Key Resources

The energy transition is disrupting the entire fossil fuel system, with profound consequences for financial markets and geopolitics.

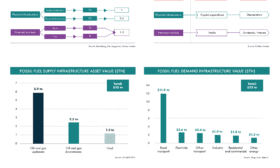

In this report, we calculate the size and vulnerability of the different parts of the system. We take a wider definition of the whole fossil fuel system, looking at stocks and flows, supply and demand, fossil fuels, infrastructure and financial markets.

![]()

Source: Bloomberg, IEA, Tong et al., Carbon Tracker

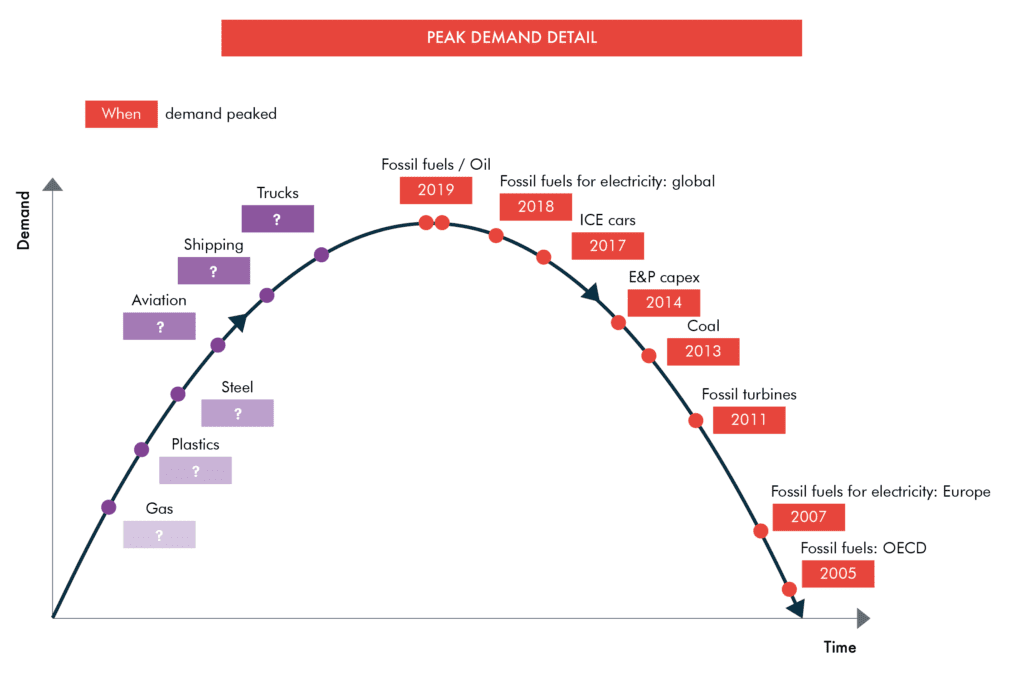

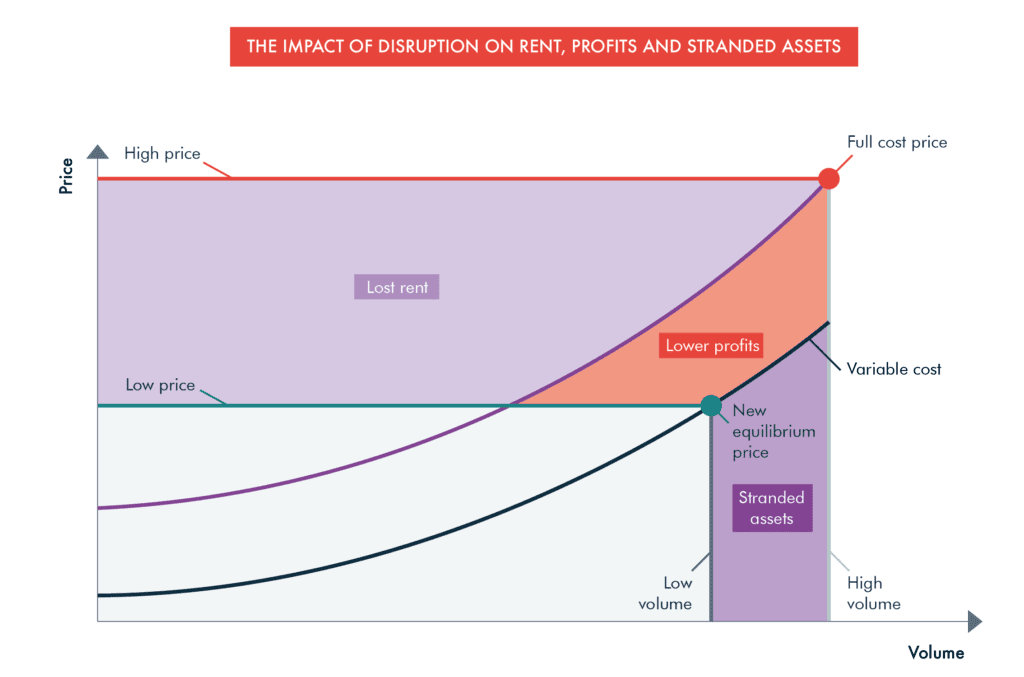

The forces of disruption in the fossil fuel system

The fossil fuel system is being disrupted by the forces of cheaper renewable technologies and more aggressive government policies. In one sector after another, these are driving peak demand, which leads to lower prices, less profit, and stranded assets. The COVID-19 crisis is now accelerating this.

Our analysis finds falling demand, lower prices and rising investment risk is likely to slash the value of oil, gas and coal reserves by nearly two thirds, increasing the risk and likelihood of stranded assets. The four main consequences of lower prices, as highlighted in the chart below, are:

- Lower rents. As the chart shows, the largest quantum of change is the fall in the amounts of rent. This means less money for the governments of petrostates.

- Lower profits. Profits fall not just for the high cost companies, but right across the system.

- Totally stranded assets. When prices fall below variable costs, you have totally stranded assets.

- Lower capex. As companies struggle to survive and figure out that growth is over, so they reduce their capex.

The decline of the fossil fuel economy poses a significant threat to global financial stability. The report warns investors there is far more risk in the fossil fuel system than is conventionally priced into financial markets. Investors need to increase discount rates, reduce expected prices, curtail terminal values and account for the clean-up costs.

For policymakers, the implication is the urgent need to put in place an orderly wind-down of assets rather than trying to rebuild the unsustainable.

Carbon Tracker has been writing for many years about which areas are most at risk from the energy transition. We have focussed on different areas of supply and demand for existing and new assets, over separate timescales, and the conclusions of that analysis are incorporated into this report.

We provide a framework within which to think about the energy transition so that the impact on each of the pieces can be better understood.