Key Resources

Press Release

Taxpayers could be forced to pay tens of billions to close and clean up oil and gas wells in the Gulf of Mexico

Read MoreLaunch Webinar

Double or Nothing: Report Launch Presentation + Q&A

Read MoreInfographic

Key Quotes

The Gulf of Mexico has long been a major oil and gas producing region for the U.S., but field depletion in shallower regions near shore has driven development into deep and ultra-deep waters, driving up the cost to develop and decommission infrastructure.

Meanwhile, aging wells and platforms closer to shore — many of which are now owned by smaller operators — are increasingly marginal in value, raising the risk that they will be abandoned by their current operators.

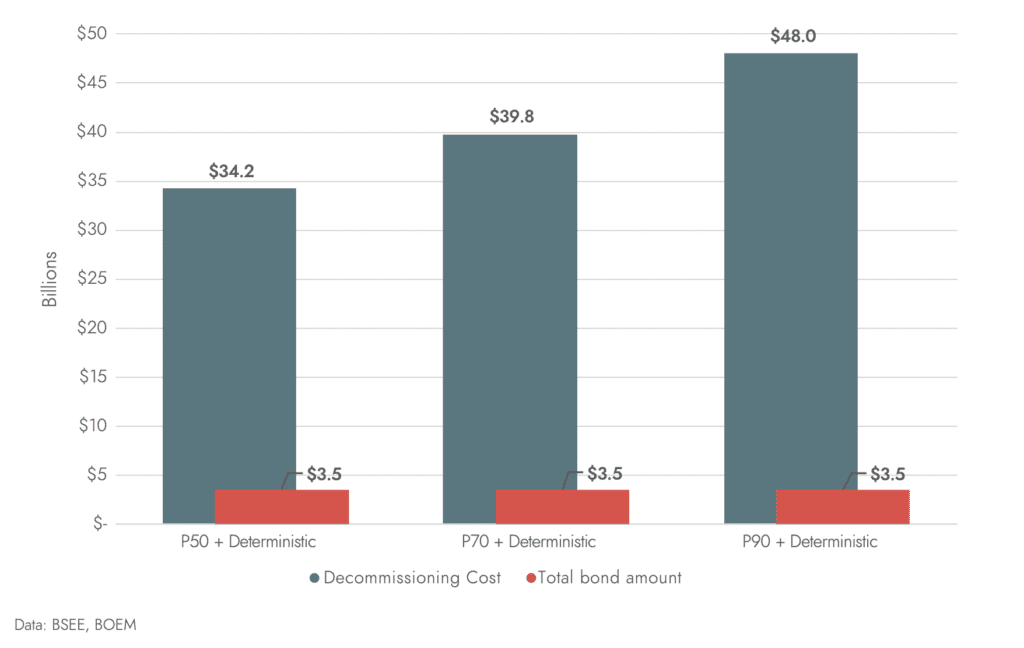

Double or Nothing finds that as the energy transition accelerates and oil and gas wells in the Gulf of Mexico close, taxpayers may be forced to pay tens of billions in clean up costs. At best, only 10% of estimated decommissioning costs for the Outer Continental Shelf (OCS) are secured by bonds.

Figure 1: Total financial collateral vs. total estimated decommissioning costs, P50, P70, and P90 cost tiers

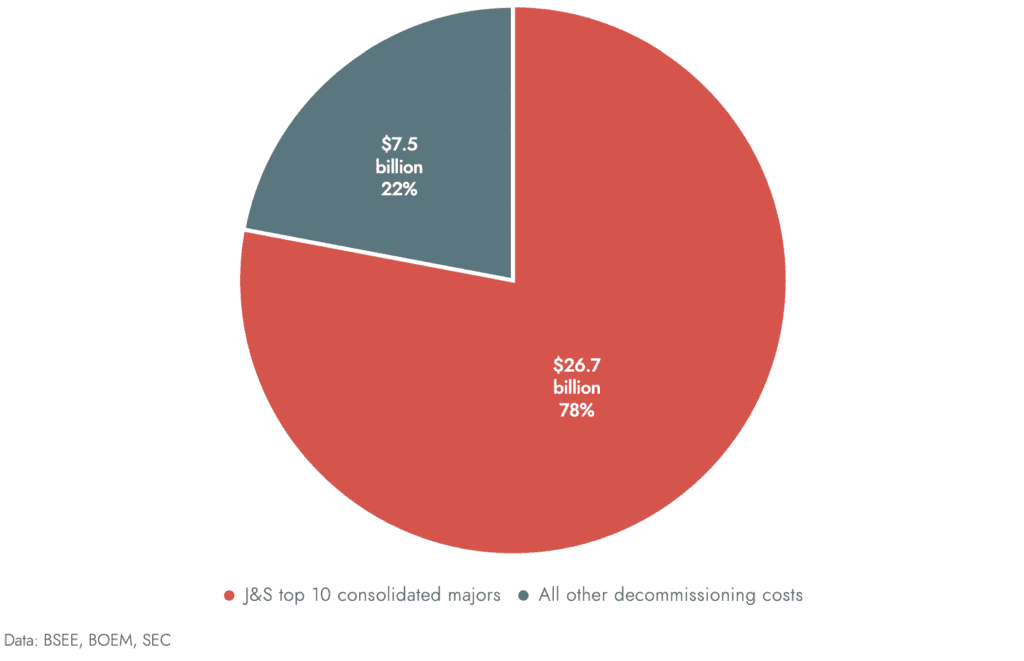

The report shows how 78% of the decommissioning costs in the Gulf are tied to the largest companies. On average only 1% of their costs are covered by bonds, meaning there is no cash in reserve to protect taxpayers if companies walk away from their cleanup obligations.

Figure 2: Share of total decommissioning costs linked by past or present lease or operating rights interest to the top 10 publicly traded companies operating in the GOM.

Key Findings

- Production on the Outer Continental Shelf (OCS) of the Gulf of Mexico (GOM) is moving into deeper water, where development and decommissioning costs are much higher. As the energy transition progresses, the risk that companies will be unable to pay their decommissioning costs will grow.

- At best, only 10% of estimated decommissioning costs for the OCS are secured by bonds (Figure 1).

- Bond coverage for the largest publicly traded exploration and production (E&P) companies in the GOM is only 1%, on average.

- The problem is, parent corporations are not, as a matter of law, liable for their subsidiaries and the major operators in the GOM are all subsidiaries.

- Federal regulators are heavily reliant on the future financial strength of large publicly traded corporations to ensure decommissioning obligations are not abandoned to the public.

- The 10 largest publicly traded companies operating in the OCS, as a group, are jointly and severally liable for 78% of total OCS decommissioning costs, amounting to at least $26.7 billion (Figure 2).

- Due to joint and several liability, the energy transition can be expected to consolidate decommissioning obligations of weaker firms in a few “last ones standing.”

- Whether parent corporations assume the decommissioning obligations of their subsidiaries, if and when called upon to do so, will be a matter of self-interest rather than law.

- Worsening economics combined with rising decommissioning costs will tilt the self-interest of large legacy operating groups towards avoiding decommissioning costs.

- If the last ones standing choose to back their subsidiaries, they could incur costs that are 2.3 to 6.8 times the amount of their direct liability on current leases, equivalent to billions in additional decommissioning costs for a given company. These costs are not generally reflected on balance sheets today.

- The U.S. Department of Interior should increase financial assurance requirements now to ensure that future decommissioning occurs on a timely basis at the expense of industry rather than taxpayers.