Develop and implement a plan for decarbonising thermal energy production and supply:

- Improve energy efficiency measures.

Practical Steps

- Carbon pricing will be a key policy lever: there should be material annual phased reductions of quotas from 2023 onwards and the Government should conduct auctions for carbon credits from 2024.

- Incentivise renewables with storage in separate auctions to improve system flexibility: a minimum standard for storage requirements should be defined which will enable the storage roll-out needed for balancing the system as more coal plants retire towards the end of the decade.

- Develop a coal phase out plan: begin engaging with stakeholders to wind down coal plants and devise a detailed retirement plan. In addition, no new coal plants should be developed. Carbon Tracker can provide a unit-by-unit coal retirement plan based on our least cost modelling and scenario analysis.

- Develop a heat energy decarbonisation plan and integrate it into the overall energy transition plan: establish a working group on heat energy supply decarbonisation at the Ministry of Energy level; conduct technology analysis and best practice analysis in compatible climate economies and implement diverse pilot projects.

- Improve the robustness of the financial sector: a stronger regulatory authority, enhanced transparency of public sector support and elimination of interest subsidies

- Define areas and resources for renewable energy development: key steps include assessing resource potential, pre-approving land permits to avoid development delays and encourage investments, and ensure availability and robustness of grid connections.

Full details can be found in the main report.

Power & Utilities – Corporate Research

Iberdrola S A – transitioning a corporation

As in the Kazakhstan example above, the complexity of change in the energy transition is also clear at a corporate energy level.

This month we looked in depth at one of the major global power and utility players at the front-end of the energy transition, Iberdrola SA.

Iberdrola is Europe’s largest and the World’s second largest utility by market cap. It is an integrated power utility with 53GW of generation capacity of which just over 40GW is renewables, mainly onshore wind & hydro.

It is the World’s No.1 wind power generator, and has a network asset base of €39bn and 36m end users. The global workforce is nearly 41,000.

The good news is Iberdrola is nearly Paris aligned for net zero emissions by 2030, showing major corporate leadership, – but it does still face the challenges of residual gas operations and scope 3 emissions (those emissions from the activities of Iberdrola’s suppliers and customers, rather than those directly from Iberdrola’s business actions – Scope 1 and 2. Note, Scope 3 emissions tend to be the highest of all – typically 70-80% total emissions).

Iberdrola shows the process of how to transition from a fossil fuel electricity generation system to an almost emissions-free one in the space of just over a decade.

It has closed higher-emitting assets first: 8.5GW of coal and fuel oil generation capacity since 2001, and closed all coal capacity in 2020.

This has achieved annual emissions reduction of 7% pa over 2017-22, implying an achievable annual reduction 2030 target of 6.5%pa to 2030, and so mostly meeting its Paris commitments by reducing scope 1 emissions by over 95%, and scope 1 and 3 emissions by 85%.

It is also planning to add 12GW of renewables over 2023-25, an increase of 30% to 52GW.

This leaves gas and Scope 3 emissions to focus on

In terms of gas, Iberdrola does not have a formal date for an exit from gas generation. But profits from its current gas assets in Spain are declining in profitability as load factors drop to about 10% – with Spain’s renewable targets of 80% by 2030 this will contribute to further decline. A faster exit from the gas business would secure Iberdrola’s alignment with its Paris targets.

A residual Scope 3 emissions rate of 25 mt pa footprint by 2030 remains a harder problem to solve – with Iberdrola aiming to use offsets, rather than abatement in this area.

Medium-term focus on grids as well as renewable capacity as the transition matures

Spanish nuclear, onshore wind and hydro are the biggest single sources of Iberdrola’s current EBITDA.

But Iberdrola’s 2023-25 €47bn capex plan marks a shift in emphasis away from renewables towards grids, with an organic split of 50%/44% (and 6% in other areas).

This reflects partly on cost inflation in renewables but also on the impact of higher interest rates on the balance sheet and credit rating in the face of greater macro uncertainty.

Longer term, it plans to invest €65-75bn over 2026-30, with an increase in renewables capacity to 80GW.

In sum

Overall, Iberdrola has seized the opportunity to re-orient itself to remain profitable in a renewable energy system. It has been able to transform supply inputs from fossil fuels to renewables and so span the energy transition effectively for consumers and shareholders.

The share price performance indicates the positive market view of this approach over the past five years.

Policies, profitability and strategy are aligned and in line with Paris commitments.

Iberdrola is in a mature phase of transformation, and with investors and management now with “long experience” of the new system.

Contrast this with the earlier story from Kazakhstan where the policies, will, technology and strategy to shift to renewables remain missing, or are in the very early stages of reluctant development.

Accounting for Change

Carbon Tracker Methodologies – CA100+

As the transition progresses Carbon Tracker is involved in a number of analytical and assessment initiatives to expose the extent of change to investors and stakeholders of energy firms.

We use these assessment products to monitor how corporations, like Iberdrola, are progressing toward to Paris targets, and so avoid the risks of stranded assets or underperforming assets for their investor base.

One key area of activity is our support to the Climate Action 100+ group – an investor-led initiative to ensure the world’s largest corporate greenhouse gas emitters take necessary action on climate change.

As a research partner to Climate Action 100+ (CA100+), Carbon Tracker Initiative conducts financial analysis and has developed a set of alignment assessments to help investors identify, quantify, and assess stranded asset risks for 69 focus companies, covering:

- 36 upstream oil & gas exploration and production companies’ investment plans, and

- 33 utilities’ announced retirement schedules of coal & gas fired electricity generation

to assess their alignment with the goals of the Paris Climate Agreement. More details are here.

This latest updated document sets out the framework and methodology for how Carbon Tracker Initiative (CTI) assesses company financial statements (and related auditor reports) for consideration of climate risk, as part of the Climate Accounting and Audit Assessment of the Climate Action 100+ Net Zero Company Benchmark.

The Climate Action 100+ Net Zero Company Benchmark draws on distinct analytical methodologies and datasets from public and self-disclosed data from companies, broadly categorised into two types of indicators: Disclosure Framework Indicators, which evaluate the adequacy of corporate disclosure, and Alignment Assessments, which evaluate the alignment of company actions with the Paris Agreement goals.

The Climate Accounting and Audit Assessment covers both disclosure and alignment and can hence be considered a “hybrid” assessment.

Carbon Tracker are partners in other initiatives in this area such as the Global Registry of Fossil Fuels released last year.

The politics and processes of disclosure and emissions improvements are also highlighted below in a new initiative we covered in the Golden State in the US.

Policy Review – California Takes the Lead on Emissions Disclosure

As the Iberdrola tale shows, as we progress into the transition further and further, confident companies are starting to drive the energy transition.

One can weave complex theories as to why this would be the case, but simpler is often better. If you have the capability to transform your firm into a new energy leader, into an industry that is growing quickly and globally – think wind, solar, EVs, heat pumps, batteries and storage – why would you not invest in that future?

In addition, if policy rewards disclosure and improving decarbonisation and investment in new technology, and penalises laggards in the incumbent industry that “have done well under the old conditions”, then the leaders will embrace the new policy directives.

Carbon Tracker notes an important case in point in a policy blog post released this month.

In early September, the California State Legislature passed bill CA SB253, which requires all companies in the state that earn $1 billion or more annually to disclose their scopes 1, 2, and 3 emissions publicly.

The significance of this is that soon investors will be able to know who is actually following through on pledges to reduce emissions, and importantly whose bottom line is most likely to be hit by potential future climate regulations or the energy transition to a low carbon economy.

While some might dismiss this as only being action in one state, it is important to remember that California, on its own, is the world’s fourth-largest economy. As Politico reports, the measure applies to 5,400 companies including Fortune 500 companies like HP, Intel, Chevron, Cisco Systems, and Wells Fargo, which have operations around the US and globally.

Although some business lobby groups, like the California Chamber of Commerce, opposed it, several companies like Apple, Microsoft, and Ikea stated their public support for the bill.

One reason California is seen as an innovator in policy is that many of the things that start in their laboratory of democracy soon become adopted by other states and even impact national policy

The importance of state action is magnified by the fact that even as this problem continues to plague investors, there has been little action at the federal level. For months, advocates have been waiting for the U.S. Securities and Exchange Commission (SEC), – a major federal financial body to issue similar regulations.

As the transition progresses, policy action such as this at local and then national level will be picked up by the new winners of the energy transition, and likely force changes as investors and corporations gain experience in the new system.

Conclusion

As Machiavelli noted – change is hard, but the rewards and risks in the energy transition are incredibly large.

As the transition progresses at growing pace and “renewables” become the norm, it is becoming clearer to see how making the change is going to be cheaper and less precarious than clinging to business-as-usual.

We now have much experience in the new technologies, and also growing experience of the climate impacts and associated costs of slower change or inaction.

The numbers are increasingly showing that for nations and corporations it is cheaper to improve the energy system than court destruction by not changing now.

—End

References

Iberdrola SA: Time to review CCGT

California Takes the Lead on Emissions Disclosure