To paraphrase the Charles Dickens classic, A Tale of Two Cities: in 2023 in terms of energy, we are in the best of times, and in the worst of times, in a fast- growing age of new clean technologies, but still in a phase of fossil fuel dependency.

Thus the energy transition has entered a key stage of the new replacing the old – putting a lot at stake in the next few years.

So this month’s Energy Transition Monitor will focus exclusively on the Carbon Tracker Annual Review 2022, and taking a slightly longer-term perspective on our activities and impact over the past year, and our body of work for the last decade or more as we enter this crucial period.

There are plenty of details in the report which cover many aspects of the energy transition in general and our work and products in particular – this Monitor will therefore just pick out a few highlights. The reader is encouraged to read the whole account.

However, the report starts with an intriguing question: Are we winning?

We’ll provide a provisional answer to this at the end of this Monitor but to be a little pedantic, we’ll need to answer who is the “we”, and what is “winning” – which we will get to.

All of this needs us to take a step back, as the Annual Review report does.

As the foreword puts it:

“We are caught in a paradoxical moment – looking back to last year’s successes and forward to our challenges ahead, we are facing a race against time. Earlier this month, HM King Charles III unfurled the UK’s Climate Countdown Clock and on Saturday July 22, 2023, the clocks around the world ticked down below six years for the first time. Meaning, we will have less than six years to dramatically reduce fossil fuel emissions to stay below 1.5°C degrees warming. “

This time last year we also asked ourselves, ‘are we winning?’ and released Unburnable Carbon: Ten Years On as an update on our first Unburnable Carbon report published in 2011.

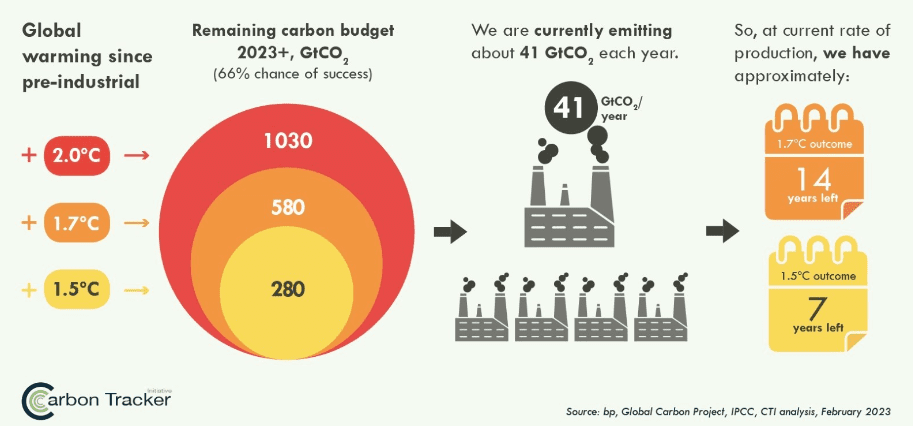

The findings were disquieting—our “safe” carbon budget had nearly halved over the past decade, with over $1 trillion worth of oil and gas assets at risk of being stranded.

Back in 2011 we had perhaps 18 years of “safe” carbon budget: when we released that updated Unburnable Carbon report it was perhaps 9 years: and now as we note we have between six and seven years to go on current emission rates to meet a 1.5°C target.

On the plus side, however, the financial stranding risks are increasingly being recognised outside the upstream oil and gas industry and we are seeing a ‘mainstreaming’ of the thesis we set out to answer a decade ago.

One of the fundamental questions any philanthropic backed initiative has to ask, is ‘have we backed and funded the right strategy?’

So we were pleased to see Goldman Sachs address this directly in a new research report, entitled ‘Top Projects 2023-Back to Growth’, 27th June 2023, reviewed in Forbes on July 20th, that wrote: “One point of controversy that has impacted industry investment over the past decade is the theory involving ‘stranded assets,’ i.e., that a significant percentage of proven reserves would eventually be left in the ground as the energy transition progresses. curtailing investment, in turn cutting global oil resource life since 2014 from 50 years to just 23 years.”

As the article notes, the stranded assets theme has acted as a constant brake on unfettered oil and gas investments, helped deliver the ESG financial concept, and at least forced the incumbent fossil fuel industry to pause to think about not just about can they build new assets, but should they build these assets: forcing wider debates about stakeholder interests of risk, return and environmental impact and reputation.

Let us also be honest: the incumbent industry is railing against this concept and using excuses of “security” and other delay tactics: but the stranded asset risk hovers above them, and continues to propel a more balanced debate (to remind, OPEC+ is into its 8th year of production cuts, whilst protesting about the ability to invest in new supply.)

So – as the world at large confronts these fast-approaching challenges, our work has become more important and urgent than ever.

Our in-depth country research enables investors to assess climate risks that stakeholders may consider in their transition plans.

By focusing investors on climate change as a financial threat we can accelerate the shift away from risks posed by fossil fuel stranded assets, resulting in a managed and swift transition. Providing company profiles informs investors and asset managers on specific risks carried by fossil assets, against projected models of the energy transition and the companies’ own Net Zero statements.

The scientific data analysis and financial reasoning that drives our work is valued not only by investors, but by a wide range of elected officials and experts, regulators, policymakers and NGOs. Even in highly regulated markets, our research assists stakeholders in influencing decision-makers to shift away from fossil fuel technologies on economic grounds.

In recent years, therefore we have focused on moving the debate with investors and policymakers to how systems and industries need to be shaped for a secure and affordable timely energy transition, and how policy, regulation, and investors can drive market-based financially sustainable solutions.

Alongside continuing our core work on Oil, Gas and Mining and Power and Utilities, we have expanded our research into accounting disclosures by companies related to Paris alignment, asset retirement obligations (AROs), and analysis of individual company transition plans – helping investors understand plans at specific company level, to actively engage with management.

We also furthered our work on the energy transition with the development of research workstreams on Clean Tech and Automotive, including country-level and company-level profiles looking at the potential financial risk of stranded assets as we move towards the unavoidable switch away from fossil fuels.

The report then covers our other major activities in Corporate Research, Audit and Accounting , Investor Outreach programs and Special Initiatives such as the support in creating the Global Registry of Fossil Fuels.

Furthermore, we overview key supporting functions in Communications, Events and Thought Leadership, Distribution, Partnerships and core internal processes in Operation and Finance and Diversity, Inclusion and Sustainability initiatives

Our work is aimed to reinforce the inevitability of transition: continuing to influence investors, regulators, and policymakers towards aligned pathways to tackle the rising climate change risks, as urgency to act grows.

Data and financial analysis and technical insights are the bedrock of our activities, but so also are the areas of thought and policy leadership.

Over the last decade we have also shown how the new scalable clean-technologies – wind, solar, batteries, heat pumps and others are economically and financially beneficial for direct stakeholders (investors, governments, corporations, consumers) but also benefit the far wider challenge of decreasing global air pollution and reducing global climate change risks.

To this point, the meme of stranded assets may have significantly curtailed oil and gas over-investment and accelerated alternative technology hyper-investment – as it cascaded from an idea, into policy development, and from there to sound economic new technology investments and away from high risk ones such as long-term fossil fuel assets.

To emphasise this we are preparing an upcoming blog looking at how to measure success in terms of avoided stranded assets, and the heightening risks of over-investment.

Full details will be covered in September’s Monitor with links to the blog.

So here is the better news.

Whilst the carbon budget has declined each year as emissions remain persistent, 2023 is a good year to review the broad landscape for three reasons:

- It is likely to be the year which global emissions peak, and start their decline, creating more time to reach climate goals

- It marks the year in which new technology investments in wind and solar in absolute and energetic terms are higher than oil and gas investments for the first time, and new power generation from renewables outstrips new global power demand causing fossil fuel power generation into decline

- It is a year in which new policy initiatives such as the US IRA and the EU Green Deal will start to cause significant mobilisation of governmental forces and financial support behind renewable technologies and major investments to catalyse the major new private capital technology investments under way

Indeed, back in 2011 when Carbon Tracker launched the concept of stranded assets, fusing economic interest and environmental degradation, there were negligible solar panels, wind turbines, electric cars, battery storage or heat pumps in existence.

Less too cheap to meter, more too small to matter.

But 12 years on these new technologies make up almost 15% of global electricity production, and 5% of primary energy consumption.

With growth rates still sticky at 15-20% per year even at this scale, there is a clear path to new technologies and hydro and nuclear power forming over 50% of the global power system by 2030.

Also back in 2011 electric vehicles (EVs) were barely noticeable: today there are over 30 million EVs on the road. By 2030 perhaps 25% of the global fleet may be electric, powered by ever cleaner power energy sources, and by some estimates removing between 4-8 million barrels of oil consumption.

The impact is profound and a first for the energy industry: wind and solar now eat into the duopoly of gas and coal in the global power system, and in turn rapidly cleaner electricity leaps the barrier into the monopoly of oil in the transport system – at scale and at high speed.

And so – Are we winning?

As stated at the outset we need to define our terms.

For Carbon Tracker – the “we” is the global population at large.

There are many categorisations of this: Global North and Global South a popular structure; OECD, non-OECD another framing.

But “we” are all in this together.

The climate is “our” planetary climate: climate does not know boundaries or state-lines, it works with and confronts us all.

We all have a major stake in climate’s future, as it does with ours – which is the primary focus and aim of Carbon Tracker’s goals.

And so to the question are we winning?

“Winning” of course goes well beyond Carbon Trackers specific goals and aims – we have always seen ourselves as part of a much wider network and combined mission of civil society, governments, corporations and consumers plus other stakeholders such as partnerships and policy fora.

“Winning” is therefore the large-scale goals.

We started with noting we have via the climate countdown clock only six years or so to meet the precise carbon budget requirements to ensure we limit climate damage to 1.5°C above pre-industrial levels.

But we have shown the massive scale of new clean manufactured-scale technologies that are replacing fossil fuels at constantly fast-growing rates.

In our annual report we detail the various impacts Carbon Tracker has produced across multiple sectors via reports, engagements, policy fora and communications aligned with the themes and issues above.

What do we therefore conclude about winning ?

In the sense that the world now understands the risks of climate, has a variety of affordable large-scale new technology options and has informed and communicated with various stakeholders and commented on their positive and negative contributions – we propose we are winning: the state of play in the energy transition is there to digest and to participate in.

We have pathways, policies, technologies and options to avoid the worst consequences of climate disruption, and as importantly create a cheaper, cleaner, fairer and safer multi-generation energy system, allowing us to leave all the jeopardy and perils of the existing fossil fuel system behind.

And as noted above, our stranded asset theory of change has now started to accelerate the exit of oil and gas investment from long-term risky fixed production assets and into short-term financial restructuring, avoiding significant future emissions.

In the precise winning definition of will we avoid 1.5°C warming and stay within the best estimate of the carbon budget remaining and not run down the Climate Clock – six years and counting – this is a higher bar.

But.

We should not exclude this higher target: we have the tools and knowledge to accelerate the inevitable transition.

Carbon Tracker’s role has always been to actively shape our energy reality with ideas and analysis, not passively report on the outcomes.

We will continue to do this via the actions we detail in our report, and in all our upcoming activities and initiatives which will constantly be updated to achieve the energy transition targets we have all set ourselves.

Never exclude success and winning as an outcome: let us all get to work.

The transition continues at pace.