The European Central Bank (ECB) has announced plans to include climate impact into their monetary operations.

This announcement represents a momentous paradigm shift and had the potential to make a huge impact with the ECB’s €345 billion quantitative easing portfolio – but the announced plans do not go far enough.

MSCI recently published findings showing that, “corporate bonds had the highest total financed emissions,” namely, the ECB would be buying the bonds of some of the world’s biggest polluting companies, including fossil fuel companies, showing the importance of decarbonizing corporate bonds (MSCI, 2022).

However, ECB plans to only “tilt” its portfolio towards greener companies and away from fossil fuel producers, based on bond redemptions will not cut it for the energy transition. Instead, ECB ought to take a stronger stance if it truly wishes to decarbonize its portfolio and be in line with Europe’s Net Zero targets, thus, ECB should also include future net new purchases in its policy. ECB should also recognize that the reserves owned by fossil fuel companies cannot be used if we are to reach a 1.5 C degree scenario. If these reserves can’t be used, then the ECB shouldn’t be funding fossil fuel expansion plans aimed at increasing fossil supply.

Previously, the ECB operated with ‘market neutrality’, where bonds were purchased in proportion to the underlying markets. Since the European bond market is heavily tilted towards high carbon emitting firms in the utilities, infrastructure, and transportation sectors, ‘market neutrality’ resulted in over-exposure to these companies. Effectively, the ECB ended up providing cheap financing to fossil fuel companies at a time when the world ought to be coming off fossil fuels.

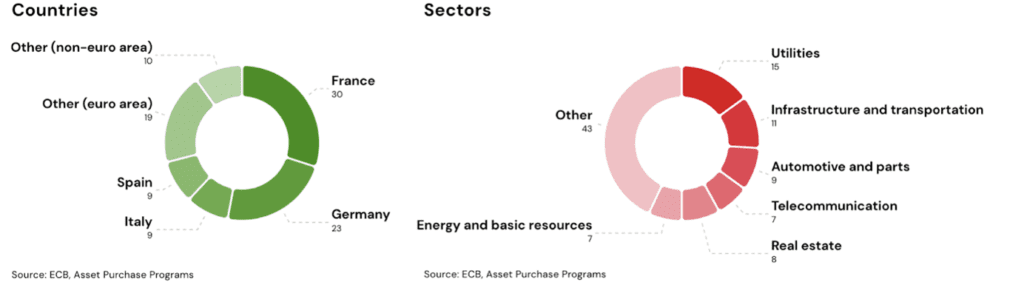

The ECB CSPP portfolio

At the end of Q1 2022, The ECB’s bond portfolio country exposures included France (30%), Germany (23%), Italy (9%) and Spain (9%). Sectors include 33% in Utilities, Infrastructure, Transportation and Basic Resources. The ECB publishes its holdings data but does not include the size of each of these holdings. It is believed that due to market neutrality, the ECB owns these bonds according to the size of issuance in the market.

The CO2 exposure of the ECB’s CSPP bond portfolio is concentrated in 20-30 issuers from carbon-intensive industries including fossil fuels, mining, manufacturing, and airlines. According to Anthropocene Fixed Income Institute (AFII), the top 25 high carbon issuers in the CSPP portfolio comprise 90% of the total footprint of the portfolio (AFII, 2022) highlighting the concentrated nature of its carbon footprint.

Today, the ECB’s plans include four measures to achieve the goal of Paris-Alignment. They will decarbonize current corporate bond holdings through reinvestment of redemptions. They will reduce the share of high carbon bonds pledged as collateral and will consider climate change risks when applying haircuts. They will require companies to comply with the Corporate Sustainability Reporting Directive (CSRD) from 2026 onwards. They will improve climate-risk tools and capabilities and will challenge ratings agencies on their methodologies of climate risks.

Most of these measures will come into effect from 2026 except for the tilting of their corporate bond portfolio towards climate-friendly names using redemptions, which will apply immediately. However, climate tilting of redemptions does not guarantee that future net new purchases of fossil fuel bonds will not take place. The ECB’s measures only affect redemptions, which is defined as the principal amount invested plus any interest owed. On average, this may be a reinvestment €1.8 billion/month into more climate positive companies. This is much less than the €8 billion/month that was spent via their QE Corporate Sector Purchase Program (CSPP) which ended in June 2022.

In addition, the measures that the ECB is using do not account for the carbon reserves that fossil fuel companies hold. According to Carbon Tracker, in order to limit warming to 1.5 degrees, “90% of fossil fuel reserves must stay in the ground as unburnable carbon” (Carbon Tracker, 2022). Fossil fuel companies in the ECB’s CSPP bond portfolio have vast fossil fuel reserves that have not been considered in evaluating the impact of their portfolio. These reserves must not be utilized if we are to stick to the Paris aligned temperature. The Corporate Sustainability Reporting Directive (CSRD) together with ratings agencies should recognize that fossil fuel reserves will not be utilized and may pose risks to bond investors. Unburnable carbon must be included if the ECB is to move its portfolio to carbon neutrality.

As the ECB diverts redemptions towards low carbon companies, they should commit to climate tilting future net new purchases and include fossil fuel reserves in their methodology. Without this, it is a feeble attempt. They ECB should also require companies to disclose the carbon potential of their reserves and use the data to inform their investment decisions.

If the ECB does not make a fundamental shift in its policy of funding fossil fuel expansion plans, it risks catalyzing climate disaster and in turn, being unable to maintain price stability in financial markets posing further risks to bond investors. It can’t be the intention of policymakers and regulators to facilitate climate failure.

References

Bank of England. (2021). “Greening the Corporate Bond Purchase Scheme”, BOE, 5 Nov 2021

Bloomberg. (2022) “Green European Credit Outlook and Review”, Bloomberg, 21 Jul 2022

Carbon Tracker, “Unburnable Carbon: Ten Years on”, Carbon Tracker, 23 June 2022

ECB. (2022). “ECB takes further steps to incorporate climate change into its monetary policy operations”, ECB, 4 July 2022

ECB. (2016). “What are haircuts?”, ECB, 3 Nov 2016

Green Central Banking. (2021) “Decarbonising is Easy: Beyond Market Neutrality in the ECB’s Corporate QE”, Green Central Banking, 22 Oct 2021

MSCI. (2022) “Measuring Climate Impact with Total-Portfolio Carbon Footprinting”, MSCI, 18 Jul 2022