Calls to expand North Sea drilling re-emerge with every energy price spike. But the case for drilling as an energy security response is increasingly out of step with the system it claims to protect.

Gulf tensions have, once again, pushed oil prices higher and raised gas price risk. Within weeks of another price surge, the same narrative dominated much of the commentary: the UK is sitting on “still huge” domestic reserves; energy security must be treated like defence; and the answer is to drill.

The instinct to take energy security seriously is right. But the conclusion has several problems. The first is pricing.

Domestic production and domestic price protection are different things

Oil and gas are internationally traded commodities, and that single fact is central to this debate. Whether a molecule is extracted from a platform west of Shetland or delivered through an LNG terminal on Teesside, the price it fetches is determined on world markets – in Rotterdam, in Singapore, at Henry Hub. UK consumers remain exposed to the same global price swings regardless of the origin of supply, and no volume of additional domestic production changes that exposure. This is why additional drilling cannot function as a price shield. A more durable approach is to reduce exposure to globally priced fuels by accelerating the system already replacing them: one running increasingly on British wind, British daylight, and British engineering. In the near term, scaling system flexibility – including battery storage – can also reduce the need for gas at peak times and limit the transmission of gas price spikes into electricity bills.

A maturing basin on a long timeline

New field development in a mature basin like the North Sea often takes five to ten years from approval to first production – long-cycle investments responding to short-cycle shocks, with an obvious mismatch between the two. The basin’s remaining reserves are also late-life and high-cost, dependent in many cases on generous tax treatment to proceed at all. Projects routinely presented as Exchequer revenue generators can deliver minimal net contributions once incentives are factored in, and in some cases may be negative. And even under optimistic industry projections, North Sea output continues its structural decline; new projects reshape the slope of that decline without fundamentally altering its direction.

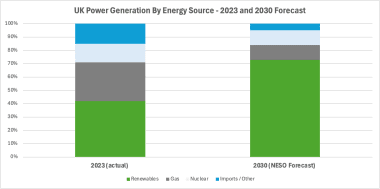

The power shift matters more than new drilling

All of which matters rather less than the more fundamental shift already underway in how the UK generates electricity. Central projections put renewables at around three-quarters of UK power generation by 2030 – a trajectory driven by build rates already in progress, not by policy aspiration. As that share rises, gas moves from primary generation source to residual balancing function, called upon less frequently and for shorter periods. Any new North Sea development sanctioned today would arrive into a market where gas demand in power has already fallen substantially, where cheaper alternatives have taken much of the space it once occupied, and where the infrastructure of the old system is being steadily repurposed around it.

The chart illustrates the expected shift towards renewables by 2030 under a median forecast, with gas moving from a central price-setting role towards a more residual balancing function. Source: https://www.gov.uk/government/publications/clean-power-2030-action-plan/clean-power-2030-action-plan-a-new-era-of-clean-electricity-main-report#our-pathway-to-2030

Gas as the driver of electricity price volatility

The less visible dimension of this shift concerns how gas currently shapes electricity prices across the whole system. Even as a minority source of generation, gas-fired plants set the marginal price of electricity – meaning that when gas prices spike, bills follow, regardless of how much wind and solar happens to be generating at the same moment. The connection runs through the market’s pricing architecture rather than through the physical share of gas in the mix, which is why periods of high renewable output have not historically translated into stable consumer prices in the way one might expect.

As renewables progressively displace gas from the system – pushing its share of generation below the threshold where it routinely sets the marginal price – that dynamic weakens. The exposure to imported gas price volatility that has defined UK energy bills for the past decade begins to recede with it. Official projections suggest the UK could become a net electricity exporter by 2030, from a position of importing 5-10% of its power today: a marker of how quickly the underlying supply arithmetic is changing.

A diversified supply cushion, and a shrinking need to use it

The UK already draws on domestic production, Norwegian pipeline imports, and global LNG –a supply base diversified enough to weather considerable disruption. What is changing is not the adequacy of that supply but the volume the system requires from it, which is falling as electrification and renewables reduce the economy’s gas intensity. Expensive new North Sea developments add cost and extend the lifespan of infrastructure at the precise moment the transition is being engineered to reduce dependence on it; they risk extending exposure to fuel price volatility without materially improving price protection or system resilience.

Reflex and strategy are not the same thing

Treating each price spike as evidence that more drilling is needed reflects a set of instincts formed in an era when gas supply and energy security were genuinely synonymous, and when the North Sea was a growth basin rather than a mature one in long-term decline. Those instincts have outlasted the conditions that made them sensible. Each new development sanctioned under their influence can lock in gas dependency for another fifteen to twenty years – sustaining exposure to the very price volatility that prompted the call for more drilling in the first place.