A key tipping point was reached in 2019. Global demand for fossil fuels peaked and is unlikely ever to recover to its pre-crisis levels. The consequences are extremely profound for energy companies, financial markets and policymakers.

At heart, this is a technology transition. Look around you at the impact of the internet on the media sector or Amazon on the retail sector to get a sense of how rapid and profound are the impacts of a technology transition. The key driver of the transition in the electricity sector has been the collapse in the price of renewable energy technologies. The price of wind and solar electricity has fallen by up to 90% in the last decade. Most importantly, solar and wind electricity prices are at levels below that of fossil fuel-based electricity in 80% of the world and continue to fall. At the same time, engineers and innovators have been coming up with new ways to incorporate an ever-rising share of variable renewables into electricity systems. In 2019 three quarters of new investment in electricity went into renewables, the utilisation rates of coal generators fell to 53%, and fossil fuel demand for electricity fell by 1%.

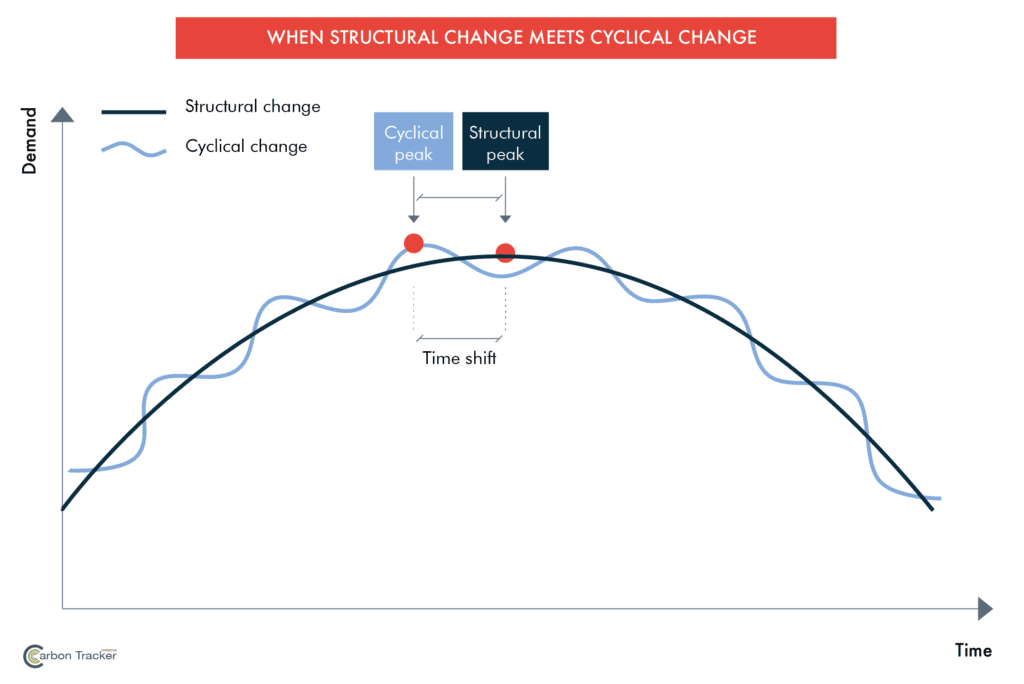

And then came the COVID-19 pandemic. According to the IEA, demand for fossil fuels is likely to collapse in 2020 by 8% at the same time as renewables keep on growing by 15%. By the time electricity demand recovers, all of the growth will be taken by renewables. What happens when you reach the top and start to decline? Companies that plan for growth have too much capacity. Excess capacity leads to low prices, which reduce profits for companies across the systems and leads to huge amounts of stranded assets. There is a huge legacy fossil fuel system with over $30 trillion USD of fixed assets, and thousands of companies whose business plan is based on rising demand. And yet this is all vulnerable to disruption as you move from growth to decline.

Infrastructure and generation plants last for decades. As investors realise that the era of business as usual is over, so they decide not to invest in the continued expansion of the legacy fossil fuel system. The impact is felt immediately if you are a company which builds new machinery for coal plants or offshore oil exploration platforms.

Financial markets are well aware of what is going on and are exiting the most vulnerable parts of the fossil fuel system. The European electricity sector collapsed in value in 2008 and spent the next decade in massive sector restructuring and the write-down of $150 billion USD of fixed assets. General Electric’s gas turbine division took a $23 billion USD write-down in 2018 as the share price of the company fell by two thirds. Coal stocks have been falling since 2011, two years before coal demand peaked. Business models based on high power plant utilisation rates and inflexible baseload provision are not needed in this environment. The companies who are feeling the shock are those that refused to accept the pace of change or are incapable of adjusting their technologies and business models to meet the energy transition.

The key hope of the incumbent fossil fuel companies was that the intermittency of renewables would be too hard for power systems to handle and somehow put a cap on their growth. They said this at 2% renewable penetration, again at 10%, and have kept on making the same argument in spite of the ever-rising share of renewables in the electricity system. In 2019, variable renewables supplied 8% of global electricity and 28% in Germany. In 2020 they have risen at times to supply over 50% of German electricity.

The solutions are complicated. They require demand and supply flexibility, new regulatory structures, new technologies and new ideas. Everywhere is different. And this is where Wärtsilä’s Atlas of 100% Renewable Energy is so important, to give direction to help to envision and enact the ultimate end-state for energy systems around the world in the most cost-optimal way.

What does this peak mean for policymakers? It would be deeply irresponsible to try to build back the old system. You may be certain that if you try to do so, the companies at the top end of the cost curve will dump their assets on the taxpayer, and you will have to pay to clean them up and close them down. As you stimulate to drive economic growth, then invest in industries like solar, wind or electric vehicles, and flexibility to keep the lights on in all weather conditions. Invest in efficiency and clean up our cities. Now is precisely the moment to forge the industries of the future, to invest in the new areas which will create jobs, opportunity and growth. Business as usual is well and truly over.

This blog was included in the report Aligning Stimulus with Energy Transformation by Wärtsilä Energy.