NEW NGFS SCENARIOS REPRESENT PROGRESS ON CLIMATE RISK IMPLICATIONS FOR FINANCIAL INSTITUTIONS, BUT NEED TO GO FURTHER TO CAPTURE THE FULL EXTENT OF FUTURE CLIMATE DAMAGES

On 5 November 2024, the Network for Greening the Financial System (NGFS) published “Phase V Climate Scenarios,”[1], in which it has significantly increased its estimate of the future economic costs of climate inaction.

The NGFS now estimate climate damages could result in economic losses amounting to 15% of global GDP by 2050 from 2°C of warming and 30% by 2100 from 3°C. The new damage estimates are three times larger than earlier NGFS assessments.

However, the new estimates still assume strong economic growth will continue, and indeed increase in future, despite high levels of global warming. The high GDP growth assumptions inherent in the NGFS models are somewhat ironic, given the Trump administration’s decision to withdraw the U.S from the NGFS on 30 January 2025, citing supposed: “inconsistency with the administrations priorities to grow the U.S economy & jobs.” [2]

The Trump Administration has further threatened to privatise NOAA, slashing 600 jobs at the weather agency which houses expert climate and ocean scientists, & collects publicly available climate and weather data, in a move which threatens to undermine the US weather warning system, and complicate efforts to track mounting climate-related damages.

A 15% fall in global GDP by 2050 converts to an annual decline of 0.62% in growth between 2025 and 2050; a 30% fall by 2100 converts to a fall of 0.35% p.a. Given that the global economy has grown by roughly 3% p.a. since 1960[3]. This suggests that the NGFS (via SSP2) expects the global economy to continue to grow by on average 2.65% per year, as global temperatures rise to 3°C above pre-industrial levels by 2100 and climate chaos accelerates.

Despite their revised estimates, it is still very hard to reconcile the new NGFS climate scenarios with the strong consensus among climate scientists that 1.5°C of warming is “dangerous” and that 3°C would be “catastrophic”.[4][5][6] In short, although an improvement on its predecessors, the NGFS is still way behind the curve with scientific literature on global warming, in ways that drastically underestimate the economic dangers of climate change, as illustrated by recent destructive Los Angeles wildfires, with the full effects of the 1.5C warming breach (2024)[7] yet to materialise.

Whilst Carbon Tracker welcomes the NGFS’s renewed focus on this critical issue, which will improve the robustness of stress testing for financial institutions, key failings include:

- It assumes that damages will be smooth and gradual, by using a “damage function” that describes damages as being proportional to the temperature change squared, when other functions which fit the data equally well generate significantly larger damages. Gradual, smooth change is only possible if critical tipping points are not triggered in the analysis – an implausible scenario, when the scientific literature clearly asserts that they will be triggered between 0.8-3°C of warming.

- It ignores climate tipping points, when the latest scientific research concludes that several critical components of the climate could be tipped into fundamentally different states by between 0.8°C and 3°C of warming. These include: (a) the Atlantic ocean (AMOC) circulation system, which scientists now estimate has a threshold of just 1.1°C, and which could tip in the next 50 years. This would make northern Europe uninhabitable, and could trigger a global famine via a fall of approximately two-thirds in potential wheat and corn output;[8] and (b) the Greenland, West Antarctic and Marine East Antarctic ice sheets, which could collectively increase global sea levels by up to 29 metres over the next few centuries.[9]

- As with all other economic studies, it uses data on GDP and climate over the last 40 years, and extrapolates the relationships found in this data forward over the next 75 years.[10] If there is one thing we can be confident of with climate change, it is that the future will (sadly) not be a mirror of the past. Future economic performance is subject to major uncertainties, being exposed to social[11] and nature-based tipping points as the climate destabilises

- The GDP data should have been corrected to exclude the gains from trade. Warm regions of the planet can trade with cold regions today. But a future hot Earth cannot trade with today’s warm Earth – as economists models infer[12].

- Continued use of equilibrium models, which fail to consider investment opportunities and benefits of transition, and discourage deviation from investment benchmarks.

One implication of the reliance on equilibrium models relevant to Carbon Tracker’s work on fossil fuels involves the NGFS V5 scenario assumption that oil and energy prices will remain high and increase in future through the energy transition, even as exponential renewables growth in the energy system, and rapid EV adoption in the transport system drive down oil demand and spur electrification. By contrast, other forward looking scenarios including the PRI commissioned Inevitable Policy Response (IPR)[13] assume a ratchet effect where as physical climate damages increase, so too does policy ambition to increase the pace of decarbonisation and fossil fuel phase out, with lower oil demand resulting in lower oil prices.

Carbon Tracker’s Head of Oil and Gas Mike Coffin said “Under scenarios where oil consumption falls sufficiently fast to limit warming to within Paris Agreement goals, we expect long-term oil prices to fall. Accordingly, we find the results of the NGFS modelling – where oil price rises under all scenarios – very surprising. This raises serious concerns about how the interactions between different sectors are captured within the modelling.”

These flaws in its methodology allow the NGFS to present a more palatable picture of relatively minor physical economic damages from global warming – in stark contrast to the more alarming, and more scientifically plausible assessment of accelerating[14] and potentially catastrophic[15] damages.

In plain language terms, there’s an Orwellian dimension to decreases in share prices and declining demand for fossil fuel energy firms being framed as transition risk, rather than transition necessity – with the enormous upsides for the biosphere and human society largely obscured by this framing.

Many climate scenarios analyses, such as that reproduced below for Gloucestershire LGPS by Mercer and MSCI[16] present damages in an annualised form, which has the effect of accentuating short-term volatility and losses associated with rapid transition (‘transition risk’), whilst obscuring the cumulative impacts of longer-term physical risk. Rather than a narrow focus on transition risk, which can be minimised by exiting non-aligned companies that lack viable transition plans[17], trustees should weigh the long term financial and social benefits of avoiding catastrophic levels of future warming, and ensuring a viable biosphere within which current and future generations can safely enjoy their retirement.

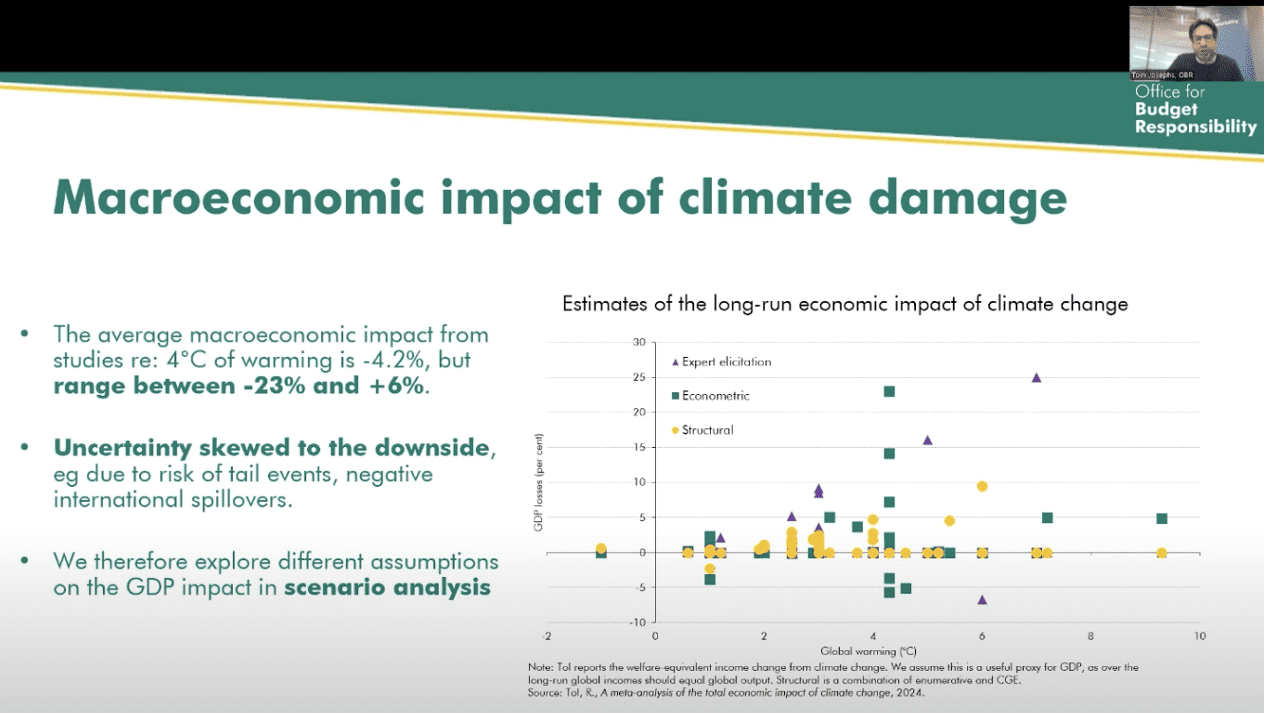

A presentation by The OBR and Green Alliance in December 2024 showed the average impact of 4˚C climate change in economic papers reviewed by the OBR resulted in just a 4.2% hit to economic output, illustrating the scale of the economic modelling problem.

We have spoken to experts who have looked in some depth at the climate scenario analysis used by the NGFS and their central bank members. Their comments are worth repeating.

Sandy Trust – of the Institute and Faculty of Actuaries noted in the January 2025 IFoA ‘Planetary Solvency’ report the NGFS approach is: “analogous to carrying out a risk assessment of the impact of the Titanic hitting an iceberg but excluding from our model the possibility that the ship could sink, the shortage of lifeboats, and death from drowning or hypothermia. The modelled results would be reassuring but dangerous as they would severely understate the level of risk.”[18]

Professor Steve Keen, author of Loading the DICE, said: “Science tells us that loss of the AMOC would result in catastrophic cooling in the Nordic countries, potentially threatening the viability of agriculture in northwestern Europe[19], and risking the loss of up to two-thirds of grain production[20]. In global terms, grain crops represent a small fraction of the 4% that agriculture contributes to global GDP. But this magnitude of a loss of such core food inputs would make it impossible to sustain a functional modern society.”

Thierry Philipponnat, Chief Economist at European nonprofit Finance Watch, said that, while he appreciated the transparency and leadership of the NGFS, they still need to account for sea level rises and other risks to ensure policymakers “have a clear view of the cost of climate inaction.”[21]

An update by Ortec Finance published September 2024 suggested: “investors should consider using climate scenarios that adopt a logistic damage function like approach as proposed by Carbon Tracker and the Institute and Faculty of Actuaries.

This approach captures stronger impacts compared to the quadratic approach, which tends to reflect the current, more optimistic views of economists on the severity of physical risk implications.”[22]

As highlighted in our report, Loading the DICE Against Pensions[23] we are particularly concerned about the underestimation of physical climate damages and the overestimation of the time available to address these issues – which provides a false sense of security to fiduciaries. Not only does it affect our collective ability to live within planetary boundaries, it also impacts the financial system, and the value of billions of ordinary people’s pensions and savings plans.

It should be remembered that it’s not just the deficient damage function that limits the effectiveness of general equilibrium models used by investment consultants and the NGFS.

Such models also fail to capture the benefits of energy transition in terms of investment opportunities in new emerging clean tech companies benefitting from rapid deployment.

Instead – equilibrium models portray rapid well below 2˚C transition as high tracking error from investment benchmarks – something pension fund trustees and asset managers are schooled to avoid.

Unless these models are subject to a fundamental overhaul, not evolution in design – they will continue to lock investors into high carbon business as usual investing and society into catastrophic levels of global warming.

This is why Carbon Tracker, Exeter University and Finance Watch are calling for a post-publication review of climate economists work estimating the future damages from climate change which is published in leading economic journals and used to calibrate IAMs – to ensure economic thinking, and the financial decision making upon which it is based aligns with climate reality.

Until more realistic numbers are generated by economists and plugged into the financial system and government policy making apparatus – climate action will continue to lag climate targets.

[1] https://www.ngfs.net/en/communique-de-presse/ngfs-publishes-latest-long-term-climate-macro-financial-scenarios-climate-risks-assessment-2024

[2] https://home.treasury.gov/news/press-releases/sb0003

[3] See https://data.worldbank.org/indicator/NY.GDP.MKTP.KD.ZG.

[4] Xu and Ramanathan 2017, p. 10315: https://www.pnas.org/content/pnas/114/39/10315.full.pdf

[5] https://www.politico.eu/article/united-nations-emissions-gap-global-warming-data-climate-change-report/

[6] https://www.theguardian.com/environment/article/2024/may/08/world-scientists-climate-failure-survey-global-temperature

[7] https://www.nature.com/articles/s41558-025-02247-8

[8] See OECD 2021, Managing Climate Risks, Facing up to Losses and Damages, p. 153: https://www.oecd.org/en/publications/2021/11/managing-climate-risks-facing-up-to-losses-and-damages_928fe20d.html

[9] See Lenton et al. 2023 The Global Tipping Points Report 2023: https://report-2023.global-tipping-points.org/, Table 1.2.1, p. 59-60, Table 1.3.1, pp. 81-85 and 1.4.1, pp. 125-127.

[10] See Kotz, Levermann and Wenz, “The economic commitment of climate change”, https://www.nature.com/articles/s41586-024-07219-0.

[11] https://www.exeter.ac.uk/research/tippingpoints/

[12] https://carbontracker.org/reports/systemic-under-pricing-of-climate-damages/

[13] https://www.unpri.org/sustainability-issues/climate-change/inevitable-policy-response

[14] https://www.eea.europa.eu/en/analysis/indicators/economic-losses-from-climate-related

[15] https://www.politico.eu/article/united-nations-emissions-gap-global-warming-data-climate-change-report/

[16] https://www.gloucestershire.gov.uk/media/3hjfjfed/tcfd-report-2023-24-gloucestershire-pension-fund.pdf

[17] https://carbontracker.org/reports/oil-and-gas-transition-plans-user-guide/

[18] https://actuaries.org.uk/document-library/thought-leadership/thought-leadership-campaigns/climate-papers/planetary-solvency-finding-our-balance-with-nature/

[19] https://en.vedur.is/media/ads_in_header/AMOC-letter_Final.pdf

[20] OECD 2021, Figure 3.20, p. 153 refer Loading the Dice Against Pension Funds 2023, Fig 4, p. 27.

[21] https://greencentralbanking.com/2024/11/13/economic-impact-of-climate-change-could-be-worse-than-anticipated-ngfs-says/

[22] https://www.ortecfinance.com/en/insights/blog/beware-how-financial-markets-are-pricing-in-climate-risk

[23] https://carbontracker.org/reports/loading-the-dice-against-pensions/