Key Resources

Summary report

Infographic

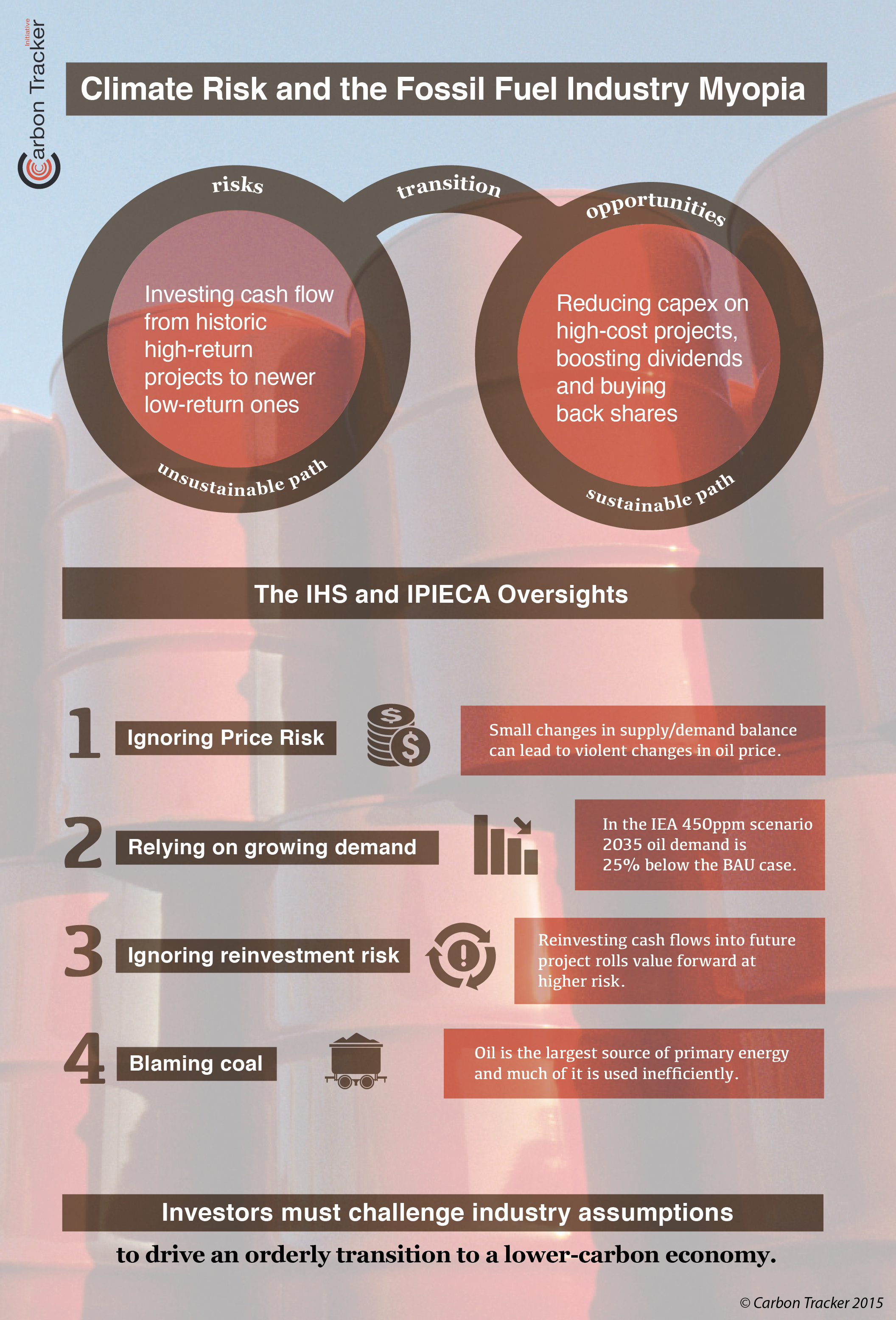

Climate Risk and the Fossil Fuel Industry Myopia

Read MoreDuring 2014, following in the footsteps of Shell and ExxonMobil, oil and gas industry association IPIECA published a “fact sheet” called “Exploring the concept of ‘unburnable carbon” in June and energy consultancy IHS Herold released a special report in July (dated September) titled “Deflating the ‘Carbon Bubble:’ Reality of oil and gas company valuation”.

We believe that these reports are complacent about the future for oil and gas, and understate the risks to industry business models.

Key Findings

Ignoring Price Risk:

IHS and IPIECA reports conclude that action on carbon emissions, although necessary, is unlikely to lead to much change in demand over the next 10-15 years. They assume that proven reserves are at little risk from policy changes. But the greatest threat to the industry comes from oil price changes impacting the cash flows coming from proven reserves. As we have seen in late 2014 (and 1986 and 2008), even small shifts in the supply/demand balance can cause large and quick moves in oil prices, moves that oil majors have no hope of reacting to given their current business models.

Figure 1: Brent oil price compared to the S&P Oil & Gas Exploration and Production Select Industry Index (rebased)

Source: Bloomberg

Figure 2: Change in global demand for oil compared to oil price

Source: BP Statistical Review of World Energy 2013

Ignoring Reinvestment Risk

The industry’s proven reserve base might appear low risk – as the reports argue. But every dollar released from proven reserves that is reinvested into new resources merely shifts value forward, often by 10-20 years, transferring it to future projects which are at greater risk from market, policy and technology changes.

The World still needs Fossil Fuels

IHS and IPIECA argue that decline rates mean the world will continue to need new oil and gas projects. True, but if meaningful climate action is taken, it will need far less. The IEA 450ppm scenario sees 2035 oil demand 25% below the business as usual case. This means fewer new projects – and hence less capital investment.

Figure 3: IEA oil demand projections – 2035 demand of 101 MBPD (New Policies Scenario) vs. 78 MBPD (450 Scenario)

Note: Calculations of 2012-2035 Delta (i.e. absolute change) and CAGR assume original WEO 2013 value for 2012 world oil demand of 87.4 MBPD (rather than the IEA’s more recent 2012 estimate of 90.1 MBPD)

Source: IEA, Carbon Tracker’s analysis 2014

Blaming Coal

Oil is the largest source of primary energy. Carbon Tracker agree that action is needed on coal but believe oil is an easier target for efficiency. Personal transport is inherently inefficient; just because action on coal is crucial does not mean that oil gets a free pass.

Key Takeaways:

- Carbon Tracker’s “Carbon Supply Cost Curve” analysis has focused on the break even prices of high cost capital expenditures and why these can potentially become wasted capital in a demand constrained world.

- IHS and IPIECA have taken this into what we see as a narrow focus of the implications for proven reserves and short term company valuations.

- In response, we have shown that whilst the majority of a company’s NPV may be due to near-term (the next 10-15 years) cash flows from proven reserves, if these cash flows are recycled and invested in new future production then the value is simply rolled over with greater risk.

Figure 4: Shell NPV profile by period (HSBC estimate)

Source: HSBC 2012 estimate, proven and probable projects

Further, even using the IHS approach of no reinvestment and looking at current proven reserves only, deterioration in the oil price driven by expectations of future demand weakness could cause cash flows to weaken and valuations to fall.

Key Action Points:

- We expect the transition towards a 2°C scenario to be driven by efficiencies, falling renewable energy costs and climate regulation, with or without a “global deal”. The impacts for fossil fuel company business models should be seriously considered.

- The key point is that, rather than diluting performance by investing cash flows from historic high-return projects into newer low-return projects, companies might improve returns and lower risk for shareholders by boosting dividends and buying back shares.

- Investors must question industry assumptions and challenge capital expenditure at the wrong end of the cost curve. It is not too late for the transition to a lower-carbon economy to be an orderly one, with fossil fuel companies steadily shrinking overall but delivering the best results for their shareholders by focusing on value rather than volume.