Key Resources

Event

Foot Off the Gas – UK Roundtable Virtual Event

Read MorePress Release

New UK gas power could derail climate targets and push up power bills

Read MoreItalian Report

Foot Off the Gas: Why Italy should invest in clean energy

Read MoreKey Quotes

Betting on new gas today means shouldering consumers with higher prices tomorrow as well as missing the net zero pathway the UK government has committed to.

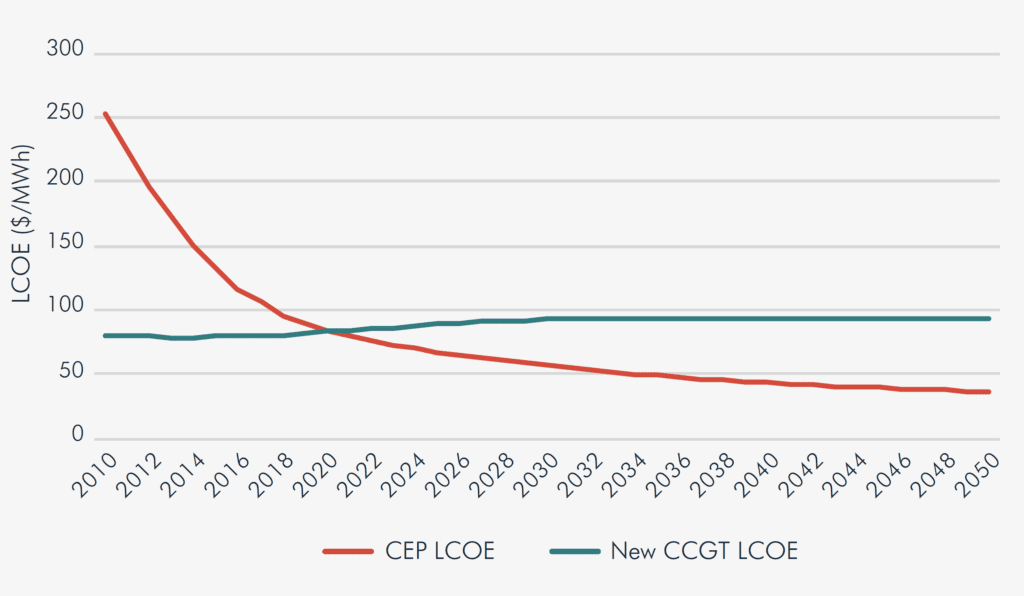

Clean Energy Portfolios are already cost competitive

In Foot of the Gas, we analyse the financial viability of new gas-fired power plants in the United Kingdom. We compare the cost of gas-fired power plants with those of a clean energy portfolio (CEP) providing the same grid services – monthly energy, peak capacity, and flexibility. These CEPs combine clean energy technologies, including onshore wind, offshore wind, utility-scale solar photovoltaics (PV), battery storage, energy efficiency, and demand response elements to provide the same grid services as gas-fired power plants.

Foot off the Gas finds that a CEP is already more cost competitive than new combined-cycle gas turbines (CCGTs) and offers the same grid requirements as gas plants i.e., a CEP will “keep the lights on”. Consequently, we find that investment in new CCGTs would not only be bad for emission goals but also lead to comparatively higher electricity prices and would result in a £9 billion ($13 billion) stranded asset risk.

Figure 1: CEP LCOE vs proposed CCGT gas plant LCOE

Source: Carbon Tracker analysis

Recommendations for investors and policymakers

Based on our analysis we see the following as important in avoiding potential stranded assets and helping the UK on its path to net zero by 2050:

1. Embrace coal-to-clean instead of coal-to-gas: new investments in gas capacity to partially fill any capacity gap left by the coal and nuclear phase outs will unlikely be a least-cost solution over the investment payback period. Importantly, our analysis highlights that a CEP is not only cheaper than new CCGTs but also offers equivalent grid services;

2. Reform the capacity market to ensure that gas is not disproportionately rewarded at the expense of other resources: this will ensure the grid does not overlook the least-cost option for the services required.

Key Findings

UK investment in new combined cycle gas plants for this decade would be misguided. Our analysis shows that a combination of clean energy sources and flexible technologies is not only cheaper than the 14 GW of slated new gas plants but also offers the same level of grid services. By investing in new gas, investors are exposing themselves to stranded asset risk of £9 billion ($13 billion). Annual emissions savings from forgoing new gas plants are also relevant at 24 million tonnes of CO2, equivalent to 7% of total emissions in 2019, enabling the UK to better meet its net zero emissions target by 2050.

The case for Clean Energy Portfolios (CEPs), a combination of clean energy sources and flexible technologies, is strong across different demand outcomes. We tested a model to manage peak and non-peak demand across the year and, although the contribution of the CEP resources changes, it is shown to be capable of providing the same grid services as a gas plant. We performed a cost sensitivity to key inputs to show that CEP economics are robust. We find that a 25% cost reduction in battery storage would bring the overall cost of a CEP down by 12%. Costs in a CEP are mitigated by the least-cost substitution which takes place unlike for gas, which is wholly exposed to gas prices.

The UK capacity market disproportionately incentivises and rewards new and existing gas power capacity. If the government wants the UK to be a world leader in green energy, which would support 60,000 jobs, it will need to level the playing field for all resources in future auctions, especially for demand side and storage technologies. Betting on new gas today means shouldering consumers with higher prices tomorrow as well as missing the net zero pathway the UK government has committed to.