Investors warned that Asian governments’ plans for 600 new coal plants could waste $150 billion

LONDON/NEW YORK, JUNE 30 Five Asian countries are responsible for 80% of the world’s planned new coal plants, endangering Paris climate goals despite the availability of cheaper renewables, finds a new report Do Not Revive Coal from the financial think tank Carbon Tracker published today.

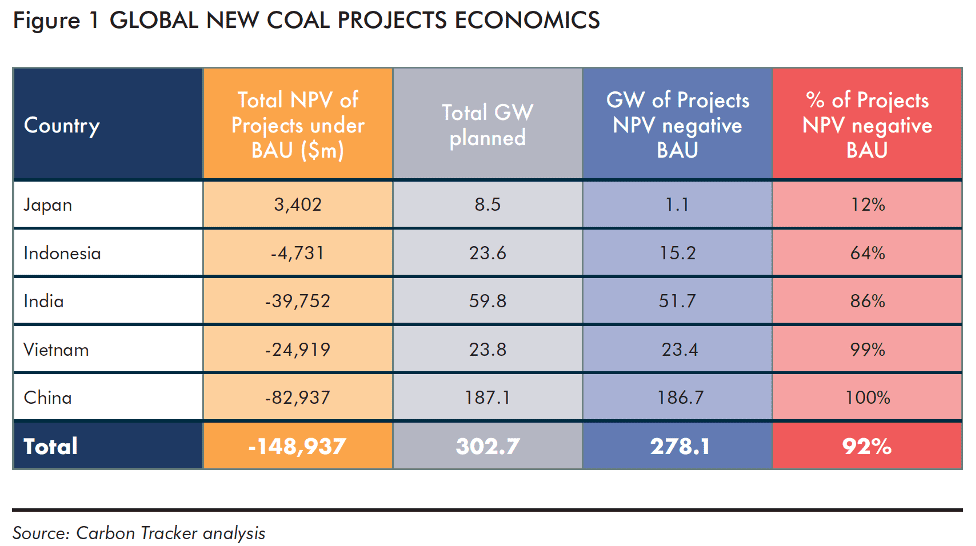

China, India, Indonesia, Japan and Vietnam plan to build more than 600 new units with a combined capacity of over 300GW, ignoring calls from UN Secretary General Antonio Guterres for all new coal plants to be cancelled. He said phasing out coal from the electricity sector is the “single most important step” in tackling the climate crisis. [1]

The report warns that 92% of these planned units will be uneconomic, even under business as usual, and up to $150 billion could be wasted. Consumers and taxpayers will ultimately foot the bill because these countries either subsidise coal power or prop it up with favourable market design, power purchase agreements or other forms of policy support.

“These last bastions of coal power are swimming against the tide, when renewables offer a cheaper solution that supports global climate targets. Investors should steer clear of new coal projects, many of which are likely to generate negative returns from the outset.”

Said, Carbon Tracker’s Head of Power & Utilities, Catharina Hillenbrand Von Der Neyen.

As well as modelling the financials of 80% of planned new coal, Do Not Revive Coal evaluates the economics of 95% of operating coal plants at the boiler level worldwide: over 6,000 operating units accounting for around 2,000 GW. It is the third report in Carbon Tracker’s annual Powering Down Coal series.

The same five Asian countries also operate nearly three quarters of the current global coal fleet, with 55% in China and 12% in India. The report warns that around 27% of existing capacity is already unprofitable and another 30% is close to breakeven, generating a nominal profit of no more than $5 per MWh. Worldwide, $220 billion of operating coal plants are deemed at risk of becoming stranded if the world meets the Paris climate targets.[2]

The report finds that around 80% of the operating global coal fleet could be replaced with new renewables with an immediate cost saving. By 2024, new renewables will be cheaper than coal in every major region, and by 2026 almost 100% of global coal capacity will be more expensive to run than building and operating new renewables.

Growing competition from renewables, coupled with increased regulation, is likely to drive continued falls in coal plant usage, undermining their profitability. The report notes that coal plant economics are highly sensitive to utilisation and just a 5% annual reduction to the conservative base assumptions in its analysis would see global coal unprofitability almost double to 52% by 2030 and rise to 77% by 2040.

COUNTRY SNAPSHOTS

- China is the world’s largest coal power producer with 1,100 GW of operating coal capacity and a pipeline of 187 GW. However, new solar and wind could already generate energy at lower cost than 86% of this capacity and by 2024 they will outcompete everywhere. China has led the global roll-out of renewables 530 GW of installed capacity and a target of reaching 1,200 GW by 2030[3]. At current rates of build this target could be achieved in under six years.

- India is the second largest coal power producer with around 250 GW of operating capacity and a pipeline of 60 GW. New renewables can already generate energy at lower cost than 84% of operating coal and will outcompete everywhere by 2024. It has a target of 450 GW of renewables by 2030 – more than five times its 2020 capacity – which will would meet 60% of energy demand[4].

- Japan has 45 GW of operating coal capacity with 9 GW in the pipeline. Renewables are already cheaper than new coal and will be cheaper than existing coal by 2022, despite being hampered by lack of land, capacity market payments favouring fossil fuels, and grid constraints[5]. The government has committed to no longer supporting foreign coal projects[6].

- Vietnam has 24 GW of operational coal power, with a further 24 GW in the pipeline. New renewables will outcompete existing coal units in Vietnam by 2022.

- Indonesia is heavily reliant on thermal power most of which (45 GW) comes from coal, with 24 GW of new coal planned. New renewables will outcompete existing coal by 2024.

“Coal no longer makes sense financially or environmentally. Governments should now create a level playing field which allows renewables to grow at least cost, using post-COVID stimulus spending as an opportunity to lay the foundations for a sustainable energy system.”

Continued Catharina Hillenbrand Von Der Neyen.

However, the silence from large polluting countries, including China and India, on more aggressive climate measures at the recent Leaders Summit on Climate spoke volumes, suggesting they still have internal priorities that conflict with policies that seek to mitigate climate change.

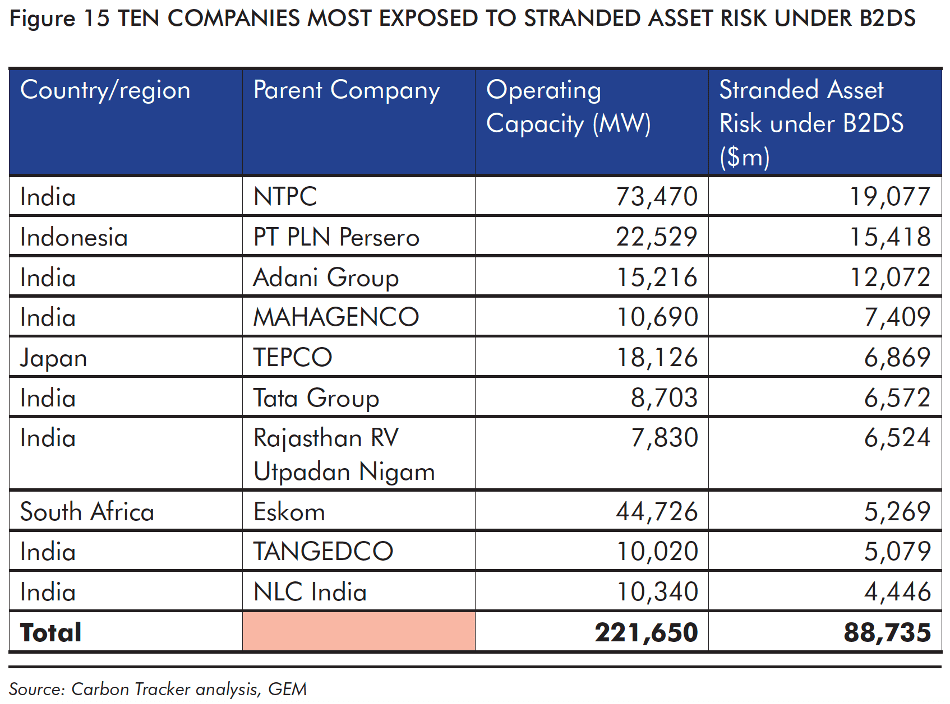

At the corporate level, just ten companies account for around 40% of the stranding risk, of which NTPC and the Adani Group in India, and PLN in Indonesia are by far the most exposed. Of the ten most exposed companies, seven are head quartered in India.

METHODOLOGY

Carbon Tracker’s Global Coal Power Economics Model (GCPEM) is a proprietary techno-economic simulation model which covers ~95% of operating, under-construction and planned coal-fired capacity.

Carbon Tracker uses publicly available information to estimate revenues from wholesale power markets and out-of-market sources such as ancillary and balancing services and capital markets. This does not include hedging.It assesses operating cashflows by deducting the cost of running each coal plant, taking into account fuel, maintenance and existing or ratified carbon pricing and air pollution policies.

It uses coal fuel price data from Bloomberg and coal capital costs from the International Energy Agency and Carbon Tracker.

Our stranded cost risk model compares three tipping or inflection points that will make coal-fired power economically obsolete (i) when new renewables outcompete new coal; (ii) when new renewables outcompete operating existing coal; and (iii) when new firm (or dispatchable) renewables outcompete operating existing coal.

Once embargo lifts the report can be downloaded here: https://carbontracker.org/reports/do-not-revive-coal/

ENDS

To arrange interviews please contact:

Joel Benjamin | jbenjamin@carbontracker.org.uk | +44 7429 637423

Stefano Ambrogi | sambrogi@carbontracker.org | +44 7557 916940

David Mason | david.mason@greenhousepr.co.uk | +44 7799 072320

About Carbon Tracker

The Carbon Tracker Initiative is a not-for-profit financial think tank that seeks to promote a climate-secure global energy market by aligning capital markets with climate reality. Our research to date on the carbon bubble, unburnable carbon and stranded assets has begun a new debate on how to align the financial system with the energy transition to a low carbon future. www.carbontracker.org