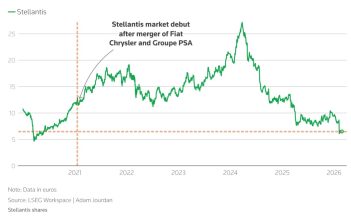

Stellantis group – a major global car manufacturer announced in February 2026 a $24billion loss in 2H 2025, related to massive write-down on its EV investments.

Its share price is now down roughly 80% from its 2024 peak. And it also noted there will be no dividend this year.

The explanation? The company “overestimated the pace of the energy transition.”

Translation: the market / consumer moved too slowly.

This is a familiar refrain from incumbent European manufacturers – the targets are too aggressive, consumers are hesitant, policy is misaligned. Slow the transition, and profitability returns.

But the market reality says otherwise.

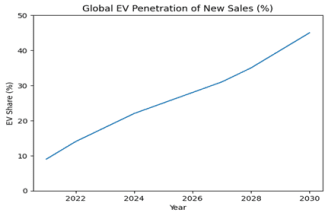

Global EV penetration is around 25% of new sales in 2025 and plausibly heading toward 35–45% by 2030. That is not a stalled market. That is a compounding structural shift.

Note 2026-2030 estimates, BNEF, IEA

Stellantis’ BEV mix sits in the mid-single digits (c.6–10%). It is underweight the fastest-growing segment of its own industry.

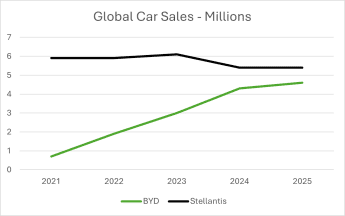

Meanwhile, BYD – often still dismissed as a “Chinese government funded manufacturer – has grown from ~0.7m vehicles in 2021 to roughly 5m in 2025. That is a ~50% CAGR. It now rivals or exceeds major Western incumbents in volume.

BYD is not a subsidy story anymore – and as Stellantis is finding out it is hazardous and very expensive to avoid focussing on the pace of industry change and business model of new entrant competitors.

BYD is vertically integrated in batteries, scales electrified platforms at cost, and is exporting aggressively into Europe, Latin America and Southeast Asia. Its growth reinforces battery learning curves and manufacturing leverage.

A model that traditional carmakers have not been able to follow due to increasingly stranded legacy capital assets and corporate engineering skills.

BYD is scaling into the new cost curve. Stellantis is defending legacy ICE exposure while hoping hybrids will cushion decline.

But hybrids, unless fundamentally differentiated, often cannibalise existing models rather than create new profit pools.

Source – BYD / Stellantis

A century ago, the Ford Model T triggered an explosion of automakers. Most disappeared as scale economics and capital intensity reshaped the industry. Chrysler survived that first cull and now sits within Stellantis.

The question is whether this is a separate episode – or the second great consolidation of the auto industry.

For Stellantis, the write-down does not signal a collapse in EV demand; it signals a widening cost gap with dominant Chinese EV car firms.

Growth is increasingly concentrating in electrified platforms where vertically integrated players such as BYD have scale and battery cost advantages. Stellantis remains exposed to legacy ICE capacity, and therefore to the large costs of rapid change.

The core investor issue is whether Stellantis can close the structural cost gap without destroying further capital. That looks increasingly unlikely.